Tyson Foods 2001 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2001 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

|

|

37

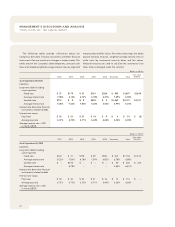

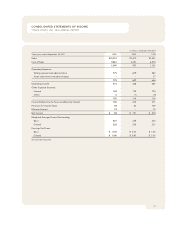

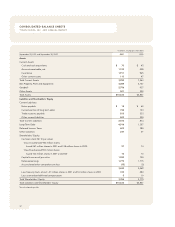

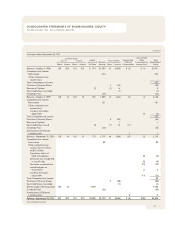

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

TYSON FOODS, INC. 2001 ANNUAL REPORT

Revenue Recognition: The Company recognizes revenue from

product sales upon delivery to customers.

Freight Expense: Freight expense associated with products

shipped to customers is recognized in cost of products sold. Prior

to the fourth quarter 2001, various freight expenses had been

classified as a reduction of net sales or as selling expense. The

effect of this reclassification was to increase revenue by $252 mil-

lion and $258 million, increase cost of sales by $410 million

and $416 million and decrease selling expense by $158 million and

$158 million in fiscal 2000 and 1999, respectively, with no changes

to net income or related earnings per share.

Advertising and Promotion Expenses: Advertising and promo-

tion expenses are charged to operations in the period incurred.

Advertising and promotion expenses for 2001, 2000 and 1999

were $337 million, $280 million and $301 million, respectively.

Minority Interest: The results of operations of IBP for the nine

weeks ended September 29, 2001, are included in the Company’s

consolidated results of operations. Minority interest primarily con-

sists of the 49.9% of IBP that was acquired on September 28, 2001.

Use of Estimates: The consolidated financial statements are

prepared in conformity with accounting principles generally

accepted in the United States which require management to

make estimates and assumptions that affect the amounts

reported in the consolidated financial statements and accom-

panying notes. Actual results could differ from those estimates.

Recently Issued Accounting Standards: In May 2000, the

Emerging Issues Task Force (EITF) reached a consensus on

Issue 00-14, “Accounting for Certain Sales Incentives.” This

issue involves the accounting and income statement classifi-

cation for sales subject to rebates and revenue sharing arrange-

ments as well as coupons and discounts. The EITF concluded

that sales incentives offered to customers to buy a product

should be classified as a reduction of sales. This issue is effec-

tive for fiscal quarters beginning after December 15, 2001.

The Company anticipates implementing this issue in the first

quarter of fiscal 2002.

In April 2001, the EITF released Issue 00-25, “Vendor Income

Statement Characterization of Consideration from a Vendor to

a Retailer,” which provides guidance on the classification of

payments such as slotting fees and cooperative advertising in

the income statement. The EITF concluded that these payments

are a reduction of the selling prices of the vendor’s products

and, therefore, should be classified as a reduction of revenue in

the vendor’s income statement, instead of as an expense. This

issue is effective for fiscal quarters beginning after December 15,

2001. The Company anticipates implementing this issue in the

first quarter of fiscal 2002.

In June 2001, the Financial Accounting Standards Board (FASB)

issued Statements of Financial Accounting Standards No. 141,

“Business Combinations” (SFAS 141), and No. 142, “Goodwill

and Other Intangible Assets” (SFAS 142). SFAS 141 eliminates the

pooling-of-interests method of accounting for business combi-

nations and requires any business combination completed after

June 30, 2001, to be accounted for by the purchase method.

Additionally, SFAS 141 changes the criteria to recognize intangible

assets apart from goodwill. Under SFAS 142, goodwill and indef-

inite lived intangible assets are no longer amortized but are

reviewed annually, or more frequently if impairment indicators

arise, for impairment. Separable intangible assets that have finite

lives will continue to be amortized over their useful lives. Because

of the different transition dates for goodwill and intangible assets

acquired on or before June 30, 2001, and those acquired after

that date, pre-existing goodwill and intangibles will be amortized

during this transition period until adoption, whereas new good-

will and other indefinite lived intangible assets acquired after

June 30, 2001, will not be amortized. Companies are required to

adopt SFAS 142 in their fiscal year beginning after December 15,

2001. The Company has applied SFAS 142 to the IBP transaction

and anticipates complete adoption in the first quarter of fiscal

2002. At that time goodwill will no longer be amortized.