EasyJet 2013 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2013 EasyJet annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

easyJet plc Annual report and accounts 2013

92

Independent Auditors’ report

to the members of easyJet plc continued

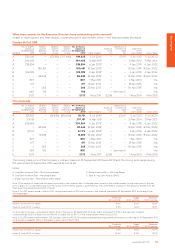

Area of focus How the scope of our audit addressed the area of focus

Aircraft maintenance provisions

The Directors have included a provision of £252 million for

aircraft maintenance costs in respect of aircraft leased under

operating leases (refer to notes 1 and 16 to the accounts).

We focused on this area because of a level of difficulty in

estimating the amount of the provision as a result of the

complex and subjective judgements that the Directors

needed to make.

We evaluated and tested the Directors’ maintenance

provision model and calculations, including evaluating the

reasonableness of the assumptions, testing the input data

and reperforming calculations. We also performed sensitivity

analysis around the key drivers of the model: likely utilisation

of the aircraft; the expected cost of the heavy maintenance

check at the time it is expected to occur; the condition of

the aircraft; and the lifespan of life-limited parts. Having

ascertained the magnitude of movements in those

assumptions, that either individually or collectively would be

required for the provision to be misstated, we considered

the likelihood of such movements arising and any impact

on the overall level of provision recorded in the accounts.

Risk of management override of internal controls

ISAs (UK & Ireland) require that we consider this.

We assessed the overall control environment of the Group,

including the arrangements for staff to ‘whistle-blow’

inappropriate actions, and interviewed senior management

and the Group’s internal audit function. We examined the

significant accounting estimates and judgements relevant to

the accounts for evidence of bias by the Directors that may

represent a risk of material misstatement due to fraud. We

also tested journal entries.

Fraud in revenue recognition

ISAs (UK & Ireland) presume there is a risk of fraud in revenue

recognition because of the pressure management may feel

to achieve the planned results. We focused on the timing of

the recognition of seat revenue and its presentation in the

consolidated income statement, because this is dependent

on the fulfilment of certain obligations.

We evaluated the relevant information technology systems and

tested the internal controls over the completeness, accuracy

and timing of seat revenue recognised in the accounts. We

tested the reconciliations between the revenue systems used

by the Group and its financial ledgers and journal entries posted

to revenue accounts to identify unusual or irregular items. We

also tested the timing of revenue recognition, checking the

necessary obligations had been fulfilled, generally that the

relevant flight had taken place.

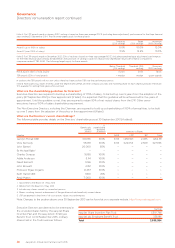

Going concern

Under the Listing Rules we are required to review

the Directors’ statement, set out on page 36, in

relation to going concern. We have nothing to

report having performed our review.

As noted in the Directors’ statement, the Directors

have concluded that it is appropriate to prepare the

Group’s and the Company’s accounts using the going

concern basis of accounting. The going concern basis

presumes that the Group and the Company have

adequate resources to remain in operation, and that

the Directors intend them to do so, for at least one

year from the date the accounts were signed. As part

of our audit we have concluded that the Directors’

use of the going concern basis is appropriate.

However, because not all future events or

conditions can be predicted, these statements

are not a guarantee as to the Group’s and the

Company’s ability to continue as a going concern.

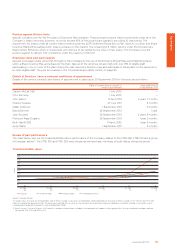

OPINIONS ON MATTERS

PRESCRIBED BY THE COMPANIES

ACT 2006

In our opinion:

• the information given in the Strategic Report

and the Directors’ Report for the financial year

for which the accounts are prepared is consistent

with the accounts; and

• the part of the Directors’ remuneration report

to be audited has been properly prepared in

accordance with the Companies Act 2006.