CVS 2001 Annual Report Download - page 4

Download and view the complete annual report

Please find page 4 of the 2001 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

|

|

2001 will be remembered as a year of great challenge— fo r o ur co untry, fo r its citizens, and fo r

o ur eco no my. CVS Co rpo ratio n will remember the year no differently.

Businesses o f all sizes and acro ss every industry faced intense challenges as we adjusted

to the realities o f o ur weakening eco no my. We are fo rtunate that o ur business, fo r the mo st

part, is recession- resistant since we sell items that peo ple need in their daily lives.

Nevertheless, we experienced so me specific areas of disappo intment in 2001. We

have taken actio n to co rrect the iso lated po ckets of pro blems that were within o ur

co ntro l. Tho se facto rs no t within o ur co ntro l— including the absence o f majo r new

drug appro vals, the timing o f generic intro ductio ns, and the weak eco no my— are

likely to rebo und o ver time. We see significant cause fo r o ptimism in 2002

and beyo nd.

We believe the pharmacy industry has the best lo ng-term gro wth dynamics in

all o f retail. Acco rding to IMS Health, the pharmacy industry is pro jected to gro w

at a 12 to 14% annual rate thro ugh 2005. By that time, the pharmacy industry is

expected to fill o ne billio n mo re prescriptio ns than it do es to day. An aging American

populatio n, the intro duc tio n of new drug s, a stro ng generic pipeline, and the pro spect o f

expanding Medicare benefits all co ntribute to this pro mising o utlo o k. With mo re market leadership

positio ns than any co mpetito r— we rank #1 o r #2 in 75% of the markets we serve— we are

extremely well po sitio ned to seize such growth o ppo rtunities.

Our prescriptio n fo r gro wth includes a renewed fo cus o n what made us so successful in the

past— superio r executio n at the sto re level— by assuring o ur sto res meet the “ Triple S” o f custo mer

service. We want to be sure o ur custo mers can find everything they expect in-sto ck, that they can

sho p in a neat, well-o rganized sto re, and that they experience quick, perso nal, co urteo us se rvice .

We are po sitio ning o urselves with cutting-edge technology and inno vative marketing pro grams,

designed to impro ve service to customers and keep them co ming back to o ur sto res. Our ExtraCare®

Lo yalty Card, launched in early 2001, already has mo re than 25 millio n cardho lders, far surpassing

o ur pro jectio ns. Our EPIC ( Excellence in Pharmacy Inno vatio n and Care) so lutio n is active no w in

every sto re, increasing pharmacy pro ductivity and reducing customer wait times. And o ur Assisted

Invento ry Management ( AIM) system, which will be ro lled o ut in 2002, is expected to impro ve o ur

in- sto ck po sitio n, thereby enhancing custo mer service.

Our stro ng balance sheet is mo re cause fo r o ptimism as we enter 2002. We have the financial

strength to suppo rt o ur aggressive growth pro gram in the years to co me.

We intend to leverage that strength as we target and enter new markets. We are establishing

beachhead positio ns in so me o f the fastest- gro wing drugsto re markets in the U.S., including

Tampa, Orlando , Ft. Lauderdale, Miami, Chicago , Las Vegas, Dallas, and Ho uston. Early results are

extremely pro mising. We plan to co ntinue penetrating these and o ther high-g ro wth markets in

2002 and the fo reseeable future.

Finally, I have great co nfidence in o ur peo ple, particularly o ur senio r management team, which

I believe is the best in the industry. They have played an integral part in o ur past successes.

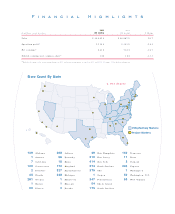

We have a stro ng histo ry o f gro wth at CVS, making swift, steady pro gress since beco ming a

public co mpany in 1996. Then, we had annual sales o f $5 billio n. To day, sales are mo re than $22

billio n. Then, we had 1,400 sto res in 14 states and the District o f Co lumbia. Today, we rank #1 in

sto re co unt with approximately 4,200 sto res in 33 states and the District o f Co lumbia.

TO OUR SHAREHOLDERS

Prescriptio n

fo r

Healthy

Financial

Growth