Rite Aid 2012 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2012 Rite Aid annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

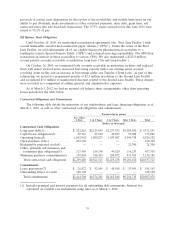

The table below provides information about our financial instruments that are sensitive to changes

in interest rates. The table presents principal payments and the related weighted average interest rates

by expected maturity dates for each fiscal year as of March 3, 2012.

Fair Value at

March 3,

2013 2014 2015 2016 2017 Thereafter Total 2012

(Dollars in thousands)

Long-term debt, including current

portion, excluding capital lease

obligations

Fixed Rate ................. $59,445 $186,345 $ — $469,187 $880,000 $3,134,000 $4,728,977 $4,934,587

Average Interest Rate ........... 8.00% 6.95% 0.00% 9.26% 10.08% 8.62% 8.88%

Variable Rate ............... $ — $ 2,971 $1,044,692 $139,430 $ — $ 326,708 $1,513,801 $1,469,813

Average Interest Rate ........... 0.00% 2.01% 2.01% 5.48% 0.00% 4.50% 2.87%

Our ability to satisfy interest payment obligations on our outstanding debt will depend largely on

our future performance, which, in turn, is subject to prevailing economic conditions and to financial,

business and other factors beyond our control. If we do not have sufficient cash flow to service our

interest payment obligations on our outstanding indebtedness and if we cannot borrow or obtain equity

financing to satisfy those obligations, our business and results of operations could be materially

adversely affected. We cannot be assured that any replacement borrowing or equity financing could be

successfully completed.

The interest rate on our variable rate borrowings, which include our revolving credit facility and

our Tranche 2 Term loans and Tranche 5 Term loans, are all based on LIBOR. However, the interest

rate on our Tranche 5 Term loans has a LIBOR floor of 125 basis points. If the market rates of interest

for LIBOR changed by 100 basis points as of March 3, 2012, our annual interest expense would change

by approximately $10.4 million.

A change in interest rates does not have an impact upon our future earnings and cash flow for

fixed-rate debt instruments. As fixed-rate debt matures, however, and if additional debt is acquired to

fund the debt repayment, future earnings and cash flow may be affected by changes in interest rates.

This effect would be realized in the periods subsequent to the periods when the debt matures.

Increases in interest rates would also impact our ability to refinance existing maturities on favorable

terms.

Item 8. Financial Statements and Supplementary Data

Our consolidated financial statements and notes thereto are included elsewhere in this report and

are incorporated by reference herein. See Item 15 of Part IV.

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

Not applicable

Item 9A. Controls and Procedures

(a) Disclosure Controls and Procedures

Our management, with the participation of our Chief Executive Officer and Chief Financial

Officer, has evaluated the effectiveness of disclosure controls and procedures (as such term is defined

in Rules 13a-15(e) and 15d-15(e) under the Securities Exchange Act of 1934, as amended (the

‘‘Exchange Act’’)) as of the end of the period covered by this report. Based on such evaluation, our

Chief Executive Officer and Chief Financial Officer have concluded that, as of the end of such period,

our disclosure controls and procedures are effective.

46