Air New Zealand 2008 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2008 Air New Zealand annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

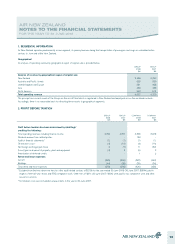

AIR NEW ZEALAND

STATEMENT OF ACCOUNTING POLICIES (CONTINUED)

Deferred income taxation is provided in full, using the balance sheet liability method, on temporary differences arising between the tax bases of assets

and liabilities and their carrying amounts in the financial statements. Deferred income tax is determined using tax rates (and laws) that have been

enacted or substantively enacted by the balance sheet date and are expected to apply when the related deferred income tax asset is realised or the

deferred income tax liability is settled.

Deferred income tax assets and unused tax losses are only recognised to the extent that it is probable that future taxable amounts will be available

against which to utilise those temporary differences and losses.

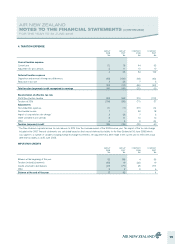

EMPLOYEE BENEFITS

Pension obligations

Payments to defined contribution retirement plans are charged as an expense as they fall due. Payments made to multi-employer retirement benefit

schemes are treated in the same way as payments to defined contribution schemes where sufficient information is not available to use defined benefit

accounting.

Air New Zealand’s net obligation in respect of defined benefit pension plans is calculated separately for each plan by an independent actuary, as being

the present value of the future obligations to the members less the fair value of the plan’s assets, adjusted for any unrecognised actuarial gains or losses

and unrecognised past service costs. The discount rate reflects the yield on government bonds that have maturity dates approximating the terms of

Air New Zealand’s obligations. When the calculation results in a benefit to Air New Zealand, the value of the asset recognised cannot exceed in

aggregate the value of any unrecognised net actuarial losses and past service cost, and the present value of any future refunds from the plan or

reductions in future contributions to the plan.

All cumulative actuarial gains and losses were recognised as at 1 July 2006 (transition date) in accordance with the available exemption under

NZ IFRS 1: First-time adoption of NZ IFRS. Any actuarial gains or losses since 1 July 2006 are amortised under the corridor method over the members’

expected average remaining working lives.

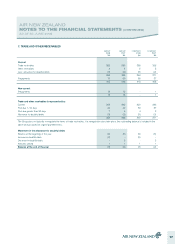

Share based compensation

All equity options are disclosed in the notes to the financial statements. The fair value (at grant date) of options granted to employees is recognised as

an expense, within the Statement of Financial Performance, over the vesting period of the options, with a corresponding entry to Issued Capital. The

amount recognised as an expense is adjusted at each reporting date to reflect the extent to which the vesting period has expired and management’s

best estimate of the number of share options that will ultimately vest.

In accordance with the exemption available under NZ IFRS 1: First-time adoption of NZ IFRS, Air New Zealand has applied the requirements of

NZ IFRS 2: Share-based Payment only to those options granted after 7 November 2002 that had not vested before 1 July 2006 (transition date).

Termination costs

Termination costs are recognised as an expense when the Group is demonstrably committed, without realistic possibility of withdrawal, to a formal

detailed plan to terminate employment before the normal termination date.

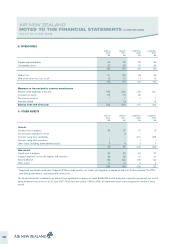

PROVISIONS

A provision is recognised when the Group has a present legal or constructive obligation as a result of a past event, it is probable that an outflow of

economic benefits will be required to settle the obligation, and the provision can be reliably measured.

12