Motorola 2014 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2014 Motorola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

54

interest related to unrecognized tax benefits in Interest expense and penalties in Selling, general and administrative expenses in

the Company’s consolidated statements of operations.

Sales and Use Taxes: The Company records taxes imposed on revenue-producing transactions, including sales,

use, value added and excise taxes, on a net basis with such taxes excluded from revenue.

Long-term Receivables: Long-term receivables include trade receivables where contractual terms of the note

agreement are greater than one year. Long-term receivables are considered impaired when management determines collection

of all amounts due according to the contractual terms of the note agreement, including principal and interest, is no longer

probable. Impaired long-term receivables are valued based on the present value of expected future cash flows discounted at the

receivable’s effective interest rate, or the fair value of the collateral if the receivable is collateral dependent. Interest income and

late fees on impaired long-term receivables are recognized only when payments are received. Previously impaired long-term

receivables are no longer considered impaired and are reclassified to performing when they have performed under a workout or

restructuring for four consecutive quarters.

Foreign Currency: Certain of the Company’s non-U.S. operations use their respective local currency as their

functional currency. Those operations that do not have the U.S. dollar as their functional currency translate assets and liabilities

at current rates of exchange in effect at the balance sheet date and revenues and expenses using rates that approximate those

in effect during the period. The resulting translation adjustments are included as a component of Accumulated other

comprehensive loss in the Company’s consolidated balance sheets. For those operations that have the U.S. dollar as their

functional currency, transactions denominated in the local currency are measured in U.S. dollars using the current rates of

exchange for monetary assets and liabilities and historical rates of exchange for nonmonetary assets. Gains and losses from

remeasurement of monetary assets and liabilities are included in Other within Other income (expense) within the Company’s

consolidated statements of operations.

Derivative Instruments: Gains and losses on hedges of existing assets or liabilities are marked-to-market and the

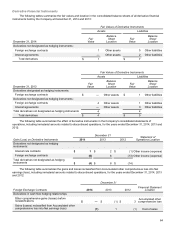

result is included in Other within Other income (expense) within the Company’s consolidated statements of operations. Certain

financial instruments are used to hedge firm future commitments or forecasted transactions. Gains and losses pertaining to

those instruments that qualify for hedge accounting are deferred until such time as the underlying transactions are recognized

and subsequently recognized in the same line within the consolidated statements of operations as the hedged item. Gains and

losses pertaining to those instruments that do not qualify for hedge accounting are recorded immediately in Other income

(expense) within the consolidated statements of operations.

Earnings Per Share: The Company calculates its basic earnings (loss) per share based on the weighted-average

effect of all common shares issued and outstanding. Net earnings (loss) attributable to Motorola Solutions, Inc. is divided by the

weighted average common shares outstanding during the period to arrive at the basic earnings (loss) per share. Diluted

earnings (loss) per share is calculated by dividing net earnings (loss) attributable to Motorola Solutions, Inc. by the sum of the

weighted average number of common shares used in the basic earnings (loss) per share calculation and the weighted average

number of common shares that would be issued assuming exercise or conversion of all potentially dilutive securities, excluding

those securities that would be anti-dilutive to the earnings (loss) per share calculation. Both basic and diluted earnings (loss) per

share amounts are calculated for earnings (loss) from continuing operations and net earnings attributable to Motorola Solutions,

Inc. for all periods presented.

Share-Based Compensation Costs: The Company has incentive plans that reward employees with stock options,

stock appreciation rights, restricted stock and restricted stock units, as well as an employee stock purchase plan. The amount of

compensation cost for these share-based awards is generally measured based on the fair value of the awards as of the date that

the share-based awards are issued and adjusted to the estimated number of awards that are expected to vest. The fair values of

stock options and stock appreciation rights are generally determined using a Black-Scholes option pricing model which

incorporates assumptions about expected volatility, risk free rate, dividend yield, and expected life. Compensation cost for share-

based awards is recognized on a straight-line basis over the vesting period.

Retirement Benefits: The Company records annual expenses relating to its pension benefit and postretirement plans

based on calculations which include various actuarial assumptions, including discount rates, assumed asset rates of return,

compensation increases, turnover rates and health care cost trend rates. The Company reviews its actuarial assumptions on an

annual basis and makes modifications to the assumptions based on current rates and trends. The effects of the gains, losses,

and prior service costs and credits are amortized either over the average service life or over the average remaining lifetime of

the participants, depending on the number of active employees in the plan. The funded status, or projected benefit obligation

less plan assets, for each plan, is reflected in the Company’s consolidated balance sheets using a December 31 measurement

date.

Advertising Expense: Advertising expenses, which are the external costs of marketing the Company’s products, are

expensed as incurred. Advertising expenses were $61 million, $76 million and $80 million for the years ended December 31,

2014, 2013 and 2012, respectively.

Recent Accounting Pronouncements: In May 2014, the FASB issued ASU No. 2014-09, "Revenue from Contracts

with Customers." This new standard will replace most existing revenue recognition guidance in U.S. GAAP. The core principle of

the ASU is that an entity should recognize revenue for the transfer of goods or services equal to the amount it expects to receive

for those goods and services. The ASU requires additional disclosure about the nature, amount, timing and uncertainty of

revenue and cash flows arising from customer contracts, including significant judgments and estimates, and changes in those