The Hartford 2008 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2008 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

-

565

-

566

-

567

-

568

-

569

-

570

-

571

-

572

-

573

-

574

-

575

-

576

-

577

-

578

-

579

-

580

-

581

-

582

-

583

-

584

-

585

-

586

-

587

-

588

-

589

-

590

-

591

-

592

-

593

-

594

-

595

-

596

-

597

-

598

-

599

-

600

-

601

-

602

-

603

-

604

-

605

-

606

-

607

-

608

-

609

-

610

-

611

-

612

-

613

-

614

-

615

-

616

-

617

-

618

-

619

-

620

-

621

-

622

-

623

-

624

-

625

-

626

-

627

-

628

-

629

-

630

-

631

-

632

-

633

-

634

-

635

-

636

-

637

-

638

-

639

-

640

-

641

-

642

-

643

-

644

-

645

-

646

-

647

-

648

-

649

-

650

-

651

-

652

-

653

-

654

-

655

-

656

-

657

-

658

-

659

-

660

-

661

-

662

-

663

-

664

-

665

-

666

-

667

-

668

-

669

-

670

-

671

-

672

-

673

-

674

-

675

-

676

-

677

-

678

-

679

-

680

-

681

-

682

-

683

-

684

-

685

-

686

-

687

-

688

-

689

-

690

-

691

-

692

-

693

-

694

-

695

-

696

-

697

-

698

-

699

-

700

-

701

-

702

-

703

-

704

-

705

-

706

-

707

-

708

-

709

-

710

-

711

-

712

-

713

-

714

-

715

-

716

-

717

-

718

-

719

-

720

-

721

-

722

-

723

-

724

-

725

-

726

-

727

-

728

-

729

-

730

-

731

-

732

-

733

-

734

-

735

-

736

-

737

-

738

-

739

-

740

-

741

-

742

-

743

-

744

-

745

-

746

-

747

-

748

-

749

-

750

-

751

-

752

-

753

-

754

-

755

-

756

-

757

-

758

-

759

-

760

-

761

-

762

-

763

-

764

-

765

-

766

-

767

-

768

-

769

-

770

-

771

-

772

-

773

-

774

-

775

-

776

-

777

-

778

-

779

-

780

-

781

-

782

-

783

-

784

-

785

-

786

-

787

-

788

-

789

-

790

-

791

-

792

-

793

-

794

-

795

-

796

-

797

-

798

-

799

-

800

-

801

-

802

-

803

-

804

-

805

-

806

-

807

-

808

-

809

-

810

-

811

-

812

-

813

-

814

-

815

|

|

Table of Contents

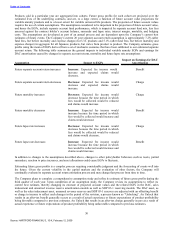

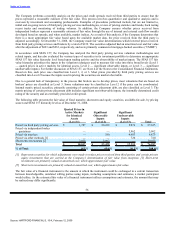

[3] The overall actual return generated by the U.S. variable annuity separate accounts is dependent on several factors,

including the relative mix of the underlying sub-accounts among bond funds and equity funds as well as equity sector

weightings and as a result of the large proportion of separate account assets invested in U.S. equity markets, the

Company’s overall U.S. separate account fund performance has been reasonably correlated to the overall performance

of the S&P 500 although no assurance can be provided that this correlation will continue in the future. Since

September 30, 2008, the date of the last unlock, the actual return on U.S. variable annuity assets has been 21% below

our estimated aggregate return. The Company estimates the actual return would need to drop by an additional 6% since

December 31, 2008, before EGPs in the Company’s models fall outside of the statistical ranges of reasonable EGPs.

[4] The overall actual return generated by the Japan variable annuity separate accounts is influenced by the variable

annuity products offered in Japan as well as the wide variety of funds offered within the sub-accounts of those

products. The actual return is also dependent upon the relative mix of the underlying sub-accounts among the funds.

Unlike in the U.S., there is no global index or market that reasonably correlates with the overall Japan actual separate

account fund performance. Since September 30, 2008, the date of the last unlock, the actual return on Japan variable

annuity assets has been 15.5% below our estimated aggregate return. The Company estimates the actual return would

need to drop by an additional 7.5% since December 31, 2008, before EGPs in the Company’s models fall outside of the

statistical ranges of reasonable EGPs.

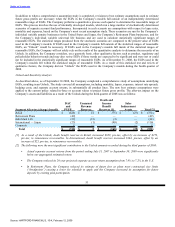

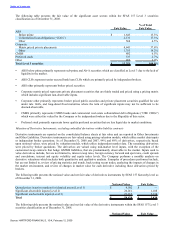

[5] For the Company’s 3Win product in Japan, decreases in the contract holder’s account value (which is partially

dependent upon equity market movements due to fixed contractual investment allocations) of greater than 20% of the

initial deposit require the contract holder to withdraw 80% of their initial deposit without penalty or recover their initial

investment through a payout annuity. The exercise of these options results in an acceleration of the amount of DAC

amortization in a specific reporting period. During the fourth quarter of 2008 approximately 97% of all 3Win

contractholders had account values that fell by 20% or more from their initial deposit. This resulted in accelerated

amortization of DAC in the fourth quarter of 2008 of $194, pre-tax. Further declines in equity markets during 2009

could cause the entire remaining DAC balance of $11 to be amortized.

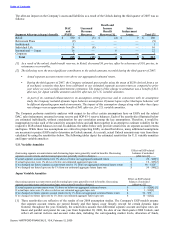

An “Unlock” only revises EGPs to reflect current best estimate assumptions. With or without an Unlock, and even after an

Unlock occurs, the Company must also test the aggregate recoverability of the DAC and sales inducement assets by

comparing the existing DAC balance to the present value of future EGPs. In addition, the Company routinely stress tests its

DAC and sales inducement assets for recoverability against severe declines in its separate account assets, which could occur

if the equity markets experienced a significant sell-off, as the majority of policyholders’ funds in the separate accounts is

invested in the equity market. As of December 31, 2008, the Company believed U.S. individual and Japan individual

variable annuity EGPs could fall, through a combination of negative market returns, lapses and mortality, by at least 6% and

49%, respectively, before portions of its DAC and sales inducement assets would be unrecoverable. The extent of the charge

against earnings upon the DAC and sales inducement assets becoming unrecoverable is dependent upon how much further

beyond the thresholds listed above variable annuity EGPs decline. The Company estimates that for every 1% decline in

variable annuity EGPs beyond the thresholds listed above, the DAC and sales inducements write-off would be $65 and $12,

after-tax, for U.S. variable annuity and Japan variable annuity, respectively. If, at the end of any quarter, the EGPs in the

Company’s models fall outside of the statistical ranges of reasonable EGPs, see footnote [3] above, and the Company has

exceeded the threshold for recoverability, the Company will first “Unlock” the future EGPs to reflect the Company’s revised

best estimates and second will re-test for recoverability.

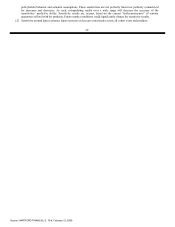

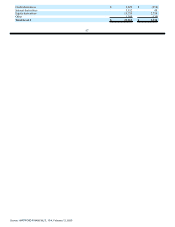

Living Benefits Required to be Fair Valued

The Company offers certain variable annuity products with a guaranteed minimum withdrawal benefit (“GMWB”) rider in

the U.S., Japan and the U.K. The Company also offers a guaranteed minimum accumulation benefit (“GMAB”) with a

variable annuity product offered in Japan. As of December 31, 2008 and December 31, 2007, the fair values of the GMWB

liabilities are $6.6 billion and $715, respectively. As of December 31, 2008 the fair value of the GMAB liability is $0. As of

December 31, 2007 the fair value of the GMAB was an asset of $2 because the present value of the fees expected to be

earned in the future exceeded the present value claims expected to be paid in the future. Due to significant market declines

in the fourth quarter of 2008, a large majority of the Company’s in force Japan 3 Win policies, which include a GMAB

feature, annuitized or surrendered free of charge in the fourth quarter of 2008. See Note 4 of Notes to Consolidated Financial

Statements for a description of the Japan GMAB.

Fair values for GMWB and GMAB contracts are calculated based upon internally developed models because active,

observable markets do not exist for those items. Below is a description of the Company’s fair value methodologies for

guaranteed benefit liabilities, the related reinsurance and customized derivatives, all accounted for under SFAS 133, prior to

the adoption of SFAS 157 and subsequent to adoption of SFAS 157.

53

Source: HARTFORD FINANCIAL S, 10-K, February 12, 2009