Energizer 2002 Annual Report Download - page 19

Download and view the complete annual report

Please find page 19 of the 2002 Energizer annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

|

|

foreign currency derivatives with a duration of generally one year or less

may be used, including forward exchange contracts, purchased put and

call options, and zero-cost option collars. Energizer policy allows foreign

currency derivatives to be used only for identifiable foreign currency expo-

sures and, therefore, Energizer does not enter into foreign currency con-

tracts for trading purposes where the sole objective is to generate profits.

Energizer has not designated any financial instruments as hedges for

accounting purposes in the three years ended September 30, 2002.

Market risk of foreign currency derivatives is the potential loss in fair value

of net currency positions for outstanding foreign currency contracts at fis-

cal year-end, resulting from a hypothetical 10% adverse change in all

foreign currency exchange rates. Market risk does not include foreign

currency derivatives that hedge existing balance sheet exposures, as any

losses on these contracts would be fully offset by exchange gains on the

underlying exposures for which the contracts are designated as hedges.

Accordingly, the market risk of Energizer’s foreign currency derivatives at

September 30, 2002 and 2001 amounts to $.9 and $1.9, respectively.

Energizer generally views as long-term its investments in foreign sub-

sidiaries with a functional currency other than the U.S. dollar. As a

result, Energizer does not generally hedge these net investments.

Capital structuring techniques are used to manage the net investment

in foreign currencies as considered necessary. Additionally, Energizer

attempts to limit its U.S. dollar net monetary liabilities in countries with

unstable currencies. In March 2002, Energizer contributed $8.4 of capi-

tal to its Argentine subsidiary sufficient to repay all U.S. dollar liabilities

in order to mitigate exposure to currency exchange losses.

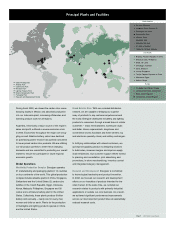

In terms of foreign currency translation risk, Energizer is exposed to the

Swiss franc, the Euro and other European currencies; the Mexican and

Argentine peso and other Latin American currencies; and the Singapore

dollar, Chinese renminbi, Australian and Hong Kong dollars, and other

Asian currencies. Energizer’s net foreign currency investment in foreign

subsidiaries and affiliates translated into U.S. dollars using year-end

exchange rates was $279.5 and $329.2 at September 30, 2002 and 2001,

respectively. The potential loss in value of Energizer’s net foreign currency

investment in foreign subsidiaries resulting from a hypothetical 10% adverse

change in quoted foreign currency exchange rates at September 30, 2002

and 2001 amounts to $28.0 and $32.9, respectively.

Stock Price

A portion of Energizer’s deferred compensation liabilities is based on

Energizer stock price and is subject to market risk. In May 2002,

Energizer entered into a prepaid share option transaction to mitigate this

risk. Energizer invested $22.9 in the prepaid share option transaction

covering 840,000 share equivalents in Energizer deferred compensation

plans. The change in fair value of these options for the year resulted in

income of $2.6, which was substantially offset by an increase in the

deferred compensation liability tied to the Energizer stock price.

Critical Accounting Policies

Energizer identified the policies below as critical to its business operations

and the understanding of its results of operations. The following discussion

is presented as recommended by Financial Reporting Release No. 60,

“Cautionary Advice Regarding Disclosure About Critical Accounting

Policies.” The impact and any associated risks related to these policies on

its business operations is discussed throughout Management’s Discussion

and Analysis of Financial Condition and Results of Operations where such

policies affect the reported and expected financial results.

Preparation of the financial statements in conformity with generally

accepted accounting principles in the United States requires Energizer to

make estimates and assumptions that affect the reported amounts of

assets and liabilities, disclosure of contingent assets and liabilities and the

reported amounts of revenues and expenses. On an ongoing basis,

Energizer evaluates its estimates, including those related to customer

programs and incentives, product returns, bad debts, inventories, intangible

assets and other long-lived assets, income taxes, financing operations,

restructuring, pensions and other postretirement benefits, and contingen-

cies. Actual results could differ from those estimates. This listing is not

intended to be a comprehensive list of all of Energizer’s accounting policies.

Revenue Recognition Energizer provides its customers a variety of pro-

grams designed to promote sales of its products, many of which require

periodic payments and allowances based on estimated results of specific

programs. Such payments and allowances are recorded as a reduction to

net sales. Energizer accrues at the time of sale the estimated total pay-

ments and allowances associated with each sale and continually assesses

the adequacy of accruals for program costs not yet paid. To the extent total

program payments differ from estimates, adjustments may be necessary.

Allowance for Doubtful Accounts Energizer maintains an allowance for

doubtful accounts receivable for estimated losses resulting from customers

that are unable to meet their financial obligations. The financial condition of

specific customers is considered when establishing the allowance.

Provisions to increase the allowance for doubtful accounts are included in

selling, general and administrative expenses. If actual bad debt losses

exceed estimates, additional provisions may be required in the future.

Pension Plans and Other Postretirement Benefits The determination of

Energizer’s obligation and expense for pension and other postretirement

benefits is dependent on certain assumptions developed by Energizer and

used by actuaries in calculating such amounts. Assumptions include,

among others, the discount rate, future salary increases and the expected

long-term rate of return on plan assets. Actual results that differ from

ENR 2002 Annual Report Page 17