Columbia Sportswear 2011 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2011 Columbia Sportswear annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

|

|

We expect to fund our future capital expenditures with existing cash, operating cash flows and credit

facilities. If the need arises, we may need to seek additional funding. Our ability to obtain additional financing

will depend on many factors, including prevailing market conditions, our financial condition, and our ability to

negotiate favorable terms and conditions. Financing may not be available on terms that are acceptable or

favorable to us, if at all.

Our operations are affected by seasonal trends typical in the outdoor apparel industry, and have historically

resulted in higher sales and profits in the third and fourth calendar quarters. This pattern has resulted primarily

from the timing of shipments of fall season products to wholesale customers and proportionally higher sales from

our direct-to-consumer operations in the fourth quarter. We believe that our liquidity requirements for at least the

next 12 months will be adequately covered by existing cash, cash provided by operations and existing short-term

borrowing arrangements.

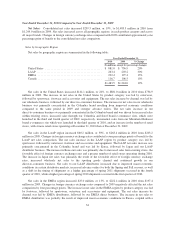

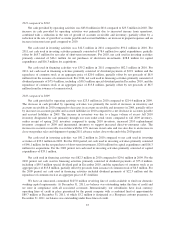

The following table presents our estimated contractual commitments (in thousands):

Year ended December 31,

2012 2013 2014 2015 2016 Thereafter Total

Inventory purchase obligations (1) . . . $351,854 $ — $ — $ — $ — $ — $351,854

Operating leases (2) ............... 38,773 35,060 29,819 26,892 25,254 94,892 250,690

(1) See Inventory Purchase Obligations in Note 13 of Notes to Consolidated Financial Statements.

(2) See Operating Leases in Note 13 of Notes to Consolidated Financial Statements.

We have recorded liabilities for net unrecognized tax benefits related to income tax uncertainties in our

Consolidated Balance Sheet at December 31, 2011 of approximately $15.4 million; however, they have not been

included in the table above because we are uncertain about whether or when these amounts may be settled. See

Note 10 of Notes to Consolidated Financial Statements.

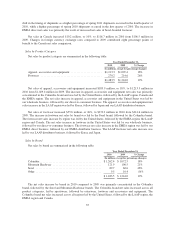

Quantitative and Qualitative Disclosures About Market Risk

In the normal course of business, our financial position and results of operations are routinely subject to a

variety of risks. These risks include risks associated with global financial and capital markets, primarily currency

exchange rate risk and, to a lesser extent, interest rate risk and equity market risk. We regularly assess these risks

and have established policies and business practices designed to mitigate the effect of these risks. We do not

engage in speculative trading in any financial or capital market.

Our primary currency exchange rate risk management objective is to mitigate the uncertainty of anticipated

cash flows attributable to changes in exchange rates. We focus on mitigating changes in functional currency

equivalent cash flows resulting from anticipated U.S. dollar denominated inventory purchases by subsidiaries

that use European euros, Canadian dollars, Japanese yen or Korean won as their functional currency. We manage

this risk primarily by using currency forward and option contracts. Additionally, we use foreign currency forward

and option contracts to hedge net balance sheet exposures related primarily to intercompany transactions and

borrowing arrangements.

The net fair value of our derivative contracts was favorable by approximately $4.5 million at December 31,

2011. A 10% exchange rate change in the euro, Canadian dollar, yen and won against the U.S. dollar would have

resulted in the net fair value declining by approximately $17.0 million at December 31, 2011. A 10% exchange

rate change in the yen and won against the euro would have resulted in the net fair value declining approximately

$4.2 million at December 31, 2011. Changes in fair value resulting from foreign exchange rate fluctuations

would be substantially offset by the change in value of the underlying hedged transactions.

38