Air New Zealand 2008 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2008 Air New Zealand annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

AIR NEW ZEALAND

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

FOR THE YEAR TO 30 JUNE 2008

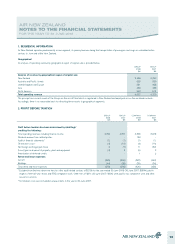

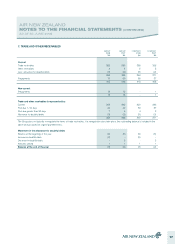

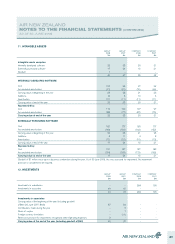

3. DERIVATIVE FINANCIAL INSTRUMENTS

Air New Zealand is subject to credit, foreign currency, interest rate, and fuel price risks. These risks are managed using various financial instruments,

based on policies approved regularly by the Board of directors. Air New Zealand’s objectives, policies and processes for managing these risks are

described more fully in note 16.

Derivatives are required to be recognised in the Statement of Financial Position at their fair market value, with subsequent changes in fair value being

recognised through earnings. Changes in the fair value of those derivatives which have been successfully designated as part of a cash flow hedge

relationship are recognised through the cash flow hedge reserve within equity, to the extent that they are effective. Any accounting ineffectiveness is

recognised through earnings.

NZ IAS 39: Financial Instruments: Recognition and Measurement requires hedge effectiveness to be determined for accounting purposes within strict

parameters. Each derivative transaction used to hedge identified risks must be documented and proven to be effective in offsetting changes in the value

of the underlying risk within a range of 80% - 125%. This measure of effectiveness may result in economically appropriate hedging transactions being

deemed ineffective for accounting purposes. In particular, the use of crude oil derivatives as a proxy for jet fuel, and the high volatility of fuel markets

may cause cash flow hedges in respect of fuel derivatives to fail the hedge effectiveness test.

Risk management practices are determined on an economic basis, rather than being designed to achieve a particular accounting outcome.

Consequently, it is expected that this will result in some transactions failing the accounting hedge effectiveness criteria from time to time and

ineffectiveness being recorded through earnings in periods other than when the hedged item occurs, causing some volatility through earnings.

Normalised earnings, disclosed as supplementary information at the foot of the Statement of Financial Performance, shows earnings before unusual

items and taxation after excluding movements on derivatives that hedge exposures in other financial periods. Such movements include amounts required

to be recognised as ineffective for accounting purposes.

Where changes in the fair value of a derivative provide a natural offset to the underlying hedged item as it impacts earnings, hedge accounting is not

applied. Both the changes in value of the hedged item and the hedging instrument are recognised through the same line within the Statement of

Financial Performance. Furthermore, some components of hedge accounted derivatives are excluded from the designated risk. Cash flow hedges in

respect of fuel derivatives only include the intrinsic value of the fuel options with all other components of the option value (mainly time value) being

marked to market through earnings. Similarly, forward points (the differential in interest rates between currencies) are excluded from the hedge

designation in respect of foreign currency derivatives which hedge account forecast foreign currency operating revenue and expenditure transactions.

These components are not hedge accounted and, accordingly, marked to market through earnings.

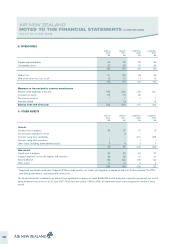

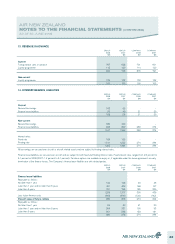

FOREIGN CURRENCY DERIVATIVES

Non-hedge accounted derivatives

Foreign currency translation gains or losses on lease return provisions (from 1 July 2007) and United States Dollar denominated interest-bearing

liabilities are recognised in the Statement of Financial Performance within “Other expenses”. Marked to market gains or losses on non-hedge accounted

foreign currency derivatives provide a natural offset to these foreign exchange movements, and are also recognised within “Other expenses”. Derivatives

were put in place to manage the exposure on the lease return provision with effect from 1 July 2007.

During the year to 30 June 2008, a gain of $12 million was recognised in respect of the above non-hedge accounted foreign currency derivatives

(30 June 2007: $183 million loss), which was offset by exchange movements on the underlying exposure. Forward point costs of $43 million in respect

of these derivatives were marked to market through “Finance costs” in the year to 30 June 2008 (30 June 2007: $11 million of costs).

Hedge accounted derivatives

The Group hedge accounts the foreign currency risk arising on forecast foreign currency operating revenue, operating expense and capital expenditure

transactions.

Forward points are excluded from the hedge designation in respect of operating revenue and expenditure transactions and are marked to market through

earnings. Forward point costs of $33 million in respect of these derivatives were marked to market through “Finance costs” in the year to 30 June 2008

(30 June 2007: $16 million of costs).

Accounting ineffectiveness arising in the year to 30 June 2008 on these cash flow hedges was a loss of $1 million on operating transactions and a loss

of $25 million on capital transactions (30 June 2007: $4 million loss on operating transactions; $3 million loss on capital transactions).

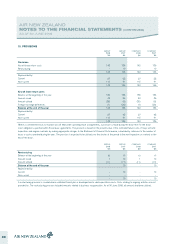

FUEL DERIVATIVES

The Group uses crude oil derivatives to hedge price risk in jet fuel. The intrinsic value component of these fuel derivatives is designated as a cash flow

hedge. All other components are marked to market through earnings, as are any short-dated outright derivatives. In the year to 30 June 2008, gains of

$9 million were recognised within “Fuel” (30 June 2007: $39 million loss). Hedge accounting was not applied to fuel derivatives in the first six months of

the year to 30 June 2007.

Accounting ineffectiveness arising in the year to 30 June 2008 of $171 million (gain) was recognised within “Fuel” (30 June 2007: $8 million gain).

INTEREST RATE DERIVATIVES

Interest rate derivatives are not hedge accounted. Changes in the fair value of these derivatives are recognised each period within “Finance costs”. In the

year to 30 June 2008 a loss of $2 million was recognised (30 June 2007: $9 million loss) in respect of non-hedge accounted interest rate derivatives.

14