Food Lion 2004 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2004 Food Lion annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

DELHAIZE GROUP ANNUAL REPORT 2004 43

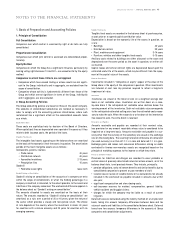

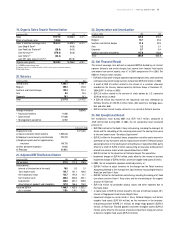

1. Basis of Preparation and Accounting Policies

1. Principle of Consolidation

Full Consolidation

Companies over which control is exercised by right or de facto are fully

consolidated.

Proportionate Consolidation

Companies over which joint control is exercised are consolidated propor-

tionately.

Equity M ethod

Companies on which the Group has a significant influence, particularly by

owning voting rights betw een 10 and 50%, are accounted for by the equity

method.

Companies to which these Criteria are not Applied:

• Companies w hich have ceased trading or whose results are not signifi-

cant to the Group, individually and in aggregate, are excluded from the

scope of consolidation.

• Companies w hose activity is fundamentally different from those of the

Group and w hich are not significant in terms of the Group, individually

and in aggregate, are also excluded.

2. Group Accounting Policies

The Group accounting policies are based on those of the parent company.

The accounts of consolidated subsidiaries are restated as necessary in

order to comply w ith the accounting policies stated below, w here such

restatement has a significant effect on the consolidated accounts taken

as a w hole.

Establishment Costs

These costs are capitalized only by decision of the Board of Directors.

When capitalized, they are depreciated over a period of five years or, if they

relate to debt issuance costs, the period of the loans.

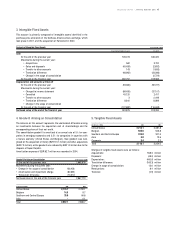

Intangible Fixed Assets

The intangible fixed assets appearing on the balance sheet are amortized

on the basis of the economic life of the assets in question. The amortization

periods of the main intangible assets are as follow s :

Concessions, patents, licences

• Trade names 40 years

• Distribution network 40 years

• Assembled workforce 2-13 years

• Prescription files 15 years

Goodwill

• Favorable lease rights lease term

Goodwill Arising on Consolidation

Goodwill arising on consolidation of the accounts of a company on entry

within the scope of consolidation, or when the holding percentage in a

company is modified, is allocated, to the extent possible, to the assets and

liabilities of the company concerned. The unallocated difference appears in

the balance sheet as “ Goodw ill arising on consolidation” .

The amounts allocated to assets are amortized on the basis of their

nature. The amounts recorded as “ Goodwill arising on consolidation” are

amortized, as a rule, over a period of 20 or 40 years, given the nature of

the sector which provides a steady and non-cyclical return. The choice

of rate depends on the country where the investment is made: 40 years

for countries w ith a mature economy and 20 years for countries with an

emerging economy.

Tangible Fixed Assets

Tangible fixed assets are recorded in the balance sheet at purchase price,

at cost price or at agreed capital contribution value.

Depreciation is based on the economic life of the assets in question, as

a rule :

• Buildings 40 years

• Distribution centers 33 years

• Plant, machinery and equipment 3-14 years

• Furniture, vehicles and other tangible fixed assets 5-10 years

Ancillary costs related to buildings are either allocated to the asset and

depreciated over the same period as the asset in question, or w ritten off

as incurred.

Capital leases and similar contract rights are depreciated based upon the

estimated useful life of the assets, which may be different from the repay-

ment of the capital value of the assets.

Financial Fixed Assets

Investments included in “ Companies at equity” appear at the value of the

Group share in the equity of the companies in question. Other investments

are included at cost, less any provision required to reflect a long-term

impairment of value.

Inventories

Inventories are valued at the lower of cost on a w eighted average cost

basis or net realizable value. Inventories are written down on a case-

by-case basis if the anticipated net realizable value declines below the

carrying amount of the inventories. Such net realizable value corresponds

to the anticipated estimated selling price less the estimated costs neces-

sary to make the sale. When the reason for a write-dow n of the inventories

has ceased to exist, the w rite-down is reversed.

Receivables and Payables

Amounts receivable and payable are recorded at their nominal value,

less provision for any amount receivable w hose value is considered to be

impaired on a long-term basis. Amounts receivable and payable in a cur-

rency other than the currency of the subsidiary are valued at the exchange

rate on the closing date. The resulting translation difference on conversion

(for each currency) is written off if it is a loss and deferred if it is a gain.

Exchange gains and losses and conversion differences arising on debts

contracted to finance non-monetary assets are recognized based on the

principle of matching expenses to the income to which they relate.

Provisions and Deferred Taxes

Provisions for liabilities and charges are recorded to cover probable or

certain losses of precisely determined nature but whose amount, as at the

balance sheet date, is not precisely know n. They include, principally:

• pension obligations, early retirement benefits and similar benefits due by

consolidated companies to present or past members of staff;

• taxation due on review of taxable income or tax calculations not already

included in the estimated tax payable included in amounts due w ithin

one year;

• significant reorganization and store closing costs;

• self-insurance reserves for w orkers’ compensation, general liability,

vehicle accident and druggist claims;

• charges for which the company may be liable as a result of current

litigation.

Deferred taxes are calculated using the liability method on a full provision

basis, taking into account temporary differences betw een book and tax

values of assets and liabilities in the consolidated balance sheet. Deferred

taxes have two sources: temporary differences in the accounts of Group

companies and consolidation adjustments.

NOTES TO THE FINANCIAL STATEMENTS