Qantas 2014 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2014 Qantas annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

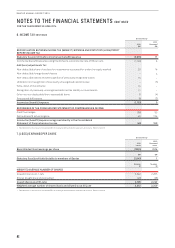

78

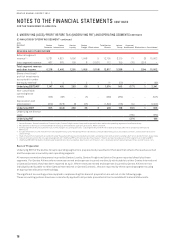

QANTAS ANNUAL REPORT 2014

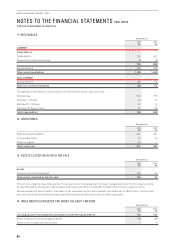

NOTES TO THE FINANCIAL STATEMENTS CONTINUED

FOR THE YEAR ENDED 30 JUNE 2014

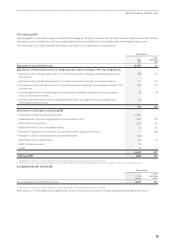

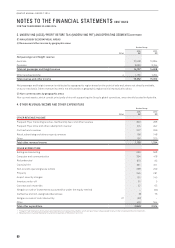

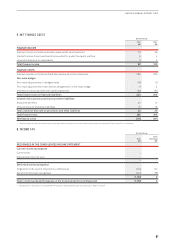

3. UNDERLYING (LOSS)/PROFIT BEFORE TAX (UNDERLYING PBT) AND OPERATING SEGMENTS CONTINUED

(D) DESCRIPTION OF UNDERLYING PBT AND RECONCILIATION FROM STATUTORY (LOSS)/PROFIT BEFORE TAX

Underlying PBT is a non-statutory measure, and is the primary reporting measure used by the Qantas Group’s chief operating

decision-making bodies, being the Chief Executive Officer, Group Management Committee and the Board of Directors. The objective

of measuring and reporting Underlying PBT is to provide a meaningful and consistent representation of the underlying performance

of each operating segment and the Group.

Underlying PBT is derived by adjusting Statutory (loss)/profit before tax for impacts of AASB 139

Financial Instruments: Recognition

and Measurement

(AASB 139) which relate to other reporting periods and identifying certain other items which are not included in

Underlying PBT.

(i) Adjusting for impacts of AASB 139 which relate to other reporting periods

All derivative transactions undertaken by the Qantas Group represent economic hedges of underlying risk and exposures.

The Qantas Group does not enter into speculative derivative transactions. Notwithstanding this, AASB 139 requires certain mark-

to-market movements in derivatives which are classified as “ineffective” to be recognised immediately in the Consolidated Income

Statement. The recognition of derivative valuation movements in reporting periods which differ from the designated transaction

causes volatility in statutory profit that does not reflect the hedging nature of these derivatives.

Underlying PBT reports all hedge derivative gains and losses in the same reporting period as the underlying transaction by adjusting

the reporting period’s statutory profit for derivative mark-to-market movements that relate to underlying exposures in other

reporting periods.

This adjustment is calculated as follows:

–Derivative mark-to-market movements recognised in the current reporting period’s statutory profit that are associated with

current year exposures remain included in Underlying PBT

–Derivative mark-to-market movements recognised in the current reporting period’s statutory profit that are associated with

underlying exposures which will occur in future reporting periods are excluded from Underlying PBT

–Derivative mark-to-market movements recognised in the current reporting period’s statutory profit that are associated with

capital expenditure are excluded from Underlying PBT and subsequently included in Underlying PBT as an implied adjustment

todepreciation expense for the related assets commencing when the assets are available for use

–Derivative mark-to-market movements recognised in previous reporting periods’ statutory profit that are associated with

underlying exposures which occurred in the current year are included in Underlying PBT

–Ineffectiveness and non-designated derivatives relating to other reporting periods affecting net finance costs are excluded

fromUnderlying PBT

All derivative mark-to-market movements which have been excluded from Underlying PBT will be recognised through Underlying PBT

in future periods when the underlying transaction occurs.

(ii) Other items not included in Underlying PBT

Items which are identified by Management and reported to the chief operating decision-making bodies as not representing the

underlying performance of the business are not included in Underlying PBT. The determination of these items is made after

consideration of their nature and materiality and is applied consistently from period to period.

Items not included in Underlying PBT primarily result from revenues or expenses relating to business activities in other reporting

periods, major transformational/restructuring initiatives, transactions involving investments and impairments of specific assets

orCGUs outside the ordinary course of business.