Supercuts 2005 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2005 Supercuts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

|

|

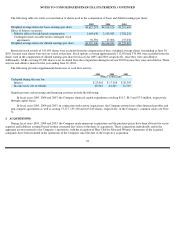

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS, CONTINUED

Derivative Instruments:

The Company may manage its exposure to interest rate and foreign currency risk within the Consolidated Financial Statements through

the use of derivative financial instruments, according to its hedging policy. The Company does not use derivatives with a level of complexity or

with a risk higher than the exposures to be hedged and does not hold or issue derivatives for trading or speculative purposes. The Company

currently has or had interest rate swaps designated as both cash flow and fair value hedges, treasury locks designated as cash flow hedges and a

hedge of its net investment in its European operations. Refer to Note 5 to the Consolidated Financial Statements for further discussion.

The Company follows Statement of Financial Accounting Standards (FAS) No. 133, “

Accounting for Derivative Instruments and Hedging

Activities,” as amended and interpreted, which requires that all derivatives be recorded on the balance sheet at fair value. FAS No.133 also

requires companies to designate all derivatives that qualify as hedging instruments as fair value hedges, cash flow hedges or hedges of net

investments in foreign operations. This designation is based upon the exposure being hedged. Cash flow and fair value hedges are designated

and documented at the inception of each hedge by matching the terms of the contract to the underlying transaction. At inception, as dictated by

the facts and circumstances, all hedges are expected to be highly effective, as the critical terms of these instruments are generally the same as

those of the underlying risks being hedged. All derivatives designated as hedging instruments are assessed for effectiveness on an on-going

basis. The Company classifies the cash flows from hedging transactions in the same categories as the cash flows from the respective hedged

items.

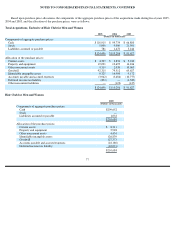

Stock-Based Employee Compensation Plans:

At June 30, 2005, the Company had the 2004 Long Term Incentive Plan (2004 Plan) and the 2000 Stock Option Plan. Additionally, the

Company has outstanding stock options under its 1991 Stock Option Plan, although the Plan terminated in 2001. Prior to July 1, 2003, the

Company accounted for its 2000 Stock Option Plan and 1991 Stock Option Plan using the intrinsic value method under the recognition and

measurement principles of Accounting Principles Board (APB) Opinion No. 25, “Accounting for Stock Issued to Employees” (APB No. 25)

and related Interpretations and applied FAS No. 123, “Accounting for Stock-Based Compensation” (FAS No. 123), as amended by FAS

No. 148,

“Accounting for Stock-Based Compensation—Transition and Disclosure” (FAS No. 148), for disclosure purposes only. The FAS

No. 123 disclosures include pro forma net income and earnings per share as if the fair value

-based method of accounting had been used. Under

the provisions of APB No. 25, no stock-based employee compensation cost is reflected in net income, as all options granted under those plans

had an exercise price equal to the market value of the underlying stock on the date of grant.

Effective July 1, 2003, the Company adopted the fair value recognition provisions of FAS No. 123 using the prospective transition

method. Under the prospective method of adoption, compensation cost is recognized related to options granted, modified or settled after the

beginning of the fiscal year in which the fair value method is first adopted. Under this approach, fiscal year 2005 and 2004 compensation

expense is less than it would have been had the fair value recognition provisions of FAS No. 123 been applied from its original effective date

because the fair value of the options vesting during the year which were granted prior to fiscal year 2004 are not recognized under the

prospective transition method in the Consolidated Statement of Operations. Options granted in fiscal years prior to the adoption of the fair

value recognition provisions continue to be accounted for under APB Opinion No. 25. The adoption of the fair value recognition provisions for

stock options increased the Company’s fiscal year 2005 compensation expense by $0.4 million (related to recognizing compensation expense

as options vest if they were granted after July 1, 2003).

70