Food Lion 2004 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2004 Food Lion annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

DELHAIZE GROUP ANNUAL REPORT 2004

34

In addition to a defi ned contribution plan provided to substantially all associ-

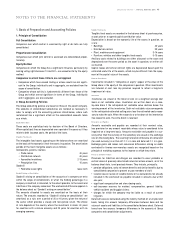

ates, Hannaford has a defi ned benefi t pension plan (cash balance plan) cover-

ing approximately 50% of its associates. The plan provides for payment of

retirement benefi ts on the basis of the associate’s length of service and sal-

ary. The plan is managed by several fund management companies for equities

(approximately 69% of assets), fi xed income (approximately 29% of assets)

and cash equivalents (2% of assets).

Under Belgian GAAP, the Hannaford pension plan is accounted for using US

GAAP rules as described hereunder, however the amount recorded under

US GAAP in “ Other comprehensive income” is reclassifi ed to the caption

“ Prepayments and accrued income” . Under US GAAP, Hannaford evaluates

annually the status of the pension fund in September. On September 30, 2004,

the fund assets had a value of EUR 60.9 million (USD 83.0 million), result-

ing in an underfunding of EUR 18.4 million (USD 25.0 million). The assump-

tions used in calculating the value of the assets w ere a discount rate of 5.8%

and an expected rate of return on investments of 7.75%. In 2004, the cost of

Hannaford’s defi ned benefi t program w as EUR 7.0 million (USD 8.7 million).

The funding contribution was EUR 6.5 million (USD 8.1 million) while a mini-

mum pension liability of EUR 20.1 million (USD 27.4 million) was recognized

on the balance sheet, a reduction from the previously recorded amount by

EUR 1.8 million (USD 2.2 million), net of taxes recorded as an adjustment to

“ Other comprehensive income” , a component of equity, without affecting net

earnings.

In addition to the pension plans described above, Delhaize Group has a post-

employment benefi t obligation at its Greek company Alfa-Beta. This obliga-

tion relates to termination indemnities prescribed by Greek law, consisting

of lump-sum compensations, granted only in cases of normal retirement or

termination of employment. Under Belgium GAAP, a provision is recorded for

the “ Accumulated benefi t obligation” determined on an actuarial basis. At the

end of 2004, the provision w as EUR 6.5 million.

Conversion to IFRS

From the fi rst quarter of 2005 on, Delhaize Group will report its fi nancial results

under International Financial Reporting Standards (IFRS) in compliance with

the European Union Directive of M ay 27, 2002. Delhaize Group believes that it

is appropriately poised for an effi cient, accurate and timely transition to IFRS.

Delhaize Group view s this change in accounting and reporting standards as a

positive step tow ards further improving transparency in fi nancial reporting.

Delhaize Group has decided to publish two comparative years (2003 and 2004)

in its 2005 annual report to provide the users of its fi nancial statements with a

complete and understandable view on the Company’s fi nancial performance.

As a foreign listed company on the New York Stock Exchange, Delhaize Group

is required to reconcile its result to US GAAP annually, while Delhaize America,

as a SEC registrant, publishes its fi nancial statements under US GAAP quar-

terly. In order to maintain consistency across all of the fi nancial reporting by

Delhaize Group and Delhaize America, Delhaize Group has aligned its IFRS

policy decisions with US GAAP requirements as closely as feasible.

IFRS provides certain options for fi rst-time adoption as w ell as ongoing report-

ing. Delhaize Group has made the follow ing key policy decisions:

• Property, plant and equipment as well as investment property will be

recorded at amortized cost versus at market value (in line w ith US GAAP);

• All unrecognized actuarial losses and gains associated with the Group’s

defi ned benefi t pension plans will be recorded as an adjustment to equity

upon adoption of IFRS. After adoption, Delhaize Group w ill use the corridor

approach to recognize actuarial gains and losses amortizing excess gains

and losses over the remaining working lives of plan participants (in line w ith

US GAAP);

• All components of pension expense will be classifi ed as operating expenses.

No components of pension expense will be recorded in fi nancial costs (in

line w ith US GAAP);

• Delhaize Group will expense all stock options and restricted shares unvested

at January 1, 2003 using the Black-Scholes valuation method, one year ear-

lier than required (stock options w ill be expensed under US GAAP beginning

in 2005; restricted shares are currently being expensed under US GAAP);

• Joint ventures w ill be proportionately consolidated versus accounted for

under the equity method. This currently only applies to the Group’s Indonesian

operations, Lion Super Indo (under US GAAP, joint ventures are accounted for

using the equity method);

• Delhaize Group w ill apply, tw o years earlier than required, IAS 32 and 39

relating to fi nancial instruments upon adoption of IFRS which is very similar

to the accounting for fi nancial instruments under US GAAP;

• IAS 21, The Effects of Changes in Foreign Exchange Rates, will be applied

retrospectively; therefore, the cumulative translation adjustment upon con-

version to IFRS will refl ect historical fl uctuations in exchange rates; and

• The accounting for business combinations prior to the adoption of IFRS will

not be restated.

The most signifi cant changes in the income statement between Belgian

GAAP and IFRS will be:

• The presentation of the income statement by function, rather than by nature

as done under Belgian GAAP;

• The notion of exceptional items does not exist under IFRS;

• Discontinued operations will be reported on a separate line on the operating

statement;

• Goodw ill and indefi nite lived intangible assets w ill no longer be amortized

but tested annually for impairment;

• Treasury share valuation adjustments will not be recorded under IFRS; trea-

sury shares are accounted for at cost in equity under IFRS;

• Stock based compensation will be expensed using the Black-Scholes valu-

ation method. Under Belgian GAAP, compensation expense related to stock

options is not recorded, but expense is recorded for the difference betw een

the price of stock purchased in the market (when necessary to satisfy option

exercises) and the stock option exercise price;

• Under IFRS closed store related charges are based on expected settlement

while Delhaize Group has recorded these provisions using a market value

approach under Belgian GAAP; and

• Certain restructuring costs associated w ith business combinations included

in the purchase price allocation under Belgian GAAP w ill be expensed under

IFRS.