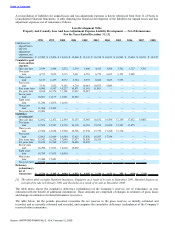

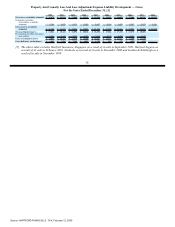

The Hartford 2008 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2008 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

-

565

-

566

-

567

-

568

-

569

-

570

-

571

-

572

-

573

-

574

-

575

-

576

-

577

-

578

-

579

-

580

-

581

-

582

-

583

-

584

-

585

-

586

-

587

-

588

-

589

-

590

-

591

-

592

-

593

-

594

-

595

-

596

-

597

-

598

-

599

-

600

-

601

-

602

-

603

-

604

-

605

-

606

-

607

-

608

-

609

-

610

-

611

-

612

-

613

-

614

-

615

-

616

-

617

-

618

-

619

-

620

-

621

-

622

-

623

-

624

-

625

-

626

-

627

-

628

-

629

-

630

-

631

-

632

-

633

-

634

-

635

-

636

-

637

-

638

-

639

-

640

-

641

-

642

-

643

-

644

-

645

-

646

-

647

-

648

-

649

-

650

-

651

-

652

-

653

-

654

-

655

-

656

-

657

-

658

-

659

-

660

-

661

-

662

-

663

-

664

-

665

-

666

-

667

-

668

-

669

-

670

-

671

-

672

-

673

-

674

-

675

-

676

-

677

-

678

-

679

-

680

-

681

-

682

-

683

-

684

-

685

-

686

-

687

-

688

-

689

-

690

-

691

-

692

-

693

-

694

-

695

-

696

-

697

-

698

-

699

-

700

-

701

-

702

-

703

-

704

-

705

-

706

-

707

-

708

-

709

-

710

-

711

-

712

-

713

-

714

-

715

-

716

-

717

-

718

-

719

-

720

-

721

-

722

-

723

-

724

-

725

-

726

-

727

-

728

-

729

-

730

-

731

-

732

-

733

-

734

-

735

-

736

-

737

-

738

-

739

-

740

-

741

-

742

-

743

-

744

-

745

-

746

-

747

-

748

-

749

-

750

-

751

-

752

-

753

-

754

-

755

-

756

-

757

-

758

-

759

-

760

-

761

-

762

-

763

-

764

-

765

-

766

-

767

-

768

-

769

-

770

-

771

-

772

-

773

-

774

-

775

-

776

-

777

-

778

-

779

-

780

-

781

-

782

-

783

-

784

-

785

-

786

-

787

-

788

-

789

-

790

-

791

-

792

-

793

-

794

-

795

-

796

-

797

-

798

-

799

-

800

-

801

-

802

-

803

-

804

-

805

-

806

-

807

-

808

-

809

-

810

-

811

-

812

-

813

-

814

-

815

|

|

Table of Contents

The markets in the United States and elsewhere have been experiencing extreme and unprecedented volatility and

disruption. We are exposed to significant financial and capital markets risk, including changes in interest rates, credit

spreads, equity prices, and foreign exchange rates which may have a material adverse effect on our results of operations,

financial condition and liquidity.

The markets in the United States and elsewhere have been experiencing and are expected to continue to experience extreme

and unprecedented volatility and disruption. We are exposed to significant financial and capital markets risk, including

changes in interest rates, credit spreads, equity prices and foreign currency exchange rates.

One important exposure to equity risk relates to the potential for lower earnings associated with certain of our Life

businesses, such as variable annuities, where fee income is earned based upon the fair value of the assets under management.

During the course of 2008, the significant declines in equity markets have negatively impacted assets under management. As

a result, fee income earned from those assets has also been negatively impacted. In addition, certain of our Life products

offer guaranteed benefits which increase our potential obligation and statutory capital exposure should equity markets

decline. Due to declines in equity markets during 2008, our liability for these guaranteed benefits has significantly increased

and our statutory capital position has decreased. Further sustained declines in equity markets during 2009 may result in the

need to devote significant additional capital to support these products. We are also exposed to interest rate and equity risk

based upon the discount rate and expected long-term rate of return assumptions associated with our pension and other

post-retirement benefit obligations. Sustained declines in long-term interest rates or equity returns are likely to have a

negative effect on the funded status of these plans.

Our exposure to interest rate risk relates primarily to the market price and cash flow variability associated with changes in

interest rates. A rise in interest rates, in the absence of other countervailing changes, will increase the net unrealized loss

position of our investment portfolio and, if long-term interest rates rise dramatically within a six to twelve month time

period, certain of our Life businesses may be exposed to disintermediation risk. Disintermediation risk refers to the risk that

our policyholders may surrender their contracts in a rising interest rate environment, requiring us to liquidate assets in an

unrealized loss position. Due to the long-term nature of the liabilities associated with certain of our Life businesses, such as

structured settlements and guaranteed benefits on variable annuities, sustained declines in long term interest rates may

subject us to reinvestment risks and increased hedging costs. In other situations, declines in interest rates or changes in credit

spreads may result in reducing the duration of certain Life liabilities, creating asset liability duration mismatches and lower

spread income.

Our exposure to credit spreads primarily relates to market price and cash flow variability associated with changes in credit

spreads. The recent widening of credit spreads has contributed to the increase in the net unrealized loss position of our

investment portfolio of $12.5 billion in 2008, before DAC effects and tax, and has also contributed to the increase in other

than temporary impairments. If issuer credit spreads continue to widen significantly over an extended period of time, it

would likely exacerbate these effects, resulting in greater and additional other-than-temporary impairments. Increased losses

have also occurred associated with credit based non-qualifying derivatives where the Company assumes credit exposure. If

credit spreads tighten significantly, it will reduce net investment income associated with new purchases of fixed maturities.

In addition, a reduction in market liquidity has made it difficult to value certain of our securities as trading has become less

frequent. As such, valuations may include assumptions or estimates that may be more susceptible to significant period to

period changes which could have a material adverse effect on our consolidated results of operations or financial condition.

Our statutory surplus is also impacted by widening credit spreads as a result of the accounting for the assets and liabilities on

our fixed market value adjusted (“MVA”) annuities. Statutory separate account assets supporting the fixed MVA annuities

are recorded at fair value. In determining the statutory reserve for the fixed MVA annuities we are required to use current

crediting rates in the U.S. and Japanese LIBOR in Japan. In many capital market scenarios, current crediting rates in the

U.S. are highly correlated with market rates implicit in the fair value of statutory separate account assets. As a result, the

change in the statutory reserve from period to period will likely substantially offset the change in the fair value of the

statutory separate account assets. However, in periods of volatile credit markets, such as we are now experiencing, actual

credit spreads on investment assets may increase sharply for certain sub-sectors of the overall credit market, resulting in

statutory separate account asset market value losses. As actual credit spreads are not fully reflected in current crediting rates

in the U.S. or Japanese LIBOR in Japan, the calculation of statutory reserves will not substantially offset the change in fair

value of the statutory separate account assets resulting in reductions in statutory surplus. This has resulted and may continue

to result in the need to devote significant additional capital to support the product.

Our primary foreign currency exchange risks are related to net income from foreign operations, non–U.S. dollar

denominated investments, investments in foreign subsidiaries, our yen-denominated individual fixed annuity product, and

certain guaranteed benefits associated with the Japan and U.K. variable annuities. These risks relate to potential decreases in

value and income resulting from a strengthening or weakening in foreign exchange rates versus the U.S. dollar. In general,

the weakening of foreign currencies versus the U.S. dollar will unfavorably affect net income from foreign operations, the

value of non-U.S. dollar denominated investments, investments in foreign subsidiaries and realized gains or losses on the

yen denominated individual fixed annuity product. In comparison, a strengthening of the Japanese yen or British pound in

comparison to the U.S. dollar and other currencies will increase our exposure to the guarantee benefits associated with the

Japan or U.K. variable annuities. Correspondingly, a strengthening of the U.S. dollar compared to other currencies will

Source: HARTFORD FINANCIAL S, 10-K, February 12, 2009