Tyson Foods 2001 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2001 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

|

|

38

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

TYSON FOODS, INC. 2001 ANNUAL REPORT

In October 2001, the FASB issued SFAS No. 144,

“

Accounting

for the Impairment or Disposal of Long-Lived Assets” (SFAS 144).

SFAS 144 supersedes SFAS No. 121, “Accounting for the Impairment

of Long-Lived Assets and for Long-Lived Assets to Be Disposed

Of;” however, it retains the fundamental provisions of that

Statement related to the recognition and measurement of the

impairment of long-lived assets to be “held and used.” In addi-

tion, the Statement provides more guidance on estimating cash

flows when performing a recoverability test, requires that a

long-lived asset to be disposed of other than by sale (e.g., aban-

doned) be classified as “held and used” until it is disposed of,

and establishes more restrictive criteria to classify an asset as

“held for sale.” The Company is required to adopt SFAS 144 in

fiscal year 2003.

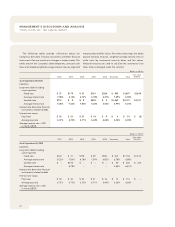

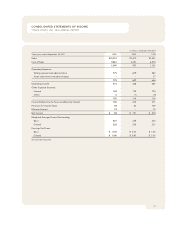

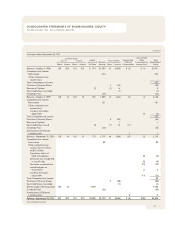

NOTE 2: ACQUISITIONS

In August 2001, the Company acquired 50.1% of IBP by paying

approximately $1.7 billion in cash representing $30 per share

for approximately 54 million shares of IBP’s common shares.

In September 2001, the Company issued approximately 129 mil-

lion shares of Class A stock, with a fair value of approximately

$1.2 billion, to acquire the remaining IBP shares, and assumed

approximately $1.7 billion of IBP debt to complete the acquisi-

tion. The IBP shares were converted into Class A stock using an

exchange ratio of 2.381. The total acquisition cost of approxi-

mately $4.6 billion was accounted for as a purchase with a

portion of the total purchase price allocated to assets acquired

and liabilities assumed based on estimated fair market value at

the date of acquisition.

IBP is the world’s largest manufacturer of fresh meats and

frozen and refrigerated food products, with 2000 annual sales of

approximately $17 billion. The acquisition of IBP will allow the

Company to expand its business to include the processing and

marketing of beef and pork products.

The transaction is being accounted for using the purchase

method of accounting required by SFAS 141. Goodwill and iden-

tifiable intangible assets recorded in the acquisition will be tested

periodically for impairment as required by SFAS 142. The alloca-

tion of the purchase price to specific assets and liabilities is based,

in part, upon an outside appraisal of IBP’s long-lived assets. The

allocation of the purchase price has been completed.

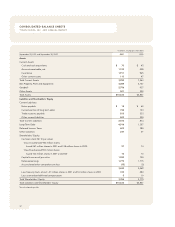

Fair value of assets acquired and liabilities assumed at

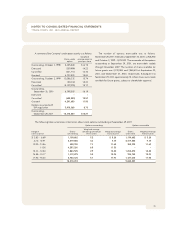

August 3, 2001:

in millions

Cash and cash equivalents

$37

Accounts receivable

641

Inventories

937

Other current assets

112

Property, plant and equipment

1,968

Goodwill

1,830

Other assets

247

Total Assets

$5,772

Accounts payable and accruals

$ 836

Other liabilities

227

Long-term debt

1,651

Deferred income taxes

221

Shareholders’ equity

2,837

Total Liabilities and Shareholders’ Equity

$5,772

Identifiable intangible assets of $242 million consist of trade-

marks of $138 million (included in goodwill), patents of $87 million

and $17 million of supply contracts (both of which are included

in other assets). The amounts associated with trademarks are

not subject to amortization as management believes their useful

lives to be indefinite. The amounts associated with patents and

supply contracts are being amortized over 15 and five years,

respectively.

In August 2001, the Company completed the financing for

the acquisition of IBP by entering into two bridge revolving credit

facilities consisting of a senior unsecured bridge credit agreement

which provided for aggregate borrowings up to $2.5 billion

(the Bridge Facility) and a senior unsecured receivables bridge

credit agreement which provided for aggregate borrowings up to

$350 million (the Receivables Bridge Facility). Subsequent to

September 29, 2001, the Company refinanced both facilities.