Suzuki 2010 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2010 Suzuki annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

|

|

SUZUKI MOTOR CORPORATION 35

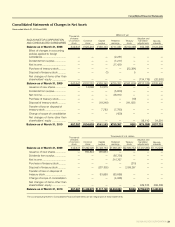

As for directors and corporate auditors of the Company, the amount to be paid at the end of scal year had been posted

pursuant to the Company’s regulations on the retirement allowance of directors and corporate auditors. However, the Com-

pany’s retirement benet system for them was abolished at the closure of the ordinary general meeting of shareholders held

on June 2006. And it was approved at ordinary general meeting of shareholders that reappointed directors and corporate

auditors are paid their retirement benet at the time of their retirement, based on their years of service. Estimated amount of

such retirement benets is appropriated at the end of this scal year.

Furthermore, for the directors and corporate auditors of some consolidated subsidiaries, the amount to be paid at the end

of the year was posted pursuant to their regulation on the retirement allowance of directors and corporate auditors.

Retirement benet cost and retirement benet obligation are calculated based on the actuarial assumptions, which include

discount rate, assumed return of investment ratio, revaluation ratio, salary rise ratio, retirement ratio and mortality ratio. Dis-

count rate is decided on the basis of yield on low-risk, long-term bonds, and assumed return of investment ratio is decided

based on the investment policies of pension assets of each pension system etc.

Decreased yield on long-term bond leads to a decrease in discount rate and has an adverse inuence on the calculation

of retirement benet cost. However, the pension system adopted by the Company has a cash balance type plan, and thus

the revaluation ratio, which is one of the base ratios, can offset any adverse effects caused by a decrease in the discount rate.

If the investment yield of pension assets is less than the assumed return of investment ratio, it will have an adverse effect

on the calculation of retirement benet cost. But by focusing on low-risk investments, this inuence should be minimal in the

case of the pension fund systems of the Company and its subsidiaries.

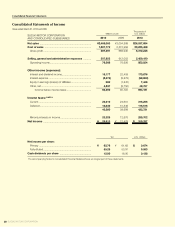

(m) Revenue recognition

Sales of products are generally recognized in the accounts as delivery is made.

(n) Net income per share

Primary net income per share is computed based on the weighted average number of shares issued during the respec-

tive years. Fully diluted net income per share is computed assuming that all convertible bonds were converted into common

stock, with an applicable adjustment for related interest expense and net of tax. Cash dividends per share are the amounts

applicable to the respective periods including dividends to be paid after the end of the period.

(o) Cash and cash equivalents

All highly liquid investments with original maturities of three months or less when purchased are considered cash and cash

equivalents.

(p) Reclassication

Certain reclassications of previously reported amounts are made to conform with current classications.

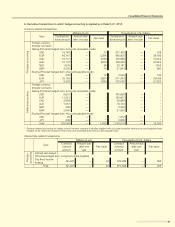

NOTE 3:Changesinbasicmattersforpreparingconsolidatednancialstatements

(a) Revenue recognition

The “Accounting Standards for Construction Contracts” (Accounting Standards Board of Japan; ASBJ Statement No.15,

December 27, 2007) and “Guidance on Accounting Standards for Construction Contracts (ASBJ Guidance No. 18, Decem-

ber 27, 2007) are applied from this scal year. The percentage-of-completion method is applied to contracts with conrmed

results for progress of construction contracts implemented during this scal year until the end of this scal year, and the

completed-contract method is applied to other contracts.

This change gives no inuences on the net sales, operating income and income before income taxes for this scal year.

(b) Applicationofthe“PartialAmendmentstoAccountingStandardforRetirementBenets(Part3)”

The “Partial Amendments to Accounting Standard for Retirement Benets (Part3)” (ASBJ Statement No.19, July 31, 2008)

is applied from this scal year.

This change gives no inuences on the operating income and income before income taxes for this scal year.

In addition, there is no balance amount of retirement benet liabilities to accrue with the application of this accounting

standard.

Consolidated Financial Statements