The Hartford 2008 Annual Report Download - page 175

Download and view the complete annual report

Please find page 175 of the 2008 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

-

565

-

566

-

567

-

568

-

569

-

570

-

571

-

572

-

573

-

574

-

575

-

576

-

577

-

578

-

579

-

580

-

581

-

582

-

583

-

584

-

585

-

586

-

587

-

588

-

589

-

590

-

591

-

592

-

593

-

594

-

595

-

596

-

597

-

598

-

599

-

600

-

601

-

602

-

603

-

604

-

605

-

606

-

607

-

608

-

609

-

610

-

611

-

612

-

613

-

614

-

615

-

616

-

617

-

618

-

619

-

620

-

621

-

622

-

623

-

624

-

625

-

626

-

627

-

628

-

629

-

630

-

631

-

632

-

633

-

634

-

635

-

636

-

637

-

638

-

639

-

640

-

641

-

642

-

643

-

644

-

645

-

646

-

647

-

648

-

649

-

650

-

651

-

652

-

653

-

654

-

655

-

656

-

657

-

658

-

659

-

660

-

661

-

662

-

663

-

664

-

665

-

666

-

667

-

668

-

669

-

670

-

671

-

672

-

673

-

674

-

675

-

676

-

677

-

678

-

679

-

680

-

681

-

682

-

683

-

684

-

685

-

686

-

687

-

688

-

689

-

690

-

691

-

692

-

693

-

694

-

695

-

696

-

697

-

698

-

699

-

700

-

701

-

702

-

703

-

704

-

705

-

706

-

707

-

708

-

709

-

710

-

711

-

712

-

713

-

714

-

715

-

716

-

717

-

718

-

719

-

720

-

721

-

722

-

723

-

724

-

725

-

726

-

727

-

728

-

729

-

730

-

731

-

732

-

733

-

734

-

735

-

736

-

737

-

738

-

739

-

740

-

741

-

742

-

743

-

744

-

745

-

746

-

747

-

748

-

749

-

750

-

751

-

752

-

753

-

754

-

755

-

756

-

757

-

758

-

759

-

760

-

761

-

762

-

763

-

764

-

765

-

766

-

767

-

768

-

769

-

770

-

771

-

772

-

773

-

774

-

775

-

776

-

777

-

778

-

779

-

780

-

781

-

782

-

783

-

784

-

785

-

786

-

787

-

788

-

789

-

790

-

791

-

792

-

793

-

794

-

795

-

796

-

797

-

798

-

799

-

800

-

801

-

802

-

803

-

804

-

805

-

806

-

807

-

808

-

809

-

810

-

811

-

812

-

813

-

814

-

815

|

|

Table of Contents

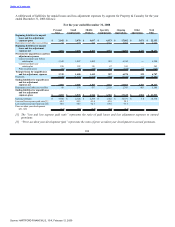

Investment yield and average invested assets

• In 2007, the after-tax investment yield increased due to a higher yield on limited partnerships and other alternative

investments and mortgage loans as well as due to a change in asset mix, including shifting a greater share of

investments to these asset classes.

• The average annual invested assets at cost increased as a result of positive operating cash flows and an increase in

collateral held from increased securities lending activities.

How Property & Casualty seeks to earn income

Net income is a measure of profit or loss used in evaluating the performance of Total Property & Casualty and the Ongoing

Operations and Other Operations segments. Within Ongoing Operations, the underwriting segments of Personal Lines,

Small Commercial, Middle Market and Specialty Commercial are evaluated by The Hartford’s management primarily based

upon underwriting results. Underwriting results within Ongoing Operations are influenced significantly by changes in

earned premium and the adequacy of the Company’s pricing. Underwriting profitability over time is also greatly influenced

by the Company’s underwriting discipline, which seeks to manage exposure to loss through favorable risk selection and

diversification, its management of claims, its use of reinsurance and its ability to manage its expense ratio which it

accomplishes through economies of scale and its management of acquisition costs and other underwriting expenses.

Pricing adequacy depends on a number of factors, including the ability to obtain regulatory approval for rate changes, proper

evaluation of underwriting risks, the ability to project future loss cost frequency and severity based on historical loss

experience adjusted for known trends, the Company’s response to rate actions taken by competitors, and expectations about

regulatory and legal developments and expense levels. Property & Casualty seeks to price its insurance policies such that

insurance premiums and future net investment income earned on premiums received will cover underwriting expenses and

the ultimate cost of paying claims reported on the policies and provide for a profit margin. For many of its insurance

products, Property & Casualty is required to obtain approval for its premium rates from state insurance departments.

In setting its pricing, Property & Casualty assumes an expected level of losses from natural or man-made catastrophes that

will cover the Company’s exposure to catastrophes over the long-term. In most years, however, Property & Casualty’s

actual losses from catastrophes will be more or less than that assumed in its pricing due to the significant volatility of

catastrophe losses. Insurance Services Office, Inc. (“ISO”) defines a catastrophe loss as an event that causes $25 or more in

industry insured property losses and affects a significant number of property and casualty policyholders and insurers.

Given the lag in the period from when claims are incurred to when they are reported and paid, final claim settlements may

vary from current estimates of incurred losses and loss expenses, particularly when those payments may not occur until well

into the future. Reserves for lines of business with a longer lag (or “tail”) in reporting are more difficult to estimate. Reserve

estimates for longer tail lines are initially set based on loss and loss expense ratio assumptions estimated when the business

was priced and are adjusted as the paid and reported claims develop, indicating that the ultimate loss and loss expense ratio

will differ from the initial assumptions. Adjustments to previously established loss and loss expense reserves, if any, are

reflected in underwriting results in the period in which the adjustment is determined to be necessary.

The investment return, or yield, on Property & Casualty’s invested assets is an important element of the Company’s earnings

since insurance products are priced with the assumption that premiums received can be invested for a period of time before

loss and loss adjustment expenses are paid. For longer tail lines, such as workers’ compensation and general liability, claims

are paid over several years and, therefore, the premiums received for these lines of business can generate significant

investment income. Due to the need to maintain sufficient liquidity to satisfy claim obligations, the vast majority of Property

& Casualty’s invested assets have been held in fixed maturities, including, among other asset classes, corporate bonds,

municipal bonds, government debt, short-term debt, mortgage-backed securities and asset-backed securities.

Through its Other Operations segment, Property & Casualty is responsible for managing operations of The Hartford that

have discontinued writing new or renewal business as well as managing the claims related to asbestos and environmental

exposures.

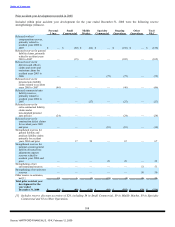

Definitions of key ratios and measures

Written and earned premiums

Written premium is a statutory accounting financial measure which represents the amount of premiums charged for policies

issued, net of reinsurance, during a fiscal period. Earned premium is a U.S. GAAP and statutory measure. Premiums are

considered earned and are included in the financial results on a pro rata basis over the policy period. Management believes

that written premium is a performance measure that is useful to investors as it reflects current trends in the Company’s sale

of property and casualty insurance products. Written and earned premium are recorded net of ceded reinsurance premium.

Reinstatement premiums

Source: HARTFORD FINANCIAL S, 10-K, February 12, 2009