Energizer 2001 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2001 Energizer annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

|

|

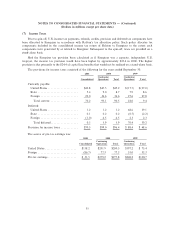

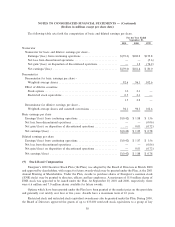

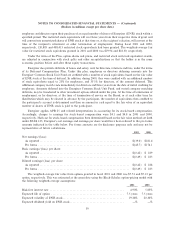

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS Ì (Continued)

(Dollars in millions except per share data)

Goodwill and Other Intangible Assets Ó Amortization of goodwill, representing the excess of cost over the

net tangible assets of acquired businesses, is recorded on a straight-line basis primarily over a period of

25 years, with some amounts being amortized over 40 years. The cost to purchase or develop other intangible

assets, which consist primarily of patents, tradenames and trademarks, is amortized on a straight-line basis

over estimated periods of related beneÑt ranging from seven to 40 years.

Impairment of Long-Lived Assets Ó Energizer reviews long-lived assets, including goodwill and other

intangible assets, for impairment whenever events or changes in business circumstances indicate that the

remaining useful life may warrant revision or that the carrying amount of the long-lived asset may not be fully

recoverable. Energizer performs undiscounted cash Öow analyses to determine if impairment exists. If

impairment is determined to exist, any related impairment loss is calculated based on fair value. Impairment

losses on assets to be disposed of, if any, are based on the estimated proceeds to be received, less costs of

disposal.

Revenue Recognition Ó Revenue is recognized in accordance with terms of sale, which is generally upon

shipment of product to or upon receipt of product by customers. Energizer provides its customers a variety of

programs designed to promote sales of its products. Promotional payments and allowances that represent

primarily a reduction in price paid by either a retail customer, distributor, wholesaler or ultimate consumer are

recorded in net sales. The provision for doubtful accounts is included in selling, general and administrative

expenses in the Consolidated Statement of Earnings.

Advertising and Promotion Costs Ó Energizer advertises and promotes its products through national and

regional media. Energizer expenses advertising and promotion in the year such costs are incurred. Due to the

seasonality of the business, with typically higher sales and volume during the holidays in the Ñrst quarter,

advertising and promotion costs incurred during interim periods are generally expensed ratably in relation to

revenues.

ReclassiÑcations Ó Certain reclassiÑcations have been made to the prior year Ñnancial statements to

conform to the current presentation.

Recently Issued Accounting Pronouncements Ó In 2001, the FASB issued Statement of Financial

Accounting Standards No. 141 (SFAS 141), ""Business Combinations.'' SFAS 141 requires that the purchase

method of accounting be used for all business combinations initiated after June 30, 2001 and establishes

speciÑc criteria for recognition of intangible assets separately from goodwill. For business combinations

initiated after June 30, 2001, SFAS 141 also requires that unallocated negative goodwill be written oÅ

immediately as an extraordinary gain. Energizer is currently evaluating the impact of SFAS 141 on its

Ñnancial statements.

Also in 2001, the FASB issued Statement of Financial Accounting Standards No. 142 (SFAS 142),

""Goodwill and Other Intangible Assets.'' SFAS 142 eliminates the amortization of goodwill and instead

requires goodwill be tested for impairment annually at the reporting unit level. Also, intangible assets are

required to be amortized over their useful lives and reviewed for impairment in accordance with Statement of

Financial Accounting Standards 121, ""Accounting for the Impairment of Long-Lived Assets and for Long-

Lived Assets to Be Disposed Of.'' Under SFAS 142, if the intangible asset has an indeÑnite useful life, it is not

amortized until its life is determined to be Ñnite. Energizer is required to adopt SFAS 142 no later than the

Ñrst quarter of Ñscal 2003, but is permitted to adopt as of the Ñrst quarter of Ñscal 2002. Energizer is currently

evaluating the impact of SFAS 142 on its Ñnancial statements.

The FASB issued SFAS No. 143, ""Accounting for Asset Retirement Obligations'' (SFAS 143) in 2001.

SFAS 143 addresses Ñnancial accounting and reporting for obligations associated with the retirement of

tangible long-lived assets and the associated asset retirement costs. Energizer is required to adopt SFAS 143

no later than the Ñrst quarter of Ñscal 2003, but is permitted to adopt earlier. Energizer is currently evaluating

the impact of SFAS 143 on its Ñnancial statements.

31