EasyJet 2013 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2013 EasyJet annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

www.easyJet.com

$FFRXQWVRWKHULQIRUPDWLRQ

Changes in intrinsic fair value are recognised in other comprehensive income to the extent that the cash flow hedges

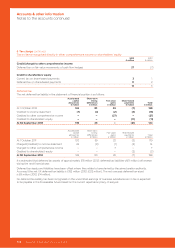

are determined to be effective. All other changes in fair value are recognised immediately in the income statement.

Where the hedged item is a non-financial asset, the accumulated gains and losses previously recognised in other

comprehensive income form part of the initial carrying amount of the asset. Otherwise accumulated gains and losses

are recognised in the income statement in the same period in which the hedged items affect the income statement.

Hedge accounting is discontinued when a hedging instrument is derecognised (e.g. through expiry or disposal),

or no longer qualifies for hedge accounting. Where the hedged item is a highly probable forecast transaction,

the related gains and losses remain in shareholders’ equity until the transaction takes place.

When a hedged future transaction is no longer expected to occur, any related gains and losses held in shareholders’

equity are immediately recognised in the income statement.

%HM@MBH@KFT@Q@MSDDR

If a claim on a financial guarantee given to a third party becomes probable, the obligation is recognised at fair value.

For subsequent measurement, the carrying amount is the higher of initial measurement and best estimate of the

expenditure required to settle the obligation at the reporting date.

3@W

Tax expense in the income statement comprises both current and deferred tax. Tax is recognised in the income

statement except when it relates to items credited or charged directly to other comprehensive income or shareholders’

equity, in which case it is recognised in other comprehensive income or shareholders’ equity. The charge for current tax

is based on the results for the year as adjusted for income that is exempt and expenses that are not deductible using

tax rates that are applicable to the taxable income.

Deferred tax is provided in full on temporary differences relating to the carrying amount of assets and liabilities, where it

is probable that the recovery or settlement will result in an obligation to pay more, or a right to pay less, tax in the future,

with the following exceptions:

where the temporary difference arises from goodwill or from the initial recognition (other than in a business

combination) of other assets and liabilities in a transaction that affects neither taxable income nor accounting

profit; and

deferred tax arising on investments in subsidiaries is not recognised where easyJet is able to control the reversal

of the temporary difference and it is probable that the temporary difference will not reverse in the foreseeable future.

Deferred tax is measured on an undiscounted basis at the tax rates that are expected to apply in the periods in

which recovery of assets and settlement of liabilities are expected to take place, based on tax rates or laws enacted

or substantively enacted at the date of the statement of financial position.

Deferred tax assets represent amounts recoverable in future periods in respect of deductible temporary differences,

losses and tax credits carried forwards. Deferred tax assets are recognised to the extent that it is probable that there

will be suitable taxable profits from which they can be deducted.

Deferred tax liabilities represent the amount of income taxes payable in future periods in respect of taxable

temporary differences.

Deferred tax assets and liabilities are offset when there is a legally enforceable right to set off current tax assets against

current tax liabilities and it is the intention to settle these on a net basis.

HQBQ@ESL@HMSDM@MBDOQNUHRHNMR

The accounting for the cost of providing major airframe and certain engine maintenance checks for owned and finance

leased aircraft is described in the accounting policy for property, plant and equipment.

easyJet has contractual obligations to maintain aircraft held under operating leases. Provisions are created over the term

of the lease based on the estimated future costs of major airframe checks, engine shop visits and end of lease liabilities.

These costs are discounted to present value where the amount of the discount is considered material.

Where an aircraft is sold and leased back other than when first delivered to easyJet, a liability to undertake future

maintenance activities, resulting from past flying activity, arises at the point the lease agreement is signed. The cost

is treated as part of the surplus or shortfall arising on the sale and leaseback, the accounting treatment of which

is described in the leases accounting policy.

A number of leases also require easyJet to pay supplemental rent to the lessor. The purpose of these payments

is to provide the lessor with collateral should an aircraft be returned in a condition that does not meet the requirements

of the lease. Supplemental rent is either refunded when qualifying maintenance is performed, or when the lease ends.

103

www.easyJet.com

Accounts & other information