Kodak 2004 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2004 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

|

|

Financials

69

2 0 0 4 S U M M A R Y A N N U A L R E P O R T

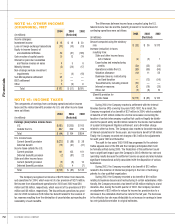

Qualex,awhollyownedsubsidiaryofKodak,hasa50%ownership

interestinExpressStopFinancing(ESF),whichisajointventurepartner-

shipbetweenQualexandasubsidiaryofDanaCreditCorporation(DCC),

awhollyownedsubsidiaryofDanaCorporation.Qualexaccountsforits

investmentinESFundertheequitymethodofaccounting.ESFprovideda

long-termfinancingsolutiontoQualex’sphotofinishingcustomersincon-

nectionwithQualex’sleasingofphotofinishingequipmenttothirdparties,

asopposedtoQualexextendinglong-termcredit.Aspartoftheoperations

ofitsphotofinishingservices,Qualexsoldequipmentunderasales-type

leasearrangementandrecordedalong-termreceivable.Theselong-term

receivablesweresubsequentlysoldtoESFwithoutrecoursetoQualexand,

therefore,thesereceivableswereremovedfromQualex’saccounts.ESF

incurreddebttofinancethepurchaseofthereceivablesfromQualex.This

debtwascollateralizedsolelybythelong-termreceivablespurchasedfrom

Qualex,andinpart,bya$40millionguaranteefromDCC.Thisguarantee

wasterminatedonDecember17,2004inconjunctionwiththepaymentin

fullofthisdebtonthesamedate(seebelow).Qualexprovidednoguaran-

teeorcollateraltoESF’screditorsinconnectionwiththedebt,andESF’s

debtwasnon-recoursetoQualex.Qualex’sonlycontinuedinvolvementin

connectionwiththesaleofthelong-termreceivablesistheservicingofthe

relatedequipmentundertheleases.Qualexhascontinuedrevenuestreams

inconnectionwiththisequipmentthroughfuturesalesofphotofinishing

consumables,includingpaperandchemicals,andmaintenance.

Althoughthelessees’requirementtopayESFundertheleaseagree-

mentsisnotcontingentuponQualex’sfulfillmentofitsservicingobliga-

tions,undertheagreementwithESF,Qualexwouldberesponsibleforany

deficiencyintheamountofrentnotpaidtoESFasaresultofanylessee’s

claimregardingmaintenanceorsupplyservicesnotprovidedbyQualex.

Suchleasepaymentswouldbemadeinaccordancewiththeoriginallease

terms,whichgenerallyextendover5to7years.Todate,theCompany

hasincurrednosuchmaterialclaims,andQualexdoesnotanticipateany

significantsituationswhereitwouldbeunabletofulfillitsserviceobliga-

tionsunderthearrangementwithESF.ESF’soutstandingleasereceivable

amountwasapproximately$113millionatDecember31,2004.

EffectiveJuly20,2004,ESFenteredintoanagreementamendingthe

ReceivablesPurchaseAgreement(RPA),whichrepresentsthefinancing

arrangementbetweenESFanditsbanks.UndertheamendedRPAagree-

ment,maximumborrowingswereloweredto$200million.OnDecember

17,2004,ESFterminatedtheRPAuponpaymentinfull,toitsbanks,of

thethenoutstandingbalanceoftheRPAtotaling$138million.Pursuant

totheESFpartnershipagreementbetweenQualexandDCC,commenc-

ingOctober6,2003,QualexnolongersellsitsleasereceivablestoESF.

QualexcurrentlyisutilizingtheservicesofImagingFinancialServices,

Inc.,awhollyownedsubsidiaryofGeneralElectricCapitalCorporation,as

itsprimaryfinancingsolutionforprospectiveleasingactivitywithitsU.S.

customers.

TheCompanyperformedananalysisofESFinordertodetermine

whethertheprovisionsofFASBInterpretationNo.46(R)“Consolidationof

VariableInterestEntitiesaninterpretationofARBNo.51”(FIN46(R))were

applicabletoESF,requiringconsolidation.Basedontheanalysisperformed,

itwasdeterminedthatESFdoesnotqualifyasavariableinterestentity

underFIN46(R)and,therefore,consolidationisnotrequired.

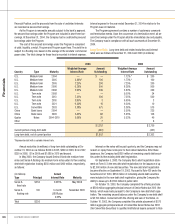

AtDecember31,2004,theCompanyhadoutstandinglettersof

credittotaling$110millionandsuretybondsintheamountof$117million

primarilytoensurethecompletionofenvironmentalremediationsandpay-

mentofpossiblecasualtyandworkers’compensationclaims.InFebruary

of2005,theCompanyissued$31millioninlettersofcreditinsupportof

Workers’Compensationliabilities.

Rentalexpense,netofminorsubleaseincome,amountedto$161

millionin2004,and$157millionineachoftheyears2003and2002.The

approximateamountsofnoncancelableleasecommitmentswithtermsof

morethanoneyear,principallyfortherentalofrealproperty,reducedby

minorsubleaseincome,are$128millionin2005,$97millionin2006,$79

millionin2007,$61millionin2008,$46millionin2009and$104million

in2010andthereafter.

InDecember2003,theCompanysoldapropertyinFranceforap-

proximately$65million,netofdirectsellingcosts,andthenleasedbacka

portionofthispropertyforanine-yearterm.InaccordancewithSFASNo.

98,“AccountingforLeases,”theentiregainonthepropertysaleofapprox-

imately$57millionwasdeferredandnogainwasrecognizableuponthe

closingofthesaleastheCompany’scontinuinginvolvementintheproperty

isdeemedtobesignificant.Asaresult,theCompanyisaccountingforthe

transactionasafinancing.Futureminimumleasepaymentsunderthisnon-

cancelableleasecommitmentamountsnotedaboveincludeapproximately

$5millionperyearfor2005through2009,andapproximately$15million

for2010andthereafter,inrelationtothistransaction.

OnMarch8,2004,theCompanyfiledacomplaintagainstSony

CorporationinfederaldistrictcourtinRochester,NewYork,fordigital

camerapatentinfringement.Severalweekslater,onMarch31,2004,

SonysuedtheCompanyfordigitalcamerapatentinfringementinfederal

districtcourtinNewark,NewJersey.Sonysubsequentlyfiledasecond

lawsuitagainsttheCompanyinNewark,NewJersey,alleginginfringement

ofavarietyofotherSonypatents.TheCompanyfiledacounterclaimin

theNewJerseyaction,assertinginfringementbySonyoftheCompany’s

kioskpatents.TheCompanysuccessfullymovedtotransferSony’sNew

JerseydigitalcamerapatentinfringementcasetoRochester,NewYork,

andthetwodigitalcamerapatentinfringementcasesarenowconsolidated

forpurposesofdiscovery.Basedonthecurrentdiscoveryschedule,the

Companyexpectsthatclaimsconstructionhearingsinthedigitalcamera

caseswilltakeplacein2006.BoththeCompanyandSonyCorporation

seekunspecifieddamagesandotherrelief.Althoughthislawsuitmayresult

intheCompany’srecoveryofdamages,theamountofthedamages,if

any,cannotbequantifiedatthistime.Accordingly,theCompanyhasnot

recognizedanygaininthefinancialstatementsasofDecember31,2004,

inconnectionwiththismatter.

OnOctober7,2004,theCompanyandSunMicrosystemsInc.reached

atentativeagreementtosettlealawsuitfiledbyKodakonFebruary11,

2002inFederalDistrictCourt,WesternDistrictofNewYork,forinfringe-

mentofthreeKodakpatentscoveringasoftwarearchitectureusedinSun’s

Javaproduct.ThesettlementfollowedanOctober1,2004verdictinwhich

afederalcourtjuryfoundthattheKodakpatentsinissuewerevalid,that

Suninfringedthepatents,andthatSun’saffirmativedefensewaswithout

merit.

OnOctober12,2004,afinalsettlementagreementwassigned.

Pursuanttothetermsofthesettlementagreement,SunpaidKodak$92

millionincashonOctober12,2004.

KodakprovidedtoSunanon-exclusivelicenseundertheKodak

patentsatissue.Inaddition,KodaklicensedtoSuncertainotherKodak