Kodak 2004 Annual Report Download - page 123

Download and view the complete annual report

Please find page 123 of the 2004 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

|

|

Proposals

14

2 0 0 5 N O T I C E O F A N N U A L M E E T I N G A N D P R O X Y S T A T E M E N T

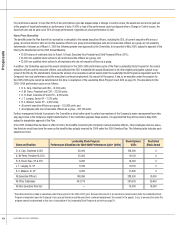

FederalTaxTreatment

ThefollowingisasummaryoftheU.S.federalincometaxconsequencesofparticipatinginthePlan.Thisdiscussiondoesnotaddressallaspectsofthe

U.S.federalincometaxconsequences,includinganystate,localorforeigntaxconsequencesofparticipatinginthePlan.Thissectionisbasedonthe

InternalRevenueCode,itslegislativehistory,existingandproposedregulationsundertheInternalRevenueCodeandpublishedrulingsandcourtdecisions,

allascurrentlyineffect.Theselawsaresubjecttochange,possiblyonaretroactivebasis.

IncentiveStockOptions.Aparticipantwillnotbesubjecttotaxuponthegrantofanincentivestockoption(ISO)orupontheexerciseofanISO.However,

theexcessofthefairmarketvalueofthesharesonthedateofexerciseovertheexercisepricepaidwillbeincludedinaparticipant’salternativeminimum

taxableincome.Whetheraparticipantissubjecttothealternativeminimumtaxwilldependontheparticipant’sparticularcircumstances.Theparticipant’s

basisinthesharesreceivedwillbeequaltotheexercisepricepaid,andtheparticipant’sholdingperiodinsuchshareswillbeginonthedayfollowingthe

dateofexercise.

Ifaparticipantdisposesofthesharesonorafterthelaterof:1)thesecondanniversaryofthedateofgrantoftheISOand2)thefirstanniversaryofthe

dateofexerciseoftheISO(thestatutoryholdingperiod),aparticipantwillrecognizeacapitalgainorlossinanamountequaltothedifferencebetween

theamountrealizedonsuchdispositionandaparticipant’sbasisintheshares.

Iftheparticipantdisposesofthesharesbeforetheendofthestatutoryholdingperiod,theparticipantwillhaveengagedina“disqualifyingdisposition.”As

aresult,theparticipantwillbesubjecttotax:1)ontheexcessofthefairmarketvalueofthesharesonthedateofexercise(ortheamountrealizedonthe

disqualifyingdisposition,ifless)overtheexercisepricepaid,asordinaryincomeand2)ontheexcess,ifany,oftheamountrealizedonsuchdisqualify-

ingdispositionoverthefairmarketvalueofthesharesonthedateofexercise,ascapitalgain.Iftheamountaparticipantrealizesfromadisqualifying

dispositionislessthantheexercisepricepaid(i.e.,theparticipant’sbasis)andthelosssustaineduponsuchdispositionwouldotherwiseberecognized,a

participantwillnotrecognizeanyordinaryincomefromsuchdisqualifyingdispositionandinsteadtheparticipantwillrecognizeacapitalloss.Intheevent

ofadisqualifyingdisposition,theCompanyoroneofitssubsidiariescangenerallydeducttheamountrecognizedasordinaryincomebytheparticipant.

ThecurrentpositionoftheInternalRevenueServiceisthatincometaxwithholdingandFICAandFUTAtaxes(employmenttaxes)donotapplyuponthe

exerciseofanISOoruponanysubsequentdisposition,includingadisqualifyingdisposition,ofsharesacquiredpursuanttotheexerciseoftheISO.

NonstatutoryStockOptions.Theparticipantwillnotbesubjecttotaxuponthegrantofanoptionwhichisnotintendedtobe(ordoesnotqualifyas)

anISO(anonstatutorystockoption).Uponexerciseofanonstatutorystockoption,anamountequaltotheexcessofthefairmarketvalueoftheshares

acquiredonthedateofexerciseovertheexercisepricepaidistaxabletotheparticipantasordinaryincome,andsuchamountisgenerallydeductibleby

theCompanyoroneofitssubsidiaries.Thisamountofincomewillbesubjecttoincometaxwithholdingandemploymenttaxes.Theparticipant’sbasisin

thesharesreceivedwillequalthefairmarketvalueofthesharesonthedateofexercise,andtheparticipant’sholdingperiodinsuchshareswillbegin.

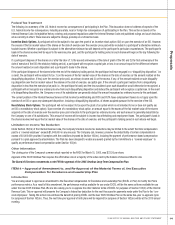

LimitationonIncomeTaxDeduction

UnderSection162(m)oftheInternalRevenueCode,theCompany’sfederalincometaxdeductionsmaybelimitedtotheextentthattotalcompensation

paidtoa“coveredemployee”exceeds$1,000,000inanyoneyear.TheCompanycan,however,preservethedeductibilityofcertaincompensationin

excessof$1,000,000provideditcomplieswiththeconditionsimposedbySection162(m),includingthepaymentofperformance-basedcompensation

pursuanttoaplanapprovedbyshareholders.ThePlanhasbeendesignedtoenableanyawardgrantedbytheCommitteetoa“coveredemployee”to

qualifyasperformance-basedcompensationunderSection162(m).

OtherInformation

TheclosingpriceoftheCompany’scommonstockreportedontheNYSEforMarch15,2005,was$33.50pershare.

Approvalofthe2005OmnibusPlanrequirestheaffirmativevoteofamajorityofthevotescastbytheholdersofsharesentitledtovote.

TheBoardofDirectorsrecommendsavoteFORtheapprovalofthe2005OmnibusLong-TermCompensationPlan.

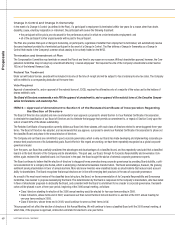

ITEM4 — ApprovalofAmendmentto,andRe-ApprovaloftheMaterialTermsof,theExecutive

CompensationforExcellenceandLeadershipPlan

Introduction

YouarebeingaskedtoapproveanamendmenttotheExecutiveCompensationforExcellenceandLeadershipPlan(EXCELorPlan)tomodifythePlan’s

performancemetrics.Asaresultofthisamendment,theperformancemetricsavailableforuseunderEXCELwillbethesameasthoseavailableforuse

underthenew2005OmnibusPlan.Wearealsoaskingyoutore-approvetheothermaterialtermsofEXCELforpurposesofSection162(m)oftheInternal

RevenueCode.Thisre-approvalwillpreservetheCompany’sfederaltaxdeductionforthenextfiveyearsforpaymentsmadeunderthePlantothe“cov-

eredemployees.”TakingthisactionnowwillhavethebenefitofplacingEXCELandthenew2005OmnibusPlanonthesamefive-yearre-approvalcycle

forpurposesofSection162(m).Thus,thenexttimeyourapprovalofbothplanswillberequiredforpurposesofSection162(m)willbeatthe2010annual

meeting.