Supercuts 2005 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2005 Supercuts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

|

|

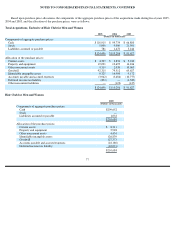

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS, CONTINUED

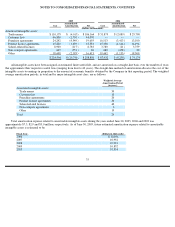

During fiscal years 2005, 2004 and 2003, the Company tested its long-lived assets for impairment and recognized impairment charges

related to the carrying value of certain salons’ property and equipment located primarily in North America of $3.6, $3.2 and $3.1 million,

respectively. None of the impaired salon assets were held for sale. Impairment charges are included in depreciation related to company-owned

salons in the Consolidated Statement of Operations.

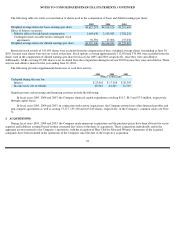

Deferred Rent and Rent Expense:

The Company leases most locations under operating leases. Most lease agreements contain tenant improvement allowances funded by

landlord incentives, rent holidays, rent escalation clauses and/or contingent rent provisions. Accounting principles generally accepted in the

United States of America require rent expense to be recognized on a straight-

line basis over the lease term. The difference between the rent due

under the stated terms of the lease compared to that of the straight-line basis is recorded as deferred rent within other noncurrent liabilities in

the Consolidated Balance Sheet.

For purposes of recognizing incentives and minimum rental expenses on a straight-line basis over the terms of the leases, the Company

uses the date that it obtains the legal right to use and control the leased space to begin amortization, which is generally when the Company

enters the space and begins to make improvements in preparation of intended use of the leased space.

For tenant improvement allowances funded by landlord incentives and rent holidays, the Company records a deferred rent liability in other

noncurrent liabilities on the Consolidated Balance Sheet and amortizes the deferred rent over the term of the lease as reductions to rent expense

on the Consolidated Statements of Operations.

Certain lease agreements contain rent escalation clauses which provide for scheduled rent increases during the lease terms or for rental

payments commencing at a date other than the date of initial occupancy. Such “stepped” rent expense is recorded in the Consolidated

Statements of Operations on a straight-line basis over the lease term.

Certain leases provide for contingent rents that are determined as a percentage of revenues in excess of specified levels. The Company

records a contingent rent liability in accrued expenses on the Consolidated Balance Sheet, along with the corresponding rent expense in the

Consolidated Statement of Operations, when specified levels have been achieved or when management determines that achieving the specified

levels during the fiscal year is probable.

Company-Owned Revenue Recognition and Deferred Revenue:

Company-owned salon revenues and related cost of sales are recognized at the time of sale, as this is when the services have been

provided or, in the case of product revenues, delivery has occurred, and the salon receives the customer’s payment. Revenues from purchases

made with gift cards are also recorded when the customer takes possession of the merchandise. Gift cards issued by the Company are recorded

as a liability (deferred revenue) until they are redeemed. An accrual for estimated returns and credits has been recorded based on historical

customer return data that management believes to be reasonable, and is less than one percent of sales.

Product sales by the Company to its franchisees are included within product revenues on the Consolidated Statement of Operations and

recorded at the time product is shipped to franchise locations. The related cost of product sold to franchisees is included within cost of product

in the Consolidated Statement of Operations.

67