3M 2011 Annual Report Download - page 96

Download and view the complete annual report

Please find page 96 of the 2011 3M annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

90

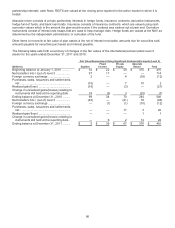

As of December 31, 2011, the Company had a balance of $22 million associated with the after tax net unrealized

gain associated with cash flow hedging instruments recorded in accumulated other comprehensive income. This

includes a $4 million balance (loss) related to a floating-to-fixed interest rate swap (discussed in the preceding

paragraph), which will be amortized over the five-year life of the note. 3M expects to reclassify a majority of the

remaining balance to earnings over the next 12 months (with the impact offset by cash flows from underlying hedged

items).

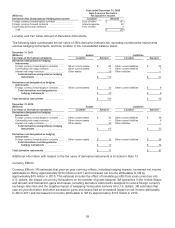

The location in the consolidated statements of income and comprehensive income and amounts of gains and losses

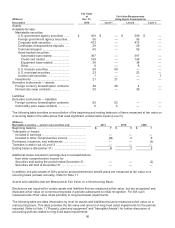

related to derivative instruments designated as cash flow hedges are provided in the following table.

Reclassifications of amounts from accumulated other comprehensive income into income include accumulated gains

(losses) on dedesignated hedges at the time earnings are impacted by the forecasted transaction.

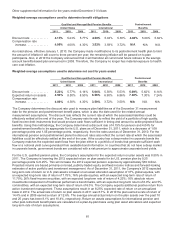

Year ended December 31, 2011

(Millions)

Derivatives in Cash Flow Hedging

Pretax Gain (Loss)

Recognized in Other

Comprehensive Income

On Effective Portion of

Derivative

Pretax Gain (Loss) Recognized

in Income on Effective Portion

of Derivative as a Result of

Reclassification from

Accumulated Other

Comprehensive Income

Ineffective Portion of Gain

(Loss) on Derivative and

Amount Excluded from

Effectiveness Testing

Recognized in Income

Relationships Amount Location Amount Location Amount

Foreign currency forward/option contracts $ 3 Cost of sales $ (87 ) Cost of sales $ —

Foreign currency forward contracts . . . (42) Interest expense (41) Interest expense

—

Commodity price swap contracts ........... (4) Cost of sales (6) Cost of sales

—

Interest rate swap contracts . . . . . . . . (7) Interest expense

—

Interest expense

—

Total ........................ $ (50 ) $ (134 ) $ —

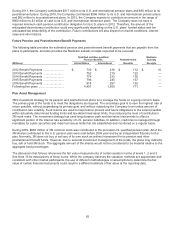

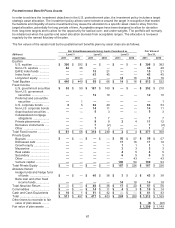

Year ended December 31, 2010

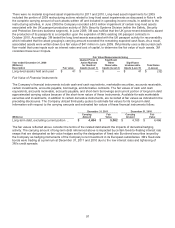

(Millions)

Derivatives in Cash Flow Hedging

Pretax Gain (Loss)

Recognized in Other

Comprehensive Income

on Effective Portion of

Derivative

Pretax Gain (Loss) Recognized

in Income on Effective Portion

of Derivative as a Result of

Reclassification from

Accumulated Other

Comprehensive Income

Ineffective Portion of Gain

(Loss) on Derivative and

Amount Excluded from

Effectiveness Testing

Recognized in Income

Relationships Amount Location Amount Location Amount

Foreign currency forward/option contracts $ (30 ) Cost of sales $ (39 ) Cost of sales $ —

Foreign currency forward contracts . . . . . 34 Interest expense 33 Interest expense —

Commodity price swap contracts . . . . . . (13 ) Cost of sales (9 ) Cost of sales —

Total .......................... $ (9 ) $ (15 ) $ —

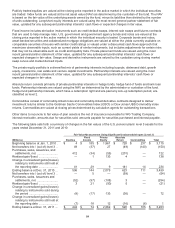

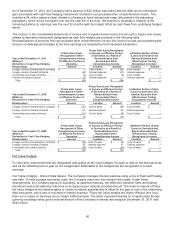

Year ended December 31, 2009

(Millions)

Derivatives in Cash Flow Hedging

Pretax Gain (Loss)

Recognized in Other

Comprehensive Income

on Effective Portion of

Derivative

Pretax Gain (Loss) Recognized

in Income on Effective Portion

of Derivative as a Result of

Reclassification from

Accumulated Other

Comprehensive Income

Ineffective Portion of Gain

(Loss) on Derivative and

Amount Excluded from

Effectiveness Testing

Recognized in Income

Relationships Amount Location Amount Location Amount

Foreign currency forward/option contracts $ (58 ) Cost of sales $ 96 Cost of sales $

—

Foreign currency forward contracts . . . . 55 Interest expense 47 Interest expense

—

Commodity price swap contracts . . . . . (18 ) Cost of sales (34 ) Cost of sales

—

Total ......................... $ (21 ) $ 109 $

—

Fair Value Hedges:

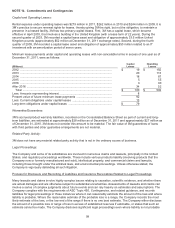

For derivative instruments that are designated and qualify as fair value hedges, the gain or loss on the derivatives as

well as the offsetting loss or gain on the hedged item attributable to the hedged risk are recognized in current

earnings.

Fair Value Hedging - Interest Rate Swaps: The Company manages interest expense using a mix of fixed and floating

rate debt. To help manage borrowing costs, the Company may enter into interest rate swaps. Under these

arrangements, the Company agrees to exchange, at specified intervals, the difference between fixed and floating

interest amounts calculated by reference to an agreed-upon notional principal amount. The mark-to-market of these

fair value hedges is recorded as gains or losses in interest expense and is offset by the gain or loss of the underlying

debt instrument, which also is recorded in interest expense. These fair value hedges are highly effective and, thus,

there is no impact on earnings due to hedge ineffectiveness. The dollar equivalent (based on inception date foreign

currency exchange rates) gross notional amount of the Company’s interest rate swaps at December 31, 2011 was

$342 million.