Air New Zealand 2011 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2011 Air New Zealand annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

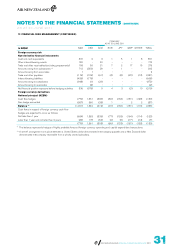

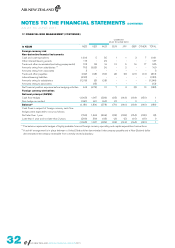

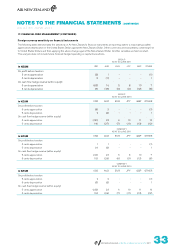

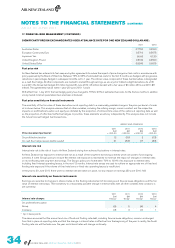

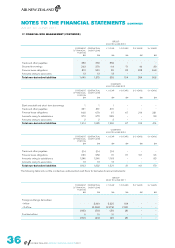

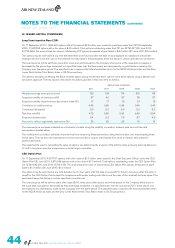

17. FINANCIAL RISK MANAGEMENT (CONTINUED)

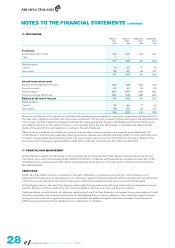

SIGNIFICANT FOREIGN EXCHANGE RATES USED AT BALANCE DATE FOR ONE NEW ZEALAND DOLLAR ARE:

2011 2010

Australian Dollar 0.7720 0.8150

European Community Euro 0.5710 0.5675

Japanese Yen 66.60 61.30

United Kingdom Pound 0.5130 0.4590

United States Dollar 0.8240 0.6915

Fuel price risk

Air New Zealand has entered into fuel swap and option agreements to reduce the impact of price changes on fuel costs in accordance with

policy approved by the Board of Directors. Between 75% to 95% of estimated fuel costs for the first 3 months are hedged, with progressive

reductions in percentages hedged in subsequent months out to 1 year. The intrinsic value component of these fuel derivatives is designated

as a cash flow hedge. All other components are marked to market through earnings, as are any short-dated outright derivatives. As at 30

June 2011, the Group had hedged 4.5 million barrels (30 June 2010: 4.8 million barrels) with a fair value of $6 million (30 June 2010: $8

million). The agreements mature within 1 year (30 June 2010: 1 year).

With effect from 1 July 2011, the fuel hedging policy has changed to 70% to 90% of estimated fuel costs for the first six months. In addition

unruly market minimum parameters have also been introduced.

Fuel price sensitivity on financial instruments

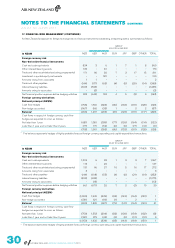

The sensitivity of the fair value of these derivatives as at reporting date to a reasonably possible change in the price per barrel of crude

oil is shown below. This analysis assumes that all other variables, including the refining margin, remain constant and the respective

impacts on profit before taxation and equity are dictated by the proportion of intrinsic/time value of the options at reporting date as well

as the proportion of effective/ineffective hedges. In practice, these elements would vary independently. This analysis does not include

the future forecast hedged fuel transactions.

GROUP AND COMPANY

Price movement per barrel:

2011

$M

+ USD 20

2011

$M

- USD 20

2010

$M

+ USD 20

2010

$M

- USD 20

On profit before taxation 12 (19) 2 (13)

On cash flow hedge reserve (within equity) 61 (53) 97 (83)

Interest rate risk

Interest rate risk is the risk of loss to Air New Zealand arising from adverse fluctuations in interest rates.

Air New Zealand has exposure to interest rate risk as a result of the long-term borrowing activities which are used to fund ongoing

activities. It is the Group’s policy to ensure the interest rate exposure is maintained to minimise the impact of changes in interest rates

on its net floating rate long-term borrowings. The Group’s policy is to fix between 70% to 100% of its exposure to interest rates,

including fixed interest operating leases, in the next 12 months. Interest rate swaps are used to achieve an appropriate mix of fixed and

floating rate exposure if the volume of fixed rate loans or fixed rate operating leases is insufficient.

In the year to 30 June 2011, there were no interest rate derivatives in place, nor any impact on earnings (30 June 2010: Nil).

Interest rate sensitivity on financial instruments

Earnings are sensitive to changes in interest rates on the floating rate element of borrowings and finance lease obligations and the fair

value of interest rate swaps. Their sensitivity to a reasonably possible change in interest rates with all other variables held constant, is

set out below:

Interest rate change:

2011

$M

+50 bp*

2011

$M

-50 bp*

2010

$M

+50 bp*

2010

$M

-50 bp*

On profit before taxation

Group (5) 5 (4) 4

Company (3) 3 (1) 1

* bp = basis points

The above assumes that the amount and mix of fixed and floating rate debt, including finance lease obligations, remains unchanged

from that in place at reporting date, and that the change in interest rates is effective from the beginning of the year. In reality, the fixed/

floating rate mix will fluctuate over the year and interest rates will change continually.

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

AS AT 30 JUNE 2011

AIR NEW ZEALAND ANNUAL FINANCIAL RESULTS 2011