Cincinnati Bell 2007 Annual Report Download - page 159

Download and view the complete annual report

Please find page 159 of the 2007 Cincinnati Bell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

|

|

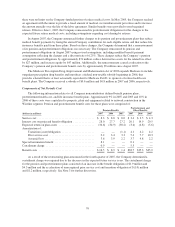

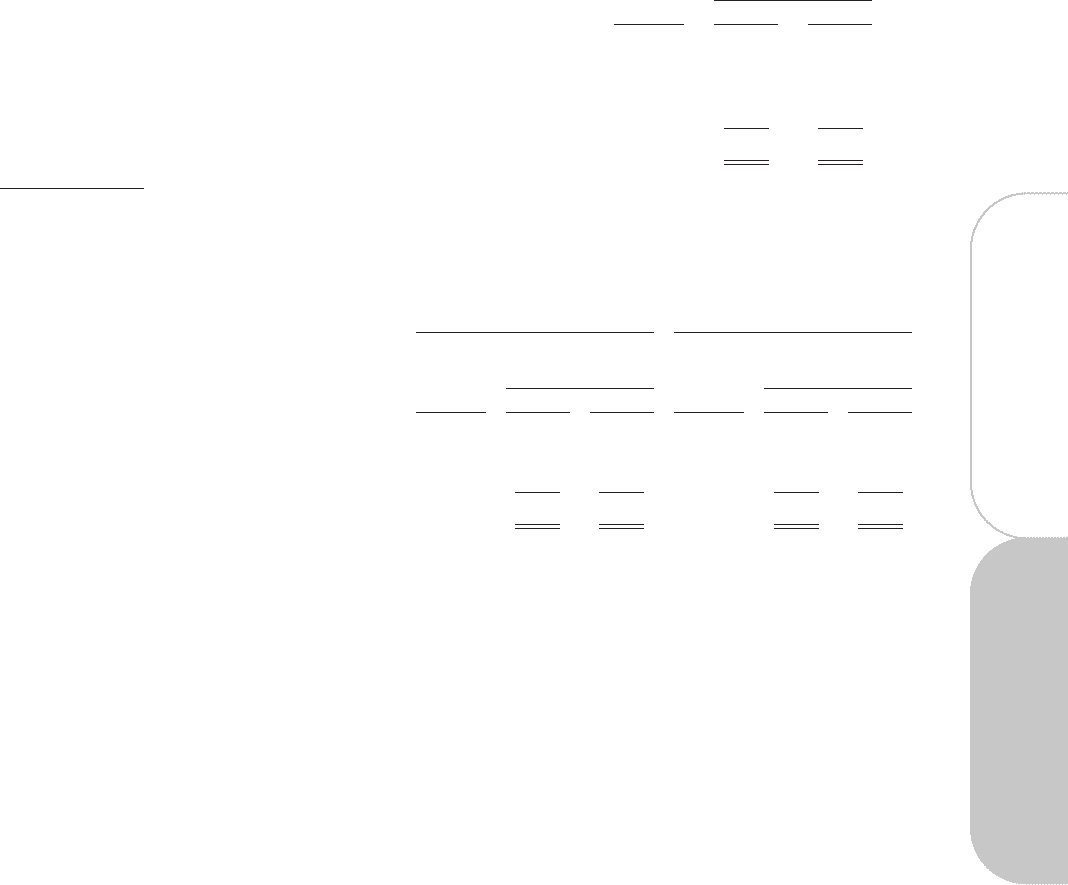

The pension plans’ assets consist of the following:

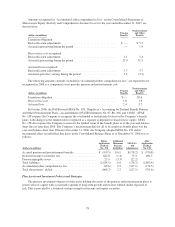

Target

Allocation

2008

Percentage of Plan

Assets at

December 31,

2007 2006

Plan assets:

Fixed income securities ................................... 20-38% 30.2% 30.0%

Equity securities * ....................................... 55-65% 59.0% 59.9%

Real estate ............................................. 8-12% 10.8% 10.1%

Total .................................................. 100.0% 100.0%

* At December 31, 2007, no pension plan assets were invested in Company common stock.

At December 31, 2006, pension plan assets included $6.4 million in Company common stock.

The postretirement and other plans’ assets consist of the following:

Health Care Group Life Insurance

Target

Allocation

2008

Percentage of Plan

Assets at

December 31, Target

Allocation

2008

Percentage of Plan

Assets at

December 31,

2007 2006 2007 2006

Plan assets:

Fixed income securities .................... 35-45% 39.9% 36.3% 35 - 45% 39.5% 41.0%

Equity securities .......................... 55-65% 60.1% 63.7% 55 - 65% 60.5% 59.0%

Total ................................... 100.0% 100.0% 100.0% 100.0%

Company contributions to its qualified pension plans were $24.1 million in 2007. No contributions were

required in 2006 or 2005. Company contributions to its non-qualified pension plan were $2.4 million, $2.5

million and $2.6 million for 2007, 2006 and 2005, respectively.

The Company expects to make cash payments of approximately $11 million related to its postretirement

health plans in 2008. Due to the early pension contribution of $20.0 million made in December 2007, the

Company does not expect to make any contributions to its qualified pension plan in 2008. Contributions to non-

qualified pension plans in 2008 are expected to be approximately $2 million.

The Pension Protection Act of 2006 (“the Act”) was enacted on August 17, 2006. Most of its provisions will

become effective in 2008. The Act significantly changes the funding requirements for single-employer defined

benefit pension plans. The funding requirements will now largely be based on a plan’s calculated funded status,

with faster amortization of any shortfalls or surpluses. The Act directs the U.S. Treasury Department to develop a

new yield curve to discount pension obligations for determining the funded status of a plan when calculating the

funding requirements. Based on current assumptions, the Company believes it will pay an estimated $45 million

to fund its qualified pension plans during the period 2009 to 2017.

Additional Minimum Liability

An additional minimum pension liability adjustment was required in 2006 as the accumulated benefit

obligation exceeded the fair value of pension plan assets for each of those plans as of the measurement date. The

additional minimum pension liability recorded (before the effect of income taxes) was $6.9 million. Upon the

adoption of SFAS No. 158, the Company is no longer required to record an additional minimum pension liability

as the unfunded status was recorded at December 31, 2006.

79

Form 10-K