Air New Zealand 2008 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2008 Air New Zealand annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

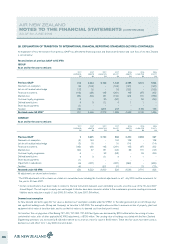

28. EXPLANATION OF TRANSITION TO INTERNATIONAL FINANCIAL REPORTING STANDARDS (NZ IFRS) (CONTINUED)

Jet aircraft residual value hedge

Under previous GAAP, the Group designated the USD denominated residual values of the jet aircraft fleet, engines, simulators and progress payments

as a hedge of related USD denominated borrowings and finance lease liabilities. NZ IFRS does not permit such a hedge. Therefore this accounting

treatment was reversed on transition to NZ IFRS.

Exchange gains and losses on USD borrowings and finance lease liabilities are recorded in the Statement of Financial Performance under NZ IFRS, but

are substantially offset, at a Group level, by movements in the fair value of non-hedge accounted foreign currency derivatives that are also recognised in

the Statement of Financial Performance and are included within the financial instruments adjustments.

Financial instruments

NZ IFRS requires the recognition of all derivatives at fair value through the Statement of Financial Performance, unless they are designated as part of a

cash flow hedge. Under previous GAAP, derivatives remained off balance sheet until the underlying hedged item was realised.

NZ IFRS requires strict criteria to be met in order to qualify for hedge accounting. Whilst Air New Zealand’s general hedging strategies are permissible

under NZ IFRS, certain changes have been made to enable these hedges to be designated as cash flow hedges. Risk management practices continue

to be determined on an economic basis, rather than being designed to achieve a particular accounting outcome. Consequently, it is expected that this

will result in some transactions failing the accounting hedge effectiveness criteria from time to time and hedging gains or losses being recorded in current

period earnings. In particular given the high volatility of fuel markets, the accounting effectiveness test may not always be met and changes in the fair

value of fuel hedging instruments would then need to be recognised in the Statement of Financial Performance and consequently, some earnings volatility

may arise. The accounting treatment of options also results in ineffectiveness being recognised through earnings, in accordance with NZ IAS 39. Only

the intrinsic value is included in the hedge designation - all other components of the option value are marked to market through earnings.

The impact on operating surplus before taxation includes the change in the fair value of non-hedge accounted foreign exchange contracts (substantially

offsetting, at Group level, the exchange impact on the reversal of the jet aircraft residual value hedge above), and interest rate swaps. The impact also

includes any accounting ineffectiveness on qualifying cash flow hedges.

The remaining movement in equity represents the effective gains or losses on qualifying cash flow hedges which were recognised in the cash flow hedge

reserve.

Maintenance

Under previous GAAP, Air New Zealand expensed all maintenance as incurred. The application of NZ IFRS in respect of accounting for aircraft and

related maintenance costs resulted in the following changes:

- Engines are accounted for as a separate component of aircraft and depreciated separately. The estimated useful life of engines was revised on

transition to NZ IFRS;

- The cost of major airframe inspections and engine overhauls is capitalised and recognised in the carrying amount of the asset. The capitalised amount

is depreciated over the period to the next expected inspection or overhaul. On transition to NZ IFRS, the appropriate carrying value of previously

expensed maintenance was reinstated on the Statement of Financial Position; and

- Where Air New Zealand has a commitment to maintain aircraft held under operating lease arrangements, provision is made during the lease term for

the lease return obligations specified within those lease agreements. The provision is based on estimated future costs of major inspections and engine

overhauls by making appropriate charges to the Statement of Financial Performance calculated by reference to the number of hours or cycles operated

during the year.

Customer Loyalty Programme

NZ IFRS requires separate recognition of award credits granted as part of an initial sales transaction. Accordingly the consideration allocated to

Air New Zealand’s Loyalty Programme must be measured by reference to their fair value. The release to revenue in future years will be determined by

the redemption profile of Airpoints.

Defined benefit plans

NZ IFRS requires actuarial valuations to use a different valuation methodology and a different discount rate to that employed under previous GAAP.

Air New Zealand applies the “corridor” approach whereby actuarial gains and losses are only recognised to the extent that they exceed 10 percent of the

greater of the scheme assets or liabilities. This excess is spread over the remaining average service lives of the employees.

Share based payments

Previous GAAP offered no guidance as to how to account for share based payments. NZ IFRS 2: Share-based Payment requires equity settled

transactions, such as the issue of share options to employees, to be recognised at fair value in the financial statements, over the vesting period.

AIR NEW ZEALAND

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

AS AT 30 JUNE 2008

47