Bed, Bath and Beyond 2006 Annual Report Download - page 11

Download and view the complete annual report

Please find page 11 of the 2006 Bed, Bath and Beyond annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

|

|

BED BATH& BEYOND ANNUAL REPORT 2006

9

In June 2006, the FASB issued FASB Interpretation No. (“FIN”) 48, “Accounting for Uncertainty in Income Taxes – An Interpretation

of FASB Statement No. 109.” FIN No. 48 prescribes a recognition threshold and measurement attribute for the financial statement

recognition and measurement of a tax position taken or expected to be taken in a tax return. FIN No. 48 is effective for fiscal

years beginning after December 15, 2006. The Company does not believe the adoption of FIN No. 48 will have a material impact

on its consolidated financial statements.

In June 2006, the FASB’s Emerging Issues Task Force (“EITF”) reached a consensus on Issue No. 06-3, “How Taxes Collected from

Customers and Remitted to Governmental Authorities Should be Presented in the Income Statement (That Is, Gross versus Net

Presentation).” The scope of EITF 06-3 includes sales, use, value added and some excise taxes that are assessed by a governmental

authority on specific revenue-producing transactions between a seller and customer. EITF 06-3 requires disclosure of the method

of accounting for the applicable assessed taxes and the amount of assessed taxes that are included in revenues if they are

accounted for under the gross method. EITF 06-3 is effective for interim and annual periods beginning after December 15, 2006.

EITF 06-3 will not impact the method for recording these taxes in the Company’s consolidated financial statements as the

Company historically has presented sales excluding these taxes.

In October 2005, the FASB issued FASB Staff Position (“FSP”) 13-1, “Accounting for Rental Costs Incurred during a Construction

Period.” FSP 13-1 requires rental costs associated with ground or building operating leases that are incurred during a construction

period be recognized as rental expense. FSP 13-1 was effective for the first reporting period beginning after December 15, 2005.

The adoption of FSP 13-1 did not have a material impact on the Company’s consolidated financial statements.

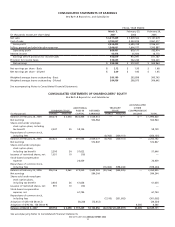

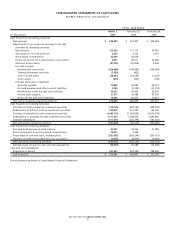

REVIEW OF EQUITY GRANTS AND PROCEDURES AND RELATED MATTERS

As a result of revised measurement dates for certain stock option grants, and the correction of various other errors, the Company

has determined that it had certain unrecorded non-cash equity-based compensation charges related to fiscal years prior to 2006.

(See “Recent Accounting Pronouncements-Staff Accounting Bulletin No. 108”). For fiscal 2006, the Company recorded $8.2 million

of expense related to the revised measurement dates.

The Company’s Board of Directors also approved a remediation program intended to protect over 1,600 employees from certain

potential adverse tax consequences. These adverse tax consequences arise pursuant to Internal Revenue Code Section 409A as

a result of historical deficiencies associated with certain of the Company’s stock option grants that were disclosed through the

Company’s stock option review. As a result of this program, the Company made cash payments totaling approximately $30.0 mil-

lion to over 1,600 employees in the fourth quarter of fiscal 2006, which resulted in a non-recurring, pre-tax stock-based compen-

sation charge. The cash outlay primarily represents payments to employees in connection with increasing the exercise prices on

certain stock option grants so as to protect them from certain potential adverse tax consequences. No executive officer received

such payments. The Company believes it is likely the Company will recoup a substantial portion of the anticipated cash outlay over

the next several years through higher proceeds from future stock option exercises, although this recovery would not flow through

the income statement.

The Company also filed a Form 8-K dated December 28, 2006 which provides further details regarding the remediation program.

The Company continues to cooperate with the informal inquiry of the SEC regarding the Company’s stock option grant practices.

In addition, the Company is also cooperating with the United States Attorney’s office for the District of New Jersey in connection

with its inquiry into such matters.

CRITICAL ACCOUNTING POLICIES

The preparation of consolidated financial statements in conformity with U.S. generally accepted accounting principles requires the

Company to establish accounting policies and to make estimates and judgments that affect the reported amounts of assets and

liabilities and disclosure of contingent assets and liabilities as of the date of the consolidated financial statements and the report-

ed amounts of revenues and expenses during the reporting period. The Company bases its estimates on historical experience

and on other assumptions that it believes to be relevant under the circumstances, the results of which form the basis for making

judgments about the carrying value of assets and liabilities that are not readily apparent from other sources. In particular,

judgment is used in areas such as the inventory valuation, impairment of long-lived assets, goodwill and other indefinitely lived

intangible assets, accruals for self insurance, litigation, store opening, expansion, relocation and closing costs, stock-based

compensation and income taxes. Actual results could differ from these estimates.