Salesforce.com 2012 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2012 Salesforce.com annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

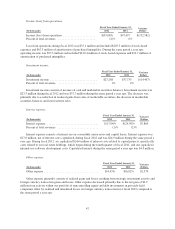

Foreign currency exchange risk

Our results of operations and cash flows are subject to fluctuations due to changes in foreign currency

exchange rates, particularly changes in the Euro, British Pound Sterling and Japanese Yen. We seek to minimize

the impact of certain foreign currency fluctuations by hedging certain balance sheet exposures with foreign

currency forward contracts. Any gain or loss from settling these contracts is offset by the loss or gain derived

from the underlying balance sheet exposures. In accordance with our policy, the hedging contracts we enter into

have maturities of less than three months. Additionally, by policy, we do not enter into any hedging contracts for

trading or speculative purposes.

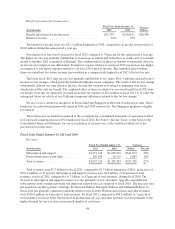

Interest rate sensitivity

We had cash, cash equivalents and marketable securities totaling $1.4 billion at January 31, 2012. This

amount was invested primarily in money market funds, time deposits, corporate notes and bonds, government

securities and other debt securities with credit ratings of at least single A or better. The cash, cash equivalents

and short-term marketable securities are held for working capital purposes. Our investments are made for capital

preservation purposes. We do not enter into investments for trading or speculative purposes.

Our cash equivalents and our portfolio of marketable securities are subject to market risk due to changes in

interest rates. Fixed rate securities may have their market value adversely impacted due to a rise in interest rates,

while floating rate securities may produce less income than expected if interest rates fall. Due in part to these

factors, our future investment income may fall short of expectation due to changes in interest rates or we may

suffer losses in principal if we are forced to sell securities that decline in market value due to changes in interest

rates. However because we classify our debt securities as “available for sale,” no gains or losses are recognized

due to changes in interest rates unless such securities are sold prior to maturity or declines in fair value are

determined to be other-than-temporary. Our fixed-income portfolio is subject to interest rate risk.

An immediate increase or decrease in interest rates of 100-basis points at January 31, 2012 could result in a

$12.1 million market value reduction or increase of the same amount. This estimate is based on a sensitivity

model that measures market value changes when changes in interest rates occur. Fluctuations in the value of our

investment securities caused by a change in interest rates (gains or losses on the carrying value) are recorded in

other comprehensive income, and are realized only if we sell the underlying securities.

At January 31, 2011, we had cash, cash equivalents and marketable securities totaling $1.4 billion. The

fixed-income portfolio was also subject to interest rate risk. Changes in interest rates of 100-basis points would

have resulted in market value changes of $27.7 million.

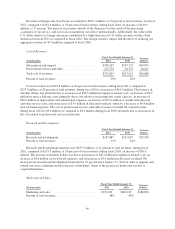

Market Risk and Market Interest Risk

In January 2010, we issued at par value $575.0 million of 0.75% convertible senior notes due 2015 (the

“Notes”). Holders may convert their Notes prior to maturity upon the occurrence of certain circumstances. Upon

conversion, we would pay the holder an amount of cash equal to the principal amount of the Notes. Amounts in

excess of the principal amount, if any, may be paid in cash or stock at our option. Concurrent with the issuance of

the Notes, we entered into separate note hedging transactions and the sale of warrants. These separate

transactions were completed to reduce the potential economic dilution from the conversion of the Notes.

For the three months ended January 31, 2012 the Notes were convertible at the option of the noteholder. For

20 trading days during the 30 consecutive trading days ended January 31, 2012, our common stock traded did not

exceed 130% of the conversion price of $85.36 per share applicable to the Notes. Accordingly, the Notes will not

be convertible at the holders’ option for the quarter ending April 30, 2012 and will be reclassified as a noncurrent

liability on our consolidated balance sheet so long as the Notes are not convertible.

57