Redbox 2003 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2003 Redbox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

|

|

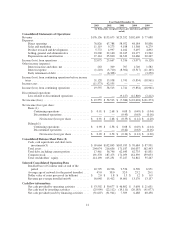

primarily of depreciation charges on Coinstar units, and to a lesser extent, depreciation on computer equipment,

leased automobiles, furniture and fixtures and leasehold improvements.

Since 1995, we have devoted significant resources to building our sales and marketing organization, adding

administrative personnel and developing the network systems and infrastructure to support the rapid growth of

our installed base of Coinstar units. The cost of this expansion and the significant depreciation expense of our

installed network resulted in significant operating losses in prior years. We have maintained an operating profit

for over a year through continuous improvements to our systems and processes. We expect to continue to

evaluate new marketing and promotional programs to increase the breadth and rate of customer utilization of our

Coinstar service. We also intend to continue to engage in systems and product research and development. We

believe our prime retail locations form a strategic platform from which we will be able to deliver additional

value-added products and services to consumers and our retail partners that may create additional revenue

streams independent of coin counting. In the future we envision the Coinstar unit as a touch-point for a range of

consumer products and services such as prepaid cards, prepaid cellular services and payroll debit cards.

We believe that our future coin-counting revenue growth, operating margin gains and profitability will

depend on the success of our efforts to increase customer usage, retain our current retail partners, expand our

installed base with retail partners in existing markets, expand into new geographies and distribution formats and

undertake ongoing marketing and promotional activities that will sustain the growth in unit coin volume over

time. Given the unpredictability of the timing of installations with retail partners and the resulting revenues, the

growth in coin processing volumes of our installed base and the continued market acceptance of our services by

consumers and retail partners, our operating results for any future periods may be subject to significant variation,

and we believe that period-to-period comparisons of our results of operations are not necessarily predictive and

should not be relied on as indications of future performance.

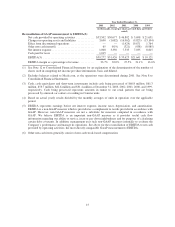

On February 6, 2003, we acquired substantially all of the assets and assumed certain liabilities of Prizm

Technologies, Inc., a privately held corporation. Prizm’s proprietary technology allows consumers to conduct a

range of automated prepaid wireless transactions at its TOP-UP™terminals, such as adding minutes to a prepaid

wireless handset. The purchase was accounted for as a business combination under the provisions of Statement of

Financial Accounting Standards (“SFAS”) No. 141, Business Combinations. The fair value of the assets acquired

and liabilities assumed were included in our financial statements as of February 6, 2003, the acquisition date. The

purchase price of this acquisition did not have a material impact on our consolidated financial position. In June

2003, we entered into an agreement with the shareholders of Prizm pursuant to which they agreed to relinquish

any claims for additional consideration in connection with the “earn-out” provisions in the asset purchase

agreement in exchange for a maximum payment of $400,000 contingent on meeting certain terms and conditions

through the end of the year. These terms and conditions were met in full and we remitted payment by December

31, 2003. Goodwill was previously recorded in accordance with SFAS No. 142, Goodwill and Other Intangible

Assets, which will be tested periodically for impairment.

On July 9, 2003, we announced that we were unable to reach mutually acceptable economic terms with

Safeway, Inc. with respect to continuing to provide Coinstar units and related services in the Safeway

supermarket chain. As a result, our contract with Safeway was terminated effective August 6, 2003. Until we

de-install all machines, we will continue to receive revenue from Coinstar units remaining in Safeway stores.

Coinstar units in Safeway stores generated approximately $13.7 million or 7.8% of our 2003 revenue. We

anticipate that approximately 1,000 machines will be de-installed from Safeway stores. We removed 90% of

our machines from Safeway supermarket locations in the third and fourth quarters of 2003 and plan to

complete the de-installation process during the first quarter of 2004. As a result of the return of the machines

from Safeway, we canceled purchase orders for additional machines.

Critical Accounting Policies and Estimates

Our discussion and analysis of our financial condition and results of operations are based upon our

consolidated financial statements, which have been prepared in accordance with accounting principles generally

17