Seagate 2003 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2003 Seagate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

|

|

Table of Contents

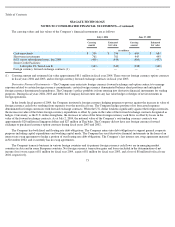

SEAGATE TECHNOLOGY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

1. Summary of Significant Accounting Policies

Nature of Operations —In August 2000, Seagate Technology, which was then known as Seagate Technology Holdings and is referred to

herein as “the Company,” was formed to be a holding company for the rigid disc drive operating business and the storage area networks

operating business of Seagate Technology, Inc., a Delaware corporation, which is referred to herein as “Seagate Delaware.”

In November 2002,

the Company sold XIOtech Corporation, its wholly-owned indirect subsidiary that operated the Company’s storage area networks operating

business, to New SAC. See Note 10, Sale of XIOtech Corporation.

In December 2002, the Company completed the initial public offering of 72,500,000 of its common shares, 24,000,000 of which were

sold by the Company and 48,500,000 of which were sold by New SAC, as selling shareholder, at a price of $12 per share. Immediately prior to

the closing of the initial public offering, the Company’s then-

outstanding 400 million preferred shares owned by New SAC were converted into

common shares on a one-to-one basis. The Company’s common shares began trading on December 11, 2002. In July 2003, the Company

completed the secondary offering of 69,000,000 of its common shares, all of which were sold by New SAC, as selling shareholder, at a price of

$18.75 per share. As of July 2, 2004, New SAC owned 282,500,000 common shares of the Company, or approximately 61.5% of total

outstanding common shares.

The Company designs, manufactures and markets products for storage, retrieval and management of data on computer and data

communications systems. The Company sells its products to original equipment manufacturers (“OEM”) for inclusion in their computer

systems or subsystems, and to distributors who typically sell to small OEMs, dealers, system integrators and other resellers.

Critical Accounting Policies and Use of Estimates —The preparation of financial statements in conformity with accounting principles

generally accepted in the United States requires management to make estimates and assumptions that affect the amounts reported in the

financial statements and accompanying notes. Actual results could differ materially from those estimates.

The Company establishes certain distributor and OEM sales programs aimed at increasing customer demand. These programs are

typically related to a distributor’s level of sales, order size, advertising or point of sale activity or an OEM’s level of sale activity or agreed

upon rebate programs. The Company provides for these obligations at the time that revenue is recorded based on estimated requirements. These

estimates are based on various factors, including estimated future price erosion, distributor sell-through levels, program participation, customer

claim submittals and sales returns. Significant actual variations in any of these factors could have a material effect on the Company’s operating

results. In addition, our failure to accurately predict the level of future sales returns by our distribution customers could have a material impact

on our financial condition and results of operations.

The Company’s warranty provision considers estimated product failure rates, trends and estimated repair or replacement costs. The

Company uses a statistical model to help with its estimates and the Company exercises considerable judgment in determining the underlying

estimates. Should actual experience in any future period differ significantly from its estimates, or should the rate of future product

technological advancements fail to keep pace with the past, the Company’s future results of operations could be materially affected. The actual

results with regard to warranty expenditures could have a material adverse effect on the Company if the actual rate of unit failure or the cost to

repair a unit is greater than that which the Company has used in estimating the warranty expense accrual.

The Company’s recording of deferred tax assets each period depends primarily on the Company’s ability to generate current and future

taxable income in the United States. Each period the Company evaluates the need for a valuation allowance for the deferred tax assets and

adjusts the valuation allowance so that net deferred tax

66