Air New Zealand 2011 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2011 Air New Zealand annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

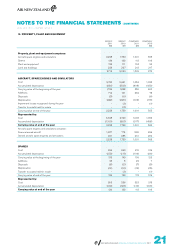

Financial Liabilities

Interest-bearing liabilities

Borrowings

Borrowings are initially recognised at fair value, net of transaction costs incurred. Borrowings are subsequently stated at amortised

cost using the effective interest rate method, where appropriate. Borrowings are classified as current liabilities unless the Group has an

unconditional right to defer settlement of the liability for more than 12 months after the balance sheet date.

Finance leases

Finance lease obligations are initially stated at fair value, net of transaction costs incurred. The obligations are subsequently stated at

amortised cost.

Trade and other payables

Trade and other payables are stated at cost.

DERIVATIVE FINANCIAL INSTRUMENTS

Air New Zealand uses derivative financial instruments to manage its exposure to foreign exchange, fuel price, and interest rate risks

arising from operational, financing and investment activities. Equity swaps were used to provide price protection in the event of a purchase

of shares in Virgin Blue Holdings Limited. Derivative financial instruments are recognised initially at fair value and transaction costs are

expensed immediately. Subsequent to initial recognition, derivative financial instruments are recognised as described below:

Derivative financial instruments at fair value through profit or loss

Derivative financial instruments, other than those designated as hedging instruments in a qualifying cash flow hedge (refer below), are

classified as held for trading. Subsequent to initial recognition, derivative financial instruments in this category are stated at fair value.

The gain or loss on remeasurement to fair value is recognised immediately in the Statement of Financial Performance.

Hedge accounted financial instruments

Where financial instruments qualify for hedge accounting in accordance with NZ IAS 39: Financial Instruments: Recognition and

Measurement, recognition of any resultant gain or loss depends on the nature of the hedging relationship, as detailed below.

Cash flow hedges

Changes in the fair value of hedging instruments designated as cash flow hedges are recognised within Other Comprehensive Income

and accumulated within equity to the extent that the hedges are deemed effective in accordance with NZ IAS 39: Financial Instruments:

Recognition and Measurement. To the extent that the hedges are ineffective for accounting, changes in fair value are recognised in the

Statement of Financial Performance.

If a hedging instrument no longer meets the criteria for hedge accounting, expires or is sold, terminated or exercised, or the designation of

the hedge relationship is revoked or changed, then hedge accounting is discontinued. The cumulative gain or loss previously recognised in

the cash flow hedge reserve remains there until the forecast transaction occurs. If the underlying hedged transaction is no longer expected

to occur, the cumulative, unrealised gain or loss recognised in the cash flow hedge reserve with respect to the hedging instrument is

recognised immediately in the Statement of Financial Performance.

Where the hedge relationship continues throughout its designated term, the amount recognised in the cash flow hedge reserve is

transferred to the Statement of Financial Performance in the same period that the hedged item is recorded in the Statement of Financial

Performance, or, when the hedged item is a non-financial asset, the amount recognised in the cash flow hedge reserve is transferred to the

carrying amount of the asset when it is recognised.

Net investment hedge

Hedges of net investments in foreign operations are accounted for similarly to cash flow hedges. Any gain or loss on the hedging

instrument relating to the effective portion of the hedge is recognised in other comprehensive income and accumulated in the foreign

currency translation reserve within equity. The gain or loss relating to the ineffective portion of the hedge is recognised immediately in

the Statement of Financial Performance.

Fair value estimation

The fair value of investments in quoted equity instruments is determined by reference to quoted market prices in an active market. This

equates to “Level 1” of the fair value hierarchy defined within “Amendments to NZ IFRS 7: Financial Instruments: Disclosures”. The fair

value of derivative financial instruments is based on published market prices for similar assets or liabilities at balance date (“Level 2” of

the fair value hierarchy). The fair value of interest-bearing liabilities for disclosure purposes is calculated based on the present value of

future principal and interest cash flows, discounted at the market rate of interest for similar liabilities at reporting date.

AIR NEW ZEALAND ANNUAL FINANCIAL RESULTS 2011

STATEMENT OF ACCOUNTING POLICIES (CONTINUED)

FOR THE YEAR TO 30 JUNE 2011