HSBC 2002 Annual Report Download - page 126

Download and view the complete annual report

Please find page 126 of the 2002 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

|

|

HSBC HOLDINGS PLC

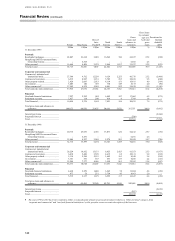

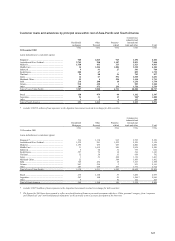

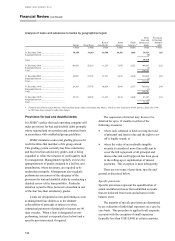

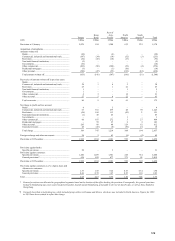

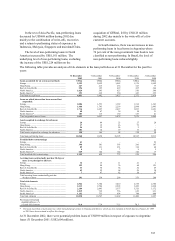

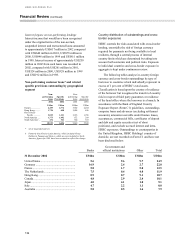

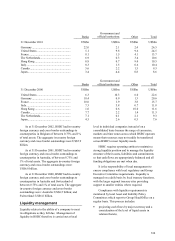

Financial Review (continued)

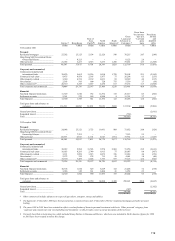

124

actual level of inherent losses is greater or less

than that suggested by historical experience.

Loss experience is defined as the annual new

provisions (net of recoveries for personal lending)

over a five-year period. These loss rates are applied

to all loans, other than those for which a specific

provision has been established in order to develop an

estimate of the level of losses inherent in the

portfolio at the reporting date. Management reviews

the need to hold a different level of general

allowance than that suggested by historical loss rates

by reference to current economic conditions and loan

gradings. Any adjustment made as a result of this

management judgement, and the basis for this

adjustment for each reporting entity, is documented

and reviewed by senior Group credit management.

The estimated period between losses occurring

and establishment of a specific provision for this loss

is determined by management for each identified

portfolio, having regard to the robustness of the

specific provisioning process and the availability of

information on which to assess specific provisions.

In general, the periods used vary between four

and nine months. In certain circumstances, such as

Argentina in 2001, economic conditions are such that

it is clear that historical loss experience provides

little evidence as to the inherent loss. In such

circumstances management will use their judgement

and any relevant experience from similar situations

to determine an appropriate provision.

Charge offs

Loans (and the related provisions) are charged off

either partially or in full when there is no prospect of

recovery of these amounts. HSBC therefore

generally writes off loans less quickly than US banks

leading to a higher reported level of credit risk

elements and associated provisions. New provisions

rather than amounts written off should be taken as

indications of current loss trends.

Loans on which interest is suspended

Provided that there is a realistic prospect of interest

being paid at some future date, interest on non-

performing loans is charged to the customer’ s

account. However, the interest is not credited to the

profit and loss account but to an interest suspense

account in the balance sheet which is netted against

the relevant loan. On receipt of cash (other than from

the realisation of security), suspended interest is

recovered and taken to the profit and loss account. A

specific provision of the same amount as the interest

receipt is then raised against the principal balance.

Amounts received from the realisation of security are

applied to the repayment of outstanding

indebtedness, with any surplus used to recover any

specific provisions and then suspended interest.

Non-accrual loans

Where the probability of receiving interest payments

is remote, interest is no longer accrued and any

suspended interest balance is written off.

Loans are not reclassified as accruing until

interest and principal payments are up-to-date and

future payments are reasonably assured.

Assets acquired in exchange for advances in

order to achieve an orderly realisation continue to be

reported as advances. The asset acquired is recorded

at the carrying value of the advance disposed of at

the date of the exchange and provisions are based on

any subsequent deterioration in its value.