Qantas 2015 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2015 Qantas annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

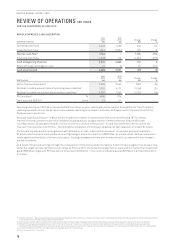

21

QANTAS ANNUAL REPORT 2015

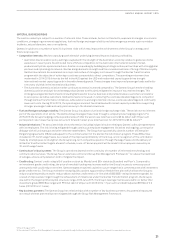

MATERIAL BUSINESS RISKS

The aviation industry is subject to a number of inherent risks. These include, but are not limited to, exposure to changes in economic

conditions, changes in government regulations, fuel and foreign exchange volatility and other exogenous events such as aviation

incidents, natural disasters, war or an epidemic.

Qantas is subject to a number of specific business risks which may impact the achievement of the Group’s strategy and

financial prospects:

–Competitive intensity: Market capacity growth ahead of underlying demand impacts industry profitability.

• Australia’s liberal aviation policy settings coupled with the strength of the Australian economy relative to global economic

weakness in recent years has attracted more offshore competitors to the Australian international aviation market,

predominantly state-sponsored airlines. Qantas is responding by building key strategic airline partnerships with strong global

partners and optimising its network. Qantas brings domestic strength and the unrivalled customer offering of Qantas Loyalty.

Qantas International has embarked on a major restructure of its legacy cost issues through the Qantas Transformation

program with the objective of achieving a cost base comparable to direct competitors. The operating environment has

moderated in 2014/2015 driven by the fall in the AUD against the USD and moderated capacity growth has brought

international market capacity growth in line with demand growth. These changes have improved passenger loads and led to

a recovery of yields in the international business.

• The Australian domestic aviation market continues to attract increased competition. The Qantas Group’s market-leading

domestic position and dual-brand strategy allow Qantas to effectively mitigate the impact of any market changes. This

strategy leverages Qantas Domestic (including QantasLink) to serve business and premium leisure customers and Jetstar

to serve price-sensitive customers. Qantas Domestic is focused on removing the cost base disadvantage to its competitor

through Qantas Transformation initiatives, while Jetstar is working to maintain its low-cost scale advantage and continually

lower unit costs. During 2014/2015, the operating environment has stabilised with market capacity moderation supporting

stronger passenger loads and early yield recovery in the domestic business.

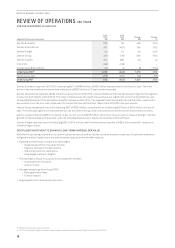

–Fuel and foreign exchange volatility: The Qantas Group is subject to fuel and foreign exchange risks. These risks are an inherent

part of the operations of an airline. The Qantas Group manages these risks through a comprehensive hedging program. For

2015/2016 the Group’s hedging profile is positioned such that the worst case total fuel cost is $3.94 billion with 73 per cent

participation rate in lower fuel prices (at current forward market price total fuel cost for 2015/2016 is $3.64 billion)58

–Industrial relations: The associated risks of transformation including industrial action relating to Qantas’ collective agreements

with its employees. The risk is being mitigated through continuous employee engagement initiatives and ongoing, constructive

dialogue with all union groups and other relevant stakeholders. The Group has successfully closed a number of Enterprise

Bargaining Agreements (EBAs) subsequent to the commencement of the Qantas Transformation program. These EBAs have

included an 18-month wage freeze. As a result of the improved profitability of the Group, and in recognition of the contribution

made by all employees to strengthen the Group’s long-term competitive position through the wage freeze and the delivery of

all Qantas Transformation targets ahead of schedule, a one-off bonus payment will be made to all employees covered by an

18-month wage freeze.

–Continuity of critical systems: The Group’s operations depend on the continuity of a number of information technology and

communication services. The Group has an extensive control and Group Risk Management Framework59 to reduce the likelihood

of outages, ensure early detection and to mitigate the impact.

–Credit rating: Qantas’ credit rating is Ba1 positive outlook by Moody’s and BB+ stable by Standard and Poor’s. Compared to

an investment grade credit rating, the price of new debt funding may increase and/or the Group’s access to some sources of

unsecured credit could reduce over time. Qantas targets an optimal capital structure range that is commensurate with investment

grade credit metrics. The Group maintains strong liquidity options supported by a flexible fleet plan which allows the Group to

reduce capital expenditure and/or reduce debt to achieve credit metrics in-line with a BBB/BBB- rating (investment grade). As

a result of improved earnings through the achievement of milestones under the Qantas Transformation program, the Group is

now within the target optimal capital structure range. At 30 June 2015, the Group’s leverage metrics were within or better than

investment grade (BBB/Baa range) with FFO/net debt of 46 per cent (2013/2014: 17 per cent) and Debt/adjusted EBITDA of 2.9

times (2013/2014: 5.1 times).

–Key business partners: The Qantas Group has relationships with a number of key business partners. Any potential exposures

as a result of these partnerships are mitigated through the Group Risk Management Framework.

58 As at 18 August 2015

59 An overview of the Group Risk Management Framework is available through the Qantas Group Business Practices Document on www.qantas.com.au