Energizer 2006 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2006 Energizer annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

|

|

ENR 2006 ANNUAL REPORT 27

performs undiscounted cash flow analyses to determine if impairment

exists. If impairment is determined to exist, any related impairment loss

is calculated based on fair value. Impairment losses on assets to be

disposed of, if any, are based on the estimated proceeds to be received,

less cost of disposal.

Revenue Recognition The Company’s revenue is from the sale of its

products. Revenue is recognized when title, ownership and risk of loss

passes to the customer. Discounts are offered to customers for early

payment and an estimate of such discounts is recorded as a reduction

of net sales in the same period as the sale. Our standard sales terms

are final and returns or exchanges are not permitted unless a special

exception is made; reserves are established and recorded in cases

where the right of return does exist for a particular sale. The Company

offers a variety of programs, primarily to its retail customers, designed

to promote sales of its products. Such programs require periodic pay-

ments and allowances based on estimated results of specific programs

and are recorded as a reduction to net sales. The Company accrues at

the time of sale the estimated total payments and allowances associated

with each transaction. Additionally, the Company offers programs

directly to consumers to promote the sale of its products. Promotions

which reduce the ultimate consumer sale prices are recorded as a

reduction of net sales at the time the promotional offer is made, generally

using estimated redemption and participation levels. The Company con-

tinually assesses the adequacy of accruals for customer and consumer

promotional program costs not yet paid. To the extent total program

payments differ from estimates, adjustments may be necessary.

Historically, these adjustments have not been material.

Advertising and Promotion Costs The Company advertises and

promotes its products through national and regional media and expenses

such activities in the year incurred.

Reclassifications Certain reclassifications have been made to the

prior year financial statements to conform to the current presentation.

Recently Issued Accounting Pronouncements In 2006, the FASB

issued FASB Interpretation No. 48, “Accounting for Uncertainty in

Income Taxes” (FIN 48). FIN 48 clarifies the treatment of uncertain

income tax positions in accordance with FASB Statement No. 109,

“Accounting for Income Taxes.” The interpretation prescribes a recog-

nition threshold and measurement attribute for the financial statement

recognition and measurement of a tax position taken or expected to be

taken in a tax return. It also provides guidance on derecognition, clas-

sification, interest and penalties, accounting for taxes in interim periods

and disclosure requirements. FIN 48 is effective for the Company on

October 1, 2007. The Company has not completed assessing the impact

that FIN 48 will have on the Consolidated Financial Statements.

The FASB issued SFAS No. 154, “Accounting Changes and

Error Corrections – a replacement of APB Opinion No. 20 and FASB

Statement No. 3” (SFAS 154), which requires retrospective application

to prior periods’ financial statements of changes in accounting principle,

unless it is impracticable to determine either the period-specific effects

or the cumulative effect of the change. It also requires that a change

in depreciation, amortization or depletion method for long-lived, non-

financial assets be accounted for as a change in accounting estimate

effected by a change in accounting principle. It is effective for the

Company on October 1, 2006. The Company is not currently contem-

plating an accounting change or aware of any errors that would be

impacted by SFAS 154.

In February 2006, the FASB issued SFAS 155, “Accounting for

Certain Hybrid Financial Instruments, and amendment of FASB

Statement No. 133 and 140” (SFAS 155). SFAS 155 permits, among

other things, an election to record hybrid financial instruments that

contain an embedded derivative at fair value rather than bifurcating the

instrument for accounting purposes, as required by previous standards.

SFAS 155 is effective for the Company as of the beginning of fiscal

2007. The Company has not yet completed its evaluation of the impact

of adopting SFAS 155 on its Consolidated Financial Statements, but

does not expect such impact to be material.

In September 2006, the FASB issued SFAS No. 157, “Fair Value

Measurements” (SFAS 157), which addresses how fair value should

be measured when required for recognition or disclosure purposes

under GAAP. It also establishes a fair value hierarchy and will require

expanded disclosures on fair value measurements. SFAS 157 is

effective for the Company on October 1, 2008. The Company has not

completed assessing the impact that SFAS 157 will have on the

Consolidated Financial Statements.

In September 2006, the FASB issued SFAS No. 158, “Employers’

Accounting for Defined Benefit Pension and Other Postretirement

Plans – an amendment of FASB Statements No. 87, 88, 106 and 132(R)”

(SFAS 158). SFAS 158 improves financial reporting by requiring an

employer to recognize the overfunded or underfunded status of a

defined benefit pension and a postretirement plan as an asset or

liability in its statement of financial position. The changes in funded

status in that year are required to go through other comprehensive

income. Additional disclosure will also be required on certain effects on

net periodic benefit cost for the next fiscal year that arise from delayed

recognition of the gains or losses, prior service costs or credits, and

transition asset or obligation. SFAS 158 is effective for the Company at

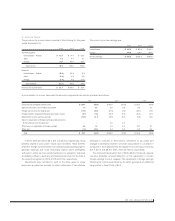

the end of fiscal 2007. We currently estimate that the impact of SFAS

158 will be an additional net pension liability of $58.9, will reduce the

postretirement liability by $37.1 and impact total shareholders equity by

$17.7 based upon valuations as of September 30, 2006.

In September 2006, the U.S. Securities and Exchange Commission

(SEC) issued Staff Accounting Bulletin No. 108, “Quantifying Financial

Statement Misstatements” (SAB 108), which provides interpretive

guidance on how registrants should quantify misstatements when

evaluating the materiality of financial statement errors. SAB 108 also

provides transition accounting and disclosure guidance for situations

in which a material error existed in prior period financial statements

by allowing companies to restate prior period financial statements or

recognize the cumulative effect of initially applying SAB 108 through

an adjustment to beginning retained earnings in the year of adoption.

SAB 108 is effective for the Company in fiscal 2007. The Company has

not completed assessing the impact that SAB 108 will have on the

Consolidated Financial Statements.