Lumber Liquidators 2009 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2009 Lumber Liquidators annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

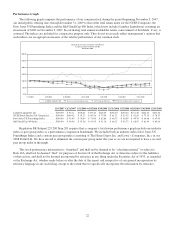

comparable store base on the first day of the thirteenth full calendar month after they open. Various factors affect comparable

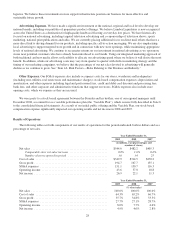

store net sales, including:

• consumer preferences, buying trends and overall economic trends and our ability to anticipate and respond

effectively to changes therein;

• changes in product assortment and the overall sales mix;

• the number of stores we open in existing markets;

• the maturity of a comparable store;

• competition;

• pricing;

• product availability and quality;

• the timing of our advertising promotional events and/or timing of three-day Holiday weekends; and

• weather and other climatological effects.

We believe increases in baseline store volumes and new store openings in existing markets, which tend to open at a

higher base level of net sales, will generally result in future comparable store net sales increases lower than increases in 2007

and earlier years. See “Item 1A. Risk Factors—Risks Related to Our Business and Industry.”

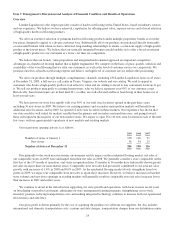

Gross Profit and Gross Margin. Gross profit is equal to our net sales minus our cost of sales, and gross margin is equal

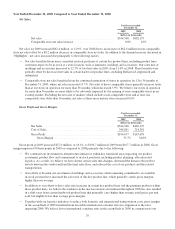

to gross profit as a percentage of net sales. Our gross profit has historically been affected by, among other things:

• our sales volumes and the margins on products we sell;

• the mix of our products sold and the related cost of that merchandise, including, in particular, the cost of hardwood

and other flooring products and accessories;

• transportation costs, both from our suppliers to our distribution centers or stores and from our distribution centers

to our stores, which may vary with factors such as international container rates and fuel costs;

• customs and duty charges on international purchases;

• the cost of third-party carrier services providing customer deliveries;

• in-house finishing costs, particularly for our Bellawood brand;

• the costs of providing samples requested by our customers;

• inventory adjustments, including shrinkage;

• the extent of any retail price reductions and the volume of inventory impacted by sales and promotional events; and

• competition.

We try to minimize the volatility of hardwood prices, which represents the largest portion of our cost of sales, by relying

on our close relationships with our suppliers and utilizing our financial flexibility to establish beneficial payment terms.

Generally, we strive to match merchandise purchase lead times with anticipated demand to maximize sustainable gross

margins, and those lead times currently range by product from approximately 90 to 180 days.

We work to improve gross profit and gross margin on an ongoing basis through inventory management improvements,

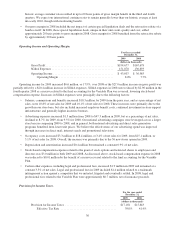

logistics alternatives, pricing levels, promotional activities and vendor relationships, among other things. Several of our

recent initiatives to position our business for more effective future growth have also had a significant impact on our gross

margins, and we continue to assess various opportunities. We review our inventory levels and sales mix on a regular basis to

identify slow-moving merchandise and products which do not meet our quality standards and cannot be sold at full price, and

generally use promotional events and mark-downs to clear such inventory. We believe that, taken together, the changes we

have made and intend to implement should enable us to sustain and gradually increase our gross margins in future periods.

Our gross profit and gross margin may not be comparable to other companies that record different costs as components of

cost of sales.

Selling, General and Administrative Expenses.

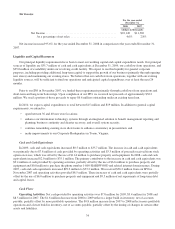

Labor Costs. One of the largest components of our selling, general and administrative (“SG&A”) expenses is labor.

The majority of our labor costs, which include salaries, commissions and benefits, relate to staff at our stores and in our

distribution network. In recent years, however, labor costs have increased as we enhanced our store support and operational

infrastructure, including key areas impacting our gross margin such as merchandise planning, product allocation and

27