Blackberry 2008 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2008 Blackberry annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88

|

|

82

RESEARCH IN MOTION LIMITED

notes to the consolidated financial statements continued

In thousands of United States dollars, except share and per share data, and except as otherwise indicated

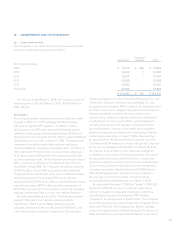

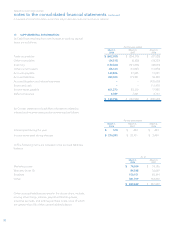

monitoring their creditworthiness. The Company’s exposure

to credit loss and market risk will vary over time as a function

of currency exchange rates. The Company measures its

counterparty credit exposure as a percentage of the total

fair value of the applicable derivative instruments. Where the

net fair value of derivative instruments with any counterparty

is negative, the Company deems the credit exposure to that

counterparty to be nil. As at March 1, 2008, the maximum

credit exposure to a single counterparty, measured as a

percentage of the total fair value of derivative instruments

with net unrealized gains was 40% (March 3, 2007 – nil;

March 4, 2006 – 46%).

The Company is exposed to market and credit risk on

its investment portfolio. The Company reduces this risk by

investing in liquid, investment grade securities and by limiting

exposure to any one entity or group of related entities. As at

March 1, 2008, no single issuer represented more than 9% of

the total cash, cash equivalents and investments (March 3, 2007

- no single issuer represented more than 9% of the total cash,

cash equivalents and investments).

Cash and cash equivalents and investments are invested

in certain instruments of varying maturities. Consequently,

the Company is exposed to interest rate risk as a result of

holding investments of varying maturities. The fair value

of investments, as well as the investment income derived

from the investment portfolio, will fluctuate with changes in

prevailing interest rates. The Company does not currently

utilize interest rate derivative instruments in its investment

portfolio.

The Company, in the normal course of business, monitors

the financial condition of its customers and reviews the credit

history of each new customer. The Company establishes

an allowance for doubtful accounts that corresponds to

the specific credit risk of its customers, historical trends

and economic circumstances. The allowance for doubtful

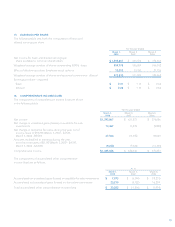

accounts as at March 1, 2008 is $2,016 (March 3, 2007- $1,824).

While the Company sells its products and services to

a variety of customers, three customers comprised 19%,

14% and 10% of trade receivables as at March 1, 2008

(March 3, 2007 - two customers comprised 23% and 13%).

Additionally, three customers comprised 21%, 15% and 12%

of the Company’s revenue (March 3, 2007 - four customers

comprised 19%, 14%, 11% and 11%; March 4, 2006 - four

customers comprised 19%, 16%, 12% and 12%).

The Company has entered into forward contracts to

hedge exposures relating to foreign currency anticipated

transactions. These contracts have been designated as cash

flow hedges, with the effective portion of the change in fair

value initially recorded in other comprehensive income and

subsequently reclassified to earnings in the period in which

the cash flows from the associated hedged transactions

affect earnings. Any ineffective portion of the change in

fair value of the cash flow hedges is recognized in current

period earnings. For fiscal years ending 2008, 2007 and

2006, the derivatives designated as cash flow hedges were

considered to be fully effective with no resulting portions

being designated as ineffective. The maturity dates of these

instruments range from March 2008 to November 2010. As

at March 1, 2008, the net unrealized gain on these forward

contracts was approximately $34,593 (March 3, 2007 – net

unrealized loss of $7,834; March 4, 2006 – net unrealized gain

of $24,868). Unrealized gains associated with these contracts

were recorded in Other current assets and Accumulated other

comprehensive income. Unrealized losses were recorded in

Accrued liabilities and Accumulated other comprehensive

income. These derivative gains or losses are reclassified to

earnings in the same period that the forecasted transaction

affects earnings. In fiscal 2009, $24,545 of the net unrealized

gain on the forward contracts will be reclassified to earnings.

The Company has entered into forward contracts to hedge

certain monetary assets and liabilities that are exposed to

foreign currency risk. These contracts have been designated

as economic hedges that are not subject to hedge

accounting, with gains and losses on the hedge instruments

being recognized in earnings each period, offsetting the

change in the U.S. dollar value of the hedged asset or liability.

The maturity dates of these instruments are in March 2008. As

at March 1, 2008, a net unrealized loss of $6,880 was recorded

in respect of this amount (March 3, 2007 – unrealized gain

of $542; March 4, 2006 – unrealized loss of $386). Unrealized

gains associated with these contracts were recorded in Other

current assets and Selling, marketing and administration.

Unrealized losses were recorded in Accrued liabilities and

Selling, marketing and administration.

The Company is exposed to credit risk on derivative

financial instruments arising from the potential for

counterparties to default on their contractual obligations.

The Company mitigates this risk by limiting counterparties

to highly rated financial institutions and by continuously