Energizer 2009 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2009 Energizer annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

Management’s Discussion and Analysis of Results of Operations and Financial Condition

(Dollars in millions, except per share and percentage data)

PAGE 16 ENERGIZER HOLDINGS INC. 2009 ANNUAL REPORT

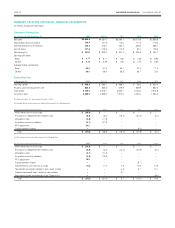

Capital expenditures of approximately $150 are anticipated in 2010

with increases in new product and cost reduction-related capital

driving the largest components of projected capital spending. Such

capital expenditures are expected to be financed with funds generated

from operations.

Financing Activities The Company’s total borrowings were $2,558.6

at September 30, 2009. The Company maintained total committed

debt facilities of $3,048.6, of which $477.4 remained available as of

September 30, 2009.

As noted previously, on May 20, 2009, the Company completed the

sale of an additional 10.925 million shares of common stock for

$49.00 per share. Net proceeds from the sale of the additional

shares were $510.2.

In October 2007, the Company borrowed approximately $1,500

under a bridge loan facility which, together with cash on hand, was

used to acquire Playtex. The Company subsequently refinanced the

bridge loan with $890 of long-term debt financing, with maturities

ranging from three to ten years and fixed rates ranging from 5.71%

to 6.55% and $600 of long-term bank financing priced at LIBOR plus

75 basis points.

Under the terms of the Company’s credit agreements, the ratio of the

Company’s indebtedness to its EBITDA, as defined in the agreements,

cannot be greater than 4.00 to 1, and may not remain above 3.50 to

1 for more than four consecutive quarters. If and so long as the ratio

is above 3.50 to 1 for any period, the Company is required to pay

additional interest expense for the period in which the ratio exceeds

3.50 to 1. The interest rate margin and certain fees vary depending

on the indebtedness to EBITDA ratio. Under the Company’s private

placement note agreements, the ratio of indebtedness to EBITDA

may not exceed 4.0 to 1. However, if the ratio is above 3.50 to 1, the

Company is required to pay an additional 75 basis points in interest

for the period in which the ratio exceeds 3.50 to 1. In addition, under

the credit agreements, the ratio of its current year EBIT, as defined

in the agreements, to total interest expense must exceed 3.00 to 1.

The Company’s ratio of indebtedness to its EBITDA was 3.14 to 1,

and the ratio of its EBIT to total interest expense was 4.40 to 1, as of

September 30, 2009. Each of the calculations at September 30, 2009

was pro forma for the Edge/Skintimate shave preparation acquisition.

The Company anticipates that it will remain in compliance with its debt

covenants for the foreseeable future. The negative impact on EBITDA

resulting from the VERO and RIF charges in the fourth quarter of 2009

had a negative impact on the ratio of indebtedness to EBITDA as such

charges are not excluded from the calculation of EBITDA under the

terms of the agreements. The VERO and RIF charges will negatively

impact trailing twelve month EBITDA, which is used in the ratio,

through the third quarter of fiscal 2010, after which it will roll out of the

calculation. Savings from the VERO and RIF programs will somewhat

mitigate the negative EBITDA impact of the restructuring charges as

they are realized during this time frame, and will remain a positive impact

on the ratio going forward. If the Company fails to comply with the

financial covenants referred to above or with other requirements of the

credit agreements or private placement note agreements, the lenders

would have the right to accelerate the maturity of the debt. Accelera-

tion under one of these facilities would trigger cross defaults on other

borrowings. The Company believes that the cost and long-term nature

of its current debt structure is a valuable asset given recent changes

in the credit markets due to the recent global economic crisis.

Additionally, the Company believes that reducing overall leverage

and maintaining a covenant cushion with a portion of the proceeds

of the recent equity offering should provide adequate capital for the

Company to pursue its strategic initiatives and provide greater financial

and operational flexibility, while helping to preserve the strength of its

current favorable debt structure.

On May 5, 2009, the Company amended and renewed its existing

receivables securitization program, under which the Company sells

interests in certain accounts receivable, and which provides funding

to the Company of up to $200 with two large financial institutions.

The sales of the receivables are affected through a bankruptcy remote

special purpose subsidiary of the Company, Energizer Receivables

Funding Corporation (ERFC). Funds received under this financing

arrangement are treated as borrowings rather than proceeds of

accounts receivables sold for accounting purposes. However,

borrowings under the program are not considered debt for covenant

compliance purposes under the Company’s credit agreements and

private placement note agreements. The program is subject to renewal

annually on the anniversary date. At September 30, 2009, a total of

$147.5 was outstanding under this financing arrangement.

Parties to long-term committed borrowings consist of a number of major

international financial institutions. The Company continually monitors

positions with, and credit ratings of, counterparties both internally and

by using outside ratings agencies. The Company has staggered long-

term borrowing maturities through 2017 to reduce refinancing risk in

any single year and to optimize the use of cash flow for repayment.

The Company purchased shares of its common stock as follows

(shares in millions):

Fiscal Year

Shares

Cost

Total

Average

Price

2009 0.0 $ 0.0 $ 0.00

2008 0.0 $ 0.0 $ 0.00

2007 0.8 $ 53.0 $67.67

The Company has 8 million shares remaining on the current authoriza-

tion from its Board of Directors to repurchase its common stock in the

future. Future purchases may be made from time to time on the open

market or through privately negotiated transactions, subject to corpo-

rate objectives and the discretion of management.