Energizer 2003 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2003 Energizer annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48

|

|

ENR 2003 ANNUAL REPORT Page 37

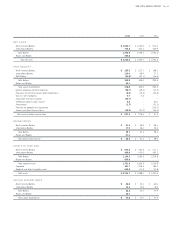

The detail of long-term debt at September 30 is as follows:

2003 2002

Private Placement, fixed interest rates ranging from

2.3% to 4.3%, due 2006 to 2013 $ 375.0 $–

Private Placement, variable interest at LIBOR +

65 to 75 basis points, or ranging from 1.8% to

1.9% at September 30, 2003, due 2008 to 2013 325.0 –

Singapore Syndication, U.S. Dollar Loan, variable

interest at SIBOR + 1%, or 2.1% at

September 30, 2003, due 2004 to 2008 125.0 –

Singapore Dollar Revolving Credit Facility, variable interest

rate, 1.6% at September 30, 2003, due 2006 78.6 –

Private Placement, interest rates ranging from 7.8%

to 8.0%, due 2003 to 2010 –175.0

Revolving Credit Facility, variable interest rate,

1.9% at September 30, 2003, due 2006 30.0 –

933.6 175.0

Less current portion 20.0 15.0

Total long-term debt $ 913.6 $ 160.0

Energizer maintains total committed debt facilities of $1,258.3, of

which $319.2 remained available as of September 30, 2003.

Under the terms of the facilities, the ratio of Energizer’s total indebted-

ness to its EBITDA cannot be greater than 3.5 to 1 and the ratio of its

EBIT to total interest expense must exceed 3.5 to 1. Additional restrictive

covenants exist under current debt facilities. Failure to comply with the

above ratios or other covenants could result in acceleration of maturity,

which could trigger cross defaults on other borrowings. Energizer believes

that covenant violations resulting in acceleration of maturity is unlikely.

Energizer’s fixed rate debt is callable by the company, subject to a “make

whole” premium, which would be required to the extent the underlying

benchmark United States treasury yield has declined since issuance.

Aggregate maturities on all long-term debt are as follows: $20.0 in

2004, $20.0 in 2005, $148.6 in 2006, $40.0 in 2007, $115.0 in

2008 and $590.0 thereafter.

14. SALE OF ACCOUNTS RECEIVABLE

Energizer entered into an agreement to sell, on an ongoing basis, a pool of

domestic trade accounts receivable to a wholly owned bankruptcy-remote

subsidiary of Energizer. The subsidiary qualifies as a Special Purpose

Entity (SPE) for accounting purposes and is therefore not consolidated for

financial reporting purposes. The SPE’s sole purpose is the acquisition of

receivables from Energizer and the sale of its interests in the receivables to

a multi-seller receivables securitization company. Energizer’s investment in

the SPE is recorded at carrying value and classified as other current assets

on the Consolidated Balance Sheet as disclosed below.

The activity related to the SPE at September 30 is presented in the

table below. The net proceeds of the transaction were used to reduce

various debt instruments. The proceeds are reflected as operating cash

flows in Energizer’s Consolidated Statement of Cash Flows.

AS OF SEPTEMBER 30, 2003 2002

Total outstanding accounts receivable sold to SPE $ 175.7 $ 164.6

Cash received by SPE from sale of receivables

to a third party 75.0 –

Subordinated retained interest 100.7 164.6

Energizer’s investment in SPE 100.7 164.6

Absent the sale treatment required for the SPE, Energizer’s balance

sheet would reflect additional accounts receivable, notes payable and

lower other current assets as follows:

AS OF SEPTEMBER 30, 2003 2002

Additional accounts receivable $ 175.7 $ 164.6

Additional notes payable 75.0 –

Lower other current assets 100.7 164.6

15. PREFERRED STOCK

Energizer’s Articles of Incorporation authorize Energizer to issue up to 10

million shares of $.01 par value of preferred stock. As of September 30,

2003, there were no shares of preferred stock outstanding.

16. SHAREHOLDERS EQUITY

On March 16, 2000, the Board of Directors declared a dividend of one

share purchase right (Right) for each outstanding share of ENR common

stock. Each Right entitles a shareholder of ENR stock to purchase an

additional share of ENR stock at an exercise price of $150.00, which

price is subject to anti-dilution adjustments. Rights, however, may only

be exercised if a person or group has acquired or commenced a public

tender for 20% or more of the outstanding ENR stock, unless the acqui-

sition is pursuant to a tender or exchange offer for all outstanding shares

of ENR stock and a majority of the Board of Directors determines that

the price and terms of the offer are adequate and in the best interests of

shareholders (a Permitted Offer). At the time that 20% or more of the

outstanding ENR stock is actually acquired (other than in connection

with a Permitted Offer), the exercise price of each Right will be adjusted

so that the holder (other than the person or member of the group that

made the acquisition) may then purchase a share of ENR stock at one-

third of its then-current market price. If Energizer merges with any other

person or group after the Rights become exercisable, a holder of a Right

may purchase, at the exercise price, common stock of the surviving entity

having a value equal to twice the exercise price. If Energizer transfers

50% or more of its assets or earnings power to any other person or group

after the Rights become exercisable, a holder of a Right may purchase,

at the exercise price, common stock of the acquiring entity having a

value equal to twice the exercise price.