CVS 1999 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 1999 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

|

|

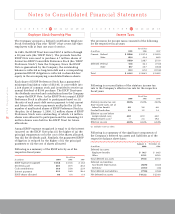

Notes to Consolidated Financial Statements

30

CVS Corporation

during the shutdown period, impairment was measured

using the “Assets to Be Held and Used” provisions of SFAS

No. 121. The analysis was prepared at the individual store

level, which is the lowest level at which individual cash

flows can be identified. The analysis first compared the

carrying amount of the store’s assets to the store’s estimated

future cash flows (undiscounted and without interest charges)

through the anticipated closing date. If the estimated future

cash flows used in this analysis were less than the carrying

amount of the store’s assets, an impairment loss calculation

was prepared. The impairment loss calculation compared the

carrying value of the store’s assets to the store’s estimated

future cash flows (discounted and with interest charges).

Management’s decision to close Revco’s corporate headquarters

was also considered to be an event or change in circumstances

as defined in SFAS No. 121. Since management intended

to dispose of these assets, impairment was measured using

the “Assets to Be Disposed Of” provisions of SFAS No. 121.

The impairment loss of $3.9 million for the facility that

Revco owned was calculated by subtracting the carrying

value of the facility from the estimated fair value less cost

to sell. Since management intended to discard the remaining

assets located in these facilities, their entire net book value

was considered to be impaired.

Contract cancellation costs included $7.4 million for estimated

termination fees and/or penalties associated with terminating

various contracts that Revco had in place prior to the merger,

which would not be used by the combined company.

Other costs included $3.5 million for estimated travel and

related expenses that would be incurred in connection

with closing Revco’s corporate headquarters and $2.0

million for other miscellaneous charges associated with

closing Revco’s corporate headquarters.

The above costs did not provide future benefit to the retained

stores or corporate facilities.

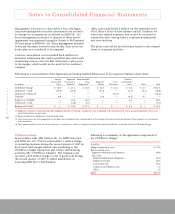

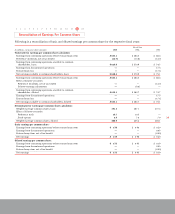

Following is a reconciliation of the beginning and ending liability balances as of the respective balance sheet dates:

Merger Employee Noncancelable Contract

Transaction Severance & Lease Duplicate Asset Cancellation

In millions Costs Benefits(1) Obligations(2) Facility Write-offs Costs Other Total

CVS/Revco Charge $ 35.0 $ 89.8 $ 67.0 $ 50.2 $ 82.2 $ 7.4 $ 5.5 $ 337.1

Utilization -- Cash (32.1) (37.4) (0.9) (37.6) — (5.1) (5.5) (118.6)

Utilization -- Noncash — — — — (82.2) — — (82.2)

Balance at 12/27/97 2.9 52.4 66.1 12.6 — 2.3 — 136.3

Utilization -- Cash (0.3) (40.0) (17.0) (11.8) — (2.3) (3.4) (74.8)

Transfer(3) (2.6) — — (0.8) — — 3.4 —

Balance at 12/26/98 — 12.4 49.1 — — — — 61.5

Utilization -- Cash — (3.4) (9.9) — — — — (13.3)

Balance at 01/1/00(4) $ — $ 9.0 $ 39.2 $ — $ — $ — $ — $ 48.2

(1) Employee severance extended through 1999. Employee benefits extend for a number of years to coincide with the payment of retirement benefits and excess

parachute payment excise taxes and related income tax gross-ups.

(2) Noncancelable lease obligations extend through 2017.

(3) The transfers between the components of the plan were recorded in the same period that the changes in estimates were determined. These amounts are considered

to be immaterial.

(4) The Company believes that the reserve balances as of January 1, 2000, are adequate to cover the remaining liabilities associated with the CVS/Revco Charge.

Big B Charge

In accordance with EITF Issue 94-3 and SFAS No. 121, the

Company recorded a $31.0 million charge to operating

expenses during the first quarter of 1997 for certain costs

associated with the restructuring of Big B, Inc. (the “Big B

Charge”), which the Company acquired in 1996. This

charge included accrued liabilities related to store closings

and duplicate corporate facilities, such as the cancellation

of lease agreements and the write-down of unutilized fixed

assets. Asset write-offs included in this charge totaled $5.1

million. The balance of the charge, $25.9 million, will

require cash outlays of which $15.9 million and $10.0

million had been incurred as of January 1, 2000, and

December 26, 1998, respectively. The remaining cash

outlays primarily include noncancelable lease commitments,

which extend through 2012. The above costs did not

provide future benefit to the retained stores or corporate

facilities.