Energizer 2009 Annual Report Download - page 19

Download and view the complete annual report

Please find page 19 of the 2009 Energizer annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

ENERGIZER HOLDINGS INC. 2009 ANNUAL REPORT PAGE 17

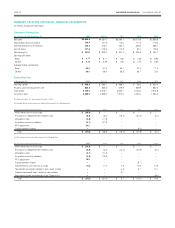

A summary of the Company’s significant contractual obligations at

September 30, 2009 is shown below:

Total

Less than

1 year 1-3 years 3-5 years

More than

5 years

Long-term debt,

including current

maturities

$2,389.5

$101.0

$497.0

$ 891.5

$900.0

Interest on

long-term debt

592.1

106.8

204.4

147.1

133.8

Operating leases 75.3 23.1 26.2 14.9 11.1

Purchase

obligations

and other (1)

44.1 37.5

3.4 3.2 –

Total $3,101.0 $268.4 $731.0 $1,056.7 $1,044.9

(1) The Company has estimated approximately $2.8 of cash settlements associated with unrecognized

tax benefits within the next year, which are included in the table above. As of September 30, 2009,

the Company’s Consolidated Balance Sheet reflects a liability for unrecognized tax benefits of $46.9,

excluding $7.4 of interest and penalties. The contractual obligations table above does not include this

liability. Due to the high degree of uncertainty regarding the timing of future cash outflows of liabilities

for unrecognized tax benefits beyond one year, a reasonable estimate of the period of cash settlement

for periods beyond the next twelve months cannot be made, and thus is not included in this table.

The Company has contractual purchase obligations for future

purchases, which generally extend one to three months. These

obligations are primarily purchase orders at fair value that are part of

normal operations and are reflected in historical operating cash flow

trends. In addition, the Company has various commitments related to

service and supply contracts that contain penalty provisions for early ter-

mination. As of September 30, 2009, we do not believe such purchase

obligations or termination penalties will have a significant effect on our

results of operations, financial position or liquidity position in the future.

In addition, the above contractual obligations table does not include

minimum contributions related to the Company’s retirement programs

as they are not considered material to the cash flow and liquidity of the

Company for any given fiscal year presented. The U.S. pension plans

constitute more than 70% of the total benefit obligations and plan assets

for the Company’s pension plans. At this time, we do not believe that a

minimum pension contribution for the U.S. plan will be required before

fiscal 2012, and, we do not believe such a minimum payment, if any,

will be material to the Company’s liquidity or cash flow based on current

discount rates, expected return on plan assets and plan design. Total

pension contributions for the Company in 2010 are estimated to be

approximately $19.

The Company believes cash flows from operating activities and periodic

borrowings will be adequate to meet short-term and long-term liquidity

requirements prior to the maturity of the Company’s credit facilities,

although no guarantee can be given in this regard.

Market Risk Sensitive Instruments and Positions

The market risk inherent in the Company’s financial instruments and

positions represents the potential loss arising from adverse changes

in currency rates, commodity prices, interest rates and the Com-

pany’s stock price. The following risk management discussion and

the estimated amounts generated from the sensitivity analyses are

forward-looking statements of market risk assuming certain adverse

market conditions occur. Company policy allows derivatives to be used

only for identifiable exposures and, therefore, the Company does not

enter into hedges for trading purposes where the sole objective is to

generate profits.

Currency Rate Exposure A significant portion of our product cost is

more closely tied to the U.S. dollar and, to a lesser extent, the Euro,

than to the local currencies in which the product is sold. As such, a

weakening of currencies relative to the U.S. dollar and, to a lesser

extent, the Euro, results in margin declines unless mitigated through

pricing actions, which are not always available due to the competitive

and economic environment. Conversely, strengthening of currencies

relative to the U.S. dollar and, to a lesser extent, the Euro can improve

margins. This margin impact coupled with the translation of foreign

operating results to the U.S. dollar, our financial reporting currency,

has an impact on reported operating profits. In 2009, the U.S. dollar

strengthened considerably versus most foreign currencies during our

first fiscal quarter due to the global economic crisis. We estimate that

operating profit for fiscal 2009 was negatively impacted by approxi-

mately $120 as compared to fiscal 2008 from unfavorable currency

movements. Changes in the value of local currencies in relation to the

U.S. dollar, and, to a lesser extent, the Euro will continue to impact

reported sales and segment profitability in the future, and we cannot

predict the direction or magnitude of future changes.

The Company generally views its investments in foreign subsidiaries

with a functional currency other than the U.S. dollar as long-term.

As a result, the Company does not generally hedge these net invest-

ments. Capital structuring techniques are used to manage the net

investment in foreign currencies, as necessary. Additionally, the

Company attempts to limit its U.S. dollar net monetary liabilities

in countries with unstable currencies.

From time to time the Company may employ foreign currency hedging

techniques to mitigate potential losses in earnings or cash flows on

foreign currency transactions, which primarily consist of anticipated

intercompany purchase transactions and intercompany borrowings.

External purchase transactions and intercompany dividends and

service fees with foreign currency risk may also be hedged. The

primary currencies to which the Company’s foreign affiliates are

exposed include the U.S. dollar, the Euro, the Yen, the British pound,

the Canadian dollar and the Australian dollar.

The Company uses natural hedging techniques, such as offsetting like

foreign currency cash flows, foreign currency derivatives with durations

of generally one year or less, including forward exchange contracts,

purchased put and call options and zero-cost option collars. Certain

of the foreign exchange contracts have been designated and are

accounted for as cash flow hedges.

The Company enters into foreign currency derivative contracts

to hedge existing balance sheet exposures. Any losses on these

contracts would be fully offset by exchange gains on the underlying

exposures, thus they are not subject to significant market risk. At

September 30, 2009, the Company had a loss of $1.1 included in

earnings on these unsettled forward currency contracts. In addition, the

Company has entered into a series of forward currency contracts to

hedge the cash flow uncertainty of forecasted inventory purchases due

to short term currency fluctuations. These transactions are accounted

for as cash flow hedges. At September 30, 2009, the Company had

an unrecognized pre-tax loss on these forward currency contracts

accounted for as cash flow hedges of $15.3 included in Accumulated

Other Comprehensive Income. Contract maturities for these hedges

extend into 2012.