Dell 2004 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2004 Dell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

Table of Contents

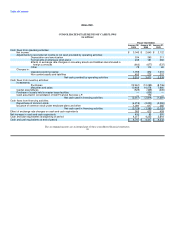

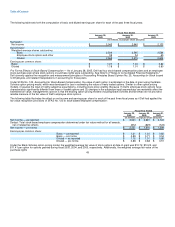

April 15, 2008 and $300 million maturing April 15, 2028. The floating rates are based on three-month London Interbank Offered Rates plus

0.41% and 0.79% for the Senior Notes and Senior Debentures, respectively. As a result of the interest rate swap agreements, Dell's effective

interest rates for the Senior Notes and Senior Debentures were 2.059% and 2.392%, respectively, for fiscal 2005.

The interest rate swap agreements are designated as fair value hedges, and the terms of the swap agreements and hedged items are such that

effectiveness can be measured using the short-cut method defined in SFAS No. 133. The differential to be paid or received on the interest rate

swap agreements is accrued and recognized as an adjustment to interest expense as interest rates change. The difference between Dell's

carrying amounts and fair value of its long-term debt and related interest rate swaps was not material at January 28, 2005 and January 30,

2004.

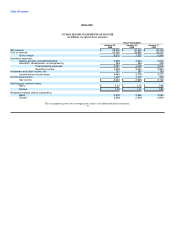

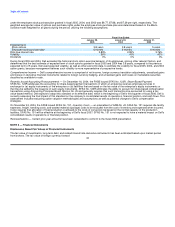

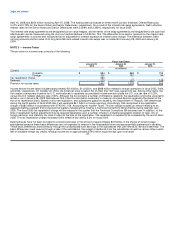

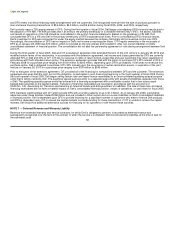

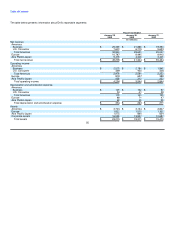

NOTE 3 — Income Taxes

The provision for income taxes consists of the following:

Fiscal Year Ended

January 28, January 30, January 31,

2005 2004 2003

(in millions)

Current:

Domestic $ 984 $ 969 $ 702

Foreign 209 132 94

Tax repatriation charge 280 — —

Deferred (71) (22) 109

Provision for income taxes $ 1,402 $ 1,079 $ 905

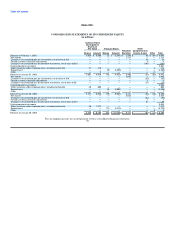

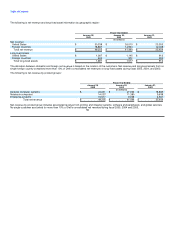

Income before income taxes included approximately $2.4 billion, $1.6 billion, and $968 million related to foreign operations in fiscal 2005, 2004,

and 2003, respectively. On October 22, 2004, the American Jobs Creation Act of 2004 (the "Act") was signed into law. Among other items, the

Act creates a temporary incentive for U.S. multinationals to repatriate accumulated income earned outside the U.S. at a tax rate of 5.25%,

versus the U.S. federal statutory rate of 35%. Although the Act contains a number of limitations related to the repatriation and some uncertainty

remains, as of January 28, 2005 Dell believes that it has the information necessary to make an informed decision regarding the impact of the

Act on its repatriation plans. Based on this new legislation, and subsequent guidance issued by the Department of Treasury, Dell determined

during the fourth quarter of fiscal 2005 that it will repatriate $4.1 billion in foreign earnings. Accordingly, Dell recognized a tax repatriation

charge of $280 million in accordance with SFAS No. 109, Accounting for Income Taxes. This tax charge includes an amount relating to an

apparent drafting oversight that Congressional leaders indicate will be fixed by a Technical Corrections Bill sometime during calendar year

2005. The fiscal 2005 tax repatriation charge will be reduced in the quarter that the Technical Corrections Bill becomes law. In addition, at the

time of repatriation further adjustment may be required depending upon a number of factors, including geographic location of cash, mix of

foreign earnings, and statutory tax rates in effect at the time of the repatriation. The repatriation is required to be completed by the end of fiscal

2006. This tax repatriation charge increased Dell's effective tax rate by 6.3% for fiscal 2005.

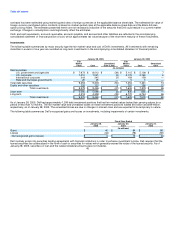

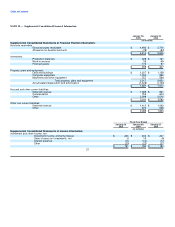

Deferred taxes have not been provided on excess book basis in the amount of approximately $2.9 billion in the shares of certain foreign

subsidiaries because these basis differences are not expected to reverse in the foreseeable future and are essentially permanent in duration.

These basis differences arose primarily through the undistributed book earnings of the subsidiaries that Dell intends to reinvest indefinitely. The

basis differences could reverse through a sale of the subsidiaries, the receipt of dividends from the subsidiaries as well as various other events.

Net of available foreign tax credits, residual income tax of approximately $740 million would be due upon a reversal

47