Tesco 2012 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2012 Tesco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

|

|

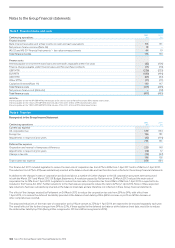

Notes to the Group financial statements

The associated cumulative gain or loss is reclassified from the other

comprehensive income and recognised in the Group Income Statement

in the same period or periods during which the hedged transaction

affects the Group Income Statement. The classification of the effective

portion when recognised in the Group Income Statement is the same

as the classification of the hedged transaction. Any element of the

remeasurement of the derivative instrument which does not meet the

criteria for an effective hedge is recognised immediately in the Group

Income Statement within finance income or costs.

Hedge accounting is discontinued when the hedging instrument expires

or is sold, terminated or exercised, or no longer qualifies for hedge

accounting. At that point in time, any cumulative gain or loss on the

hedging instrument recognised in equity is retained in the Group

Statement of Changes in Equity until the forecasted transaction occurs

or the original hedged item affects the Group Income Statement. If a

forecasted hedged transaction is no longer expected to occur, the net

cumulative gain or loss recognised in the Group Statement of Changes

in Equity is reclassified to the Group Income Statement.

Net investment hedging

Derivative financial instruments are classified as net investment hedges

when they hedge the Group’s net investment in an overseas operation.

The effective element of any foreign exchange gain or loss from

remeasuring the derivative instrument is recognised directly in other

comprehensive income. Any ineffective element is recognised immediately

in the Group Income Statement. Gains and losses accumulated in other

comprehensive income are included in the Group Income Statement when

the foreign operation is disposed of.

Treatment of agreements to acquire non-controlling interests

The Group has entered into a number of agreements to purchase the

remaining shares of subsidiaries with non-controlling interests.

The net present value of the expected future payments are shown as a

financial liability. At the end of each period, the valuation of the liability is

reassessed with any changes recognised in the Group Income Statement

within finance income or costs.

Provisions

Provisions are measured at the present value of the expenditures expected

to be required to settle the obligation using a pre-tax rate that reflects

current market assessments of the time value of money and the risks

specific to the obligation. The increase in the provision due to passage

of time is recognised as interest expense.

Provisions for onerous leases are recognised when the Group believes

that the unavoidable costs of meeting the lease obligations exceed the

economic benefits expected to be received under the lease. Provisions

for dilapidation costs are recognised on a lease by lease basis.

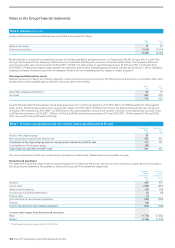

Other recent accounting developments

As of the date of authorisation of these financial statements, the following

standards were in issue but not yet effective and not yet been endorsed by

the EU. The Group has not applied these standards in the preparation of

the financial statements:

IAS 1 (Amended) ‘Financial statement presentation’ regarding other

comprehensive income ‘Presentation of financial statements’ is effective

from periods commencing on or after 1 July 2012. The main change

from this amendment is to require entities to group items presented

in ‘other comprehensive income’ (‘OCI’) on the basis of whether they are

potentially reclassifiable to the Group Income Statement subsequently

(reclassification adjustments). The amendments do not address which

items are presented in OCI.

IAS 19 (Amended) ‘Employee benefits’ is effective from periods

commencing on or after 1 January 2013. It eliminates the corridor

approach and requires immediate recognition of all actuarial gains and

losses in the other comprehensive income, immediate recognition of all

past service costs and the replacement of interest cost and expected

return on plan assets with a net interest amount that is calculated by

applying the discount rate to the net defined benefit liability/asset.

IFRS 9 ‘Financial instruments’ is effective from periods commencing

on or after 1 January 2015. It is the first standard issued as part of a

wider project to replace IAS 39. It retains but simplifies the mixed

measurement model and establishes two primary measurement

categories for financial assets: i) amortised cost and ii) fair value.

The basis of classification depends on the entity’s business model

and the contractual cash flow characteristics of the financial asset.

IFRS 10 ‘Consolidated financial statements’ is effective from periods

commencing on or after 1 January 2013. It builds on existing principles

by identifying the concept of control as the determining factor in

whether an entity should be included within the consolidated financial

statements of the parent company. It also provides additional guidance

to assist in the determination of control where this is difficult to assess.

IFRS 11 ‘Joint arrangements’ is effective from periods commencing

onor after 1 January 2013. It is a more realistic reflection of joint

arrangements by focusing on the rights and obligations of the

arrangement rather than its legal form. There are now only two

typesofjoint arrangement: joint operations and joint ventures.

IFRS 12 ‘Disclosures of interests in other entities’ is effective from

periods commencing on or after 1 January 2013. It includes the

disclosure requirements for all forms of interests in other entities,

including joint arrangements, associates, special purpose vehicles

and other off balance sheet vehicles.

IFRS 13 ‘Fair value measurement’ is effective from periods commencing

on or after 1 January 2013. It aims to improve consistency and reduce

complexity by providing precise definition of fair value and single

sourceof fair value measurement and disclosure requirements for

useacross IFRSs.

IAS 27 (Amended) ‘Separate financial statements’ is effective from

periods commencing on or after 1 January 2013. It includes the

provisions on separate financial statements that are left after the

control provisions of IAS 27 have been included in the new IFRS 10.

IAS 28 (Amended) ‘Associates and joint ventures’ is effective from

periods commencing on or after 1 January 2013. It includes the

requirements for joint ventures, as well as associates, to be equity

accounted following the issue of IFRS 11.

IFRS 7 (Amended) ‘Financial instruments: Disclosures’ and IAS 32

(Amended) Financial instruments: Presentation’ are effective from

1 January 2013 and 2014 respectively. The IAS 32 amendment clarifies

some of the requirements for offsetting financial assets and financial

liabilities on the statement of financial position while the IFRS 7

amendment will require more extensive disclosures than are

required under IFRS.

Use of non-GAAP profit measures – underlying profit before tax

The Directors believe that underlying profit before tax and underlying

diluted earnings per share measures provide additional useful information

for shareholders on underlying trends and performance. These measures

are used for performance analysis. Underlying profit is not defined by IFRS

and therefore may not be directly comparable with other companies’

adjusted profit measures. It is not intended to be a substitute for, or

superior to IFRS measurements of profit.

Note 1 Accounting policies continued

100 Tesco PLC Annual Report and Financial Statements 2012