Supercuts 2005 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2005 Supercuts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

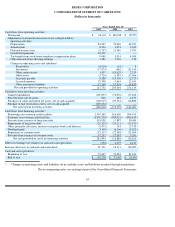

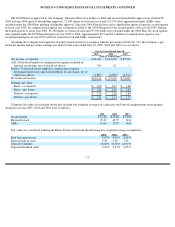

|

|

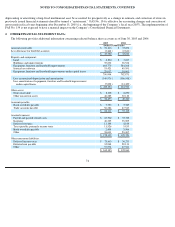

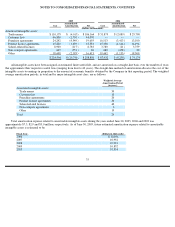

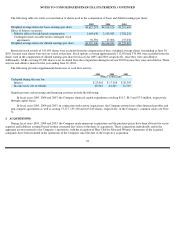

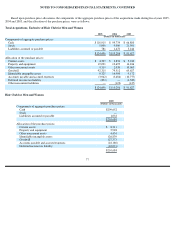

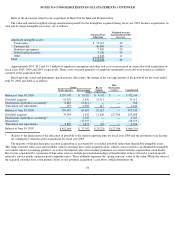

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS, CONTINUED

including how fair value was determined; and (c) the amount of the settlement gain or loss recognized. This EITF must be applied to business

combinations after October 13, 2004. The adoption of EITF 04-1 has not had, and the Company does not expect it to have in the future, a

material impact on its Consolidated Financial Statements.

Also during October 2004, the FASB ratified the consensus reached by the EITF with respect to EITF Issue No. 04-10, “Determining

Whether to Aggregate Operating Segments That Do Not Meet the Quantitative Thresholds” (EITF 04-10), which clarifies the guidance in

paragraph 19 of FAS No. 131, “Disclosures about Segments of an Enterprise and Related Information” (FAS No. 131). According to EITF 04-

10, operating segments that do not meet the quantitative thresholds can be aggregated under paragraph 19 only if aggregation is consistent with

the objective and basic principle of FAS No. 131, the segments have similar economic characteristics, and the segments share a majority of the

aggregation criteria listed in items (a)-(e) in paragraph 17 of FAS No. 131. EITF 04-10 is effective for fiscal years ending after September 15,

2005 (i.e., the Company’s fiscal year 2006), with early application is permitted. The adoption of EITF 04-10 is not expected to have an impact

on the Company’s Consolidated Financial Statements.

On December 21, 2004, the FASB issued FASB Staff Position (FSP) No. FAS 109-2, “Accounting and Disclosure Guidance for the

Foreign Earnings Repatriation Provision within the American Jobs Creation Act of 2004.” FSP No. FAS 109-2 provides accounting and

disclosure guidance for the repatriation provision under the American Jobs Creation Act of 2004, and allows additional time for entities

potentially impacted by the provision to determine whether any foreign earnings will be repatriated under those provisions. As discussed in

Note 8, the Company has completed an evaluation of the repatriation provisions and Treasury guidance and has determined that there is no

advantage to electing repatriation under the Act. As such, the Company does not anticipate repatriating amounts under the provisions of the

Act.

In March 2005, the FASB issued FASB Staff Position (FSP) FIN 46(R)-5, “Implicit Variable Interests Under FIN 46(R).” FSP FIN 46

(R)-5 states that a reporting entity should consider whether it holds an implicit variable interest in a variable interest entity (VIE) or in a

potential VIE. If the aggregate of the explicit and implicit variable interests held by the reporting entity and its related parties would, if held by

a single party, identify that party as the primary beneficiary, the party within the group most closely associated with the VIE should be deemed

the primary beneficiary. The guidance of FSP FIN 46(R)-5 was effective for the reporting period beginning after March 3, 2005 (i.e., the

beginning of the Company’s fiscal fourth quarter). The adoption of FSP FIN 46(R)-5 has not had, and is not expected to have in the future, a

material impact on the Company’s Consolidated Financial Statements.

In March 2005, the FASB also issued FASB Interpretation No. 47, “Accounting for Conditional Asset Retirement Obligations” (FIN 47).

FIN 47 clarifies that an entity must record a liability for a “conditional” asset retirement obligation if the fair value of the obligation can be

reasonably estimated. FIN 47 is effective for no later than the end of fiscal years ending after December 15, 2005 (i.e., the end of the

Company’s fiscal year 2006). The Company adopted FIN 47 during the fourth quarter of fiscal year 2005 and it did not have a material effect

on the Consolidated Financial Statements.

In June 2005, the FASB issued FAS No. 154, “Accounting Changes and Error Corrections.”

FAS No. 154 replaces Accounting Principles

Board Opinion No. 20, “Accounting Changes” and FAS No. 3, “Reporting Accounting Changes in Interim Financial Statements.” FAS

No. 154 requires that a voluntary change in accounting principle be applied retrospectively with all prior period financial statements presented

on the new accounting principle. FAS No. 154 also requires that a change in method of

73