The Hartford 2008 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2008 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

-

565

-

566

-

567

-

568

-

569

-

570

-

571

-

572

-

573

-

574

-

575

-

576

-

577

-

578

-

579

-

580

-

581

-

582

-

583

-

584

-

585

-

586

-

587

-

588

-

589

-

590

-

591

-

592

-

593

-

594

-

595

-

596

-

597

-

598

-

599

-

600

-

601

-

602

-

603

-

604

-

605

-

606

-

607

-

608

-

609

-

610

-

611

-

612

-

613

-

614

-

615

-

616

-

617

-

618

-

619

-

620

-

621

-

622

-

623

-

624

-

625

-

626

-

627

-

628

-

629

-

630

-

631

-

632

-

633

-

634

-

635

-

636

-

637

-

638

-

639

-

640

-

641

-

642

-

643

-

644

-

645

-

646

-

647

-

648

-

649

-

650

-

651

-

652

-

653

-

654

-

655

-

656

-

657

-

658

-

659

-

660

-

661

-

662

-

663

-

664

-

665

-

666

-

667

-

668

-

669

-

670

-

671

-

672

-

673

-

674

-

675

-

676

-

677

-

678

-

679

-

680

-

681

-

682

-

683

-

684

-

685

-

686

-

687

-

688

-

689

-

690

-

691

-

692

-

693

-

694

-

695

-

696

-

697

-

698

-

699

-

700

-

701

-

702

-

703

-

704

-

705

-

706

-

707

-

708

-

709

-

710

-

711

-

712

-

713

-

714

-

715

-

716

-

717

-

718

-

719

-

720

-

721

-

722

-

723

-

724

-

725

-

726

-

727

-

728

-

729

-

730

-

731

-

732

-

733

-

734

-

735

-

736

-

737

-

738

-

739

-

740

-

741

-

742

-

743

-

744

-

745

-

746

-

747

-

748

-

749

-

750

-

751

-

752

-

753

-

754

-

755

-

756

-

757

-

758

-

759

-

760

-

761

-

762

-

763

-

764

-

765

-

766

-

767

-

768

-

769

-

770

-

771

-

772

-

773

-

774

-

775

-

776

-

777

-

778

-

779

-

780

-

781

-

782

-

783

-

784

-

785

-

786

-

787

-

788

-

789

-

790

-

791

-

792

-

793

-

794

-

795

-

796

-

797

-

798

-

799

-

800

-

801

-

802

-

803

-

804

-

805

-

806

-

807

-

808

-

809

-

810

-

811

-

812

-

813

-

814

-

815

|

|

Table of Contents

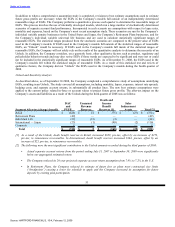

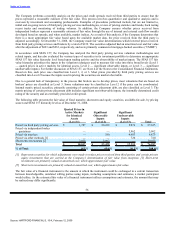

The after-tax impact on the Company’s assets and liabilities as a result of the Unlock during the third quarter of 2007 was as

follows:

Death and

DAC Unearned Income Sales

and Revenue Benefit Inducement

Segment After-tax (charge) benefit PVFP Reserves Reserves [1] Assets Total [2]

Retail $ 180 $ (5) $ (4) $ 9 $ 180

Retirement Plans (9) — — — (9)

Institutional 1 — — — 1

Individual Life 24 (8) — — 16

International — Japan 16 — 6 — 22

Corporate 3 — — — 3

Total $ 215 $ (13) $ 2 $ 9 $ 213

[1] As a result of the unlock, death benefit reserves, in Retail, decreased $4, pre-tax, offset by a decrease of $10, pre-tax, in

reinsurance recoverables.

[2] The following were the most significant contributors to the unlock amounts recorded during the third quarter of 2007:

• Actual separate account returns were above our aggregated estimated return.

• During the third quarter of 2007, the Company estimated gross profits using the mean of EGPs derived from a set

of stochastic scenarios that have been calibrated to our estimated separate account return as compared to prior

year where we used a single deterministic estimation. The impact of this change in estimation was a benefit of $13,

after-tax, for Japan variable annuities and $20, after-tax, for U.S. variable annuities.

• As part of its continual enhancement to its assumption setting processes and in connection with its assumption

study, the Company included dynamic lapse behavior assumptions. Dynamic lapses reflect that lapse behavior will

be different depending upon market movements. The impact of this assumption change along with other base lapse

rate changes was an approximate benefit of $40, after-tax, for U.S. variable annuities.

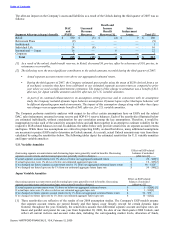

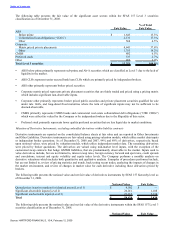

The Company performs sensitivity analyses with respect to the effect certain assumptions have on EGPs and the related

DAC, sales inducement, unearned revenue reserve and SOP 03-1 reserve balances. Each of the sensitivities illustrated below

are estimated individually, without consideration for any correlation among the key assumptions. Therefore, it would be

inappropriate to take each of the sensitivity amounts below and add them together in an attempt to estimate volatility for the

respective EGP-related balances in total. In addition, the tables below only provide sensitivities on separate account returns

and lapses. While those two assumptions are critical in projecting EGPs, as described above, many additional assumptions

are necessary to project EGPs and to determine an Unlock amount. As a result, actual Unlock amounts may vary from those

calculated by using the sensitivities below. The following tables depict the estimated sensitivities for U.S. variable annuities

and Japan variable annuities:

U.S. Variable Annuities

Effect on EGP-related

(Increasing separate account returns and decreasing lapse rates generally result in benefits. Decreasing balances if unlocked

separate account returns and increasing lapse rates generally result in charges.) (after-tax) [1]

If actual separate account returns were 1% above or below our aggregated estimated return $ 20 – $40[3]

If actual lapse rates were 1% above or below our estimated aggregate lapse rate $ 10 – $25[2]

If we changed our future separate account return rate by 1% from our aggregated estimated future return $ 90 – $120

If we changed our future lapse rate by 1% from our estimated aggregate future lapse rate $ 50 – $80[2]

Japan Variable Annuities

Effect on EGP-related

(Increasing separate account returns and decreasing lapse rates generally result in benefits. Decreasing balances if unlocked

separate account returns and increasing lapse rates generally result in charges.) (after-tax) [1]

If actual separate account returns were 1% above or below our aggregated estimated return $ 5 – $20[4] [5]

If actual lapse rates were 1% above or below our estimated aggregate lapse rate $ 1 – $10[2]

If we changed our future separate account return rate by 1% from our aggregated estimated future return $ 50 – $70

If we changed our future lapse rate by 1% from our estimated aggregate future lapse rate $ 10 – $25[2]

[1] These sensitivities are reflective of the results of our 2008 assumption studies. The Company’s EGP models assume

that separate account returns are earned linearly and that lapses occur linearly (except for certain dynamic lapse

features) throughout the year. Similarly, the sensitivities assume that differential separate account and lapse rates are

linear and parallel and persist for one year from September 30, 2008, the date of our third quarter 2008 Unlock, and

reflect all current in-force and account value data, including the corresponding market levels, allocation of funds,

Source: HARTFORD FINANCIAL S, 10-K, February 12, 2009