Chrysler 2002 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2002 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

|

|

Sales performance

In Western Europe, demand for commercial vehicles totaled

650,500 units in 2002, or 5.7% less than in 2001. Only Italy

reversed the trend (+11.1%), due mainly to the positive impact

of the investment incentives provided by the Tremonti Bis Law.

New registrations of light commercial vehicles (GVW between

3.5 and 6 tons) were down 2.2% to 355,000 units. The decrease

in demand that occurred in all major European markets was

offset only in part by a substantial gain in Italy (+13.8%), and

asteady performance in Great Britain (+3.0%).

Demand for medium vehicles (GVW between 6.1 and 15.9 tons)

decreased by 8.6% to 81,800 units.

The negative impact of sharp decreases in Germany and Great

Britain (-16.5% and -8.6%, respectively) was only partially offset

by a 17.8% increase in Italy.

With 213,700 new units registered in 2002, the market for heavy

vehicles (GVW ≥16 tons) contracted by 9.9%, with particularly

steep declines in Germany (-14.7%), France (-12.3%) and Great

Britain (-6.5%). Only Italy recorded a gain, with demand

increasing by 2.7%.

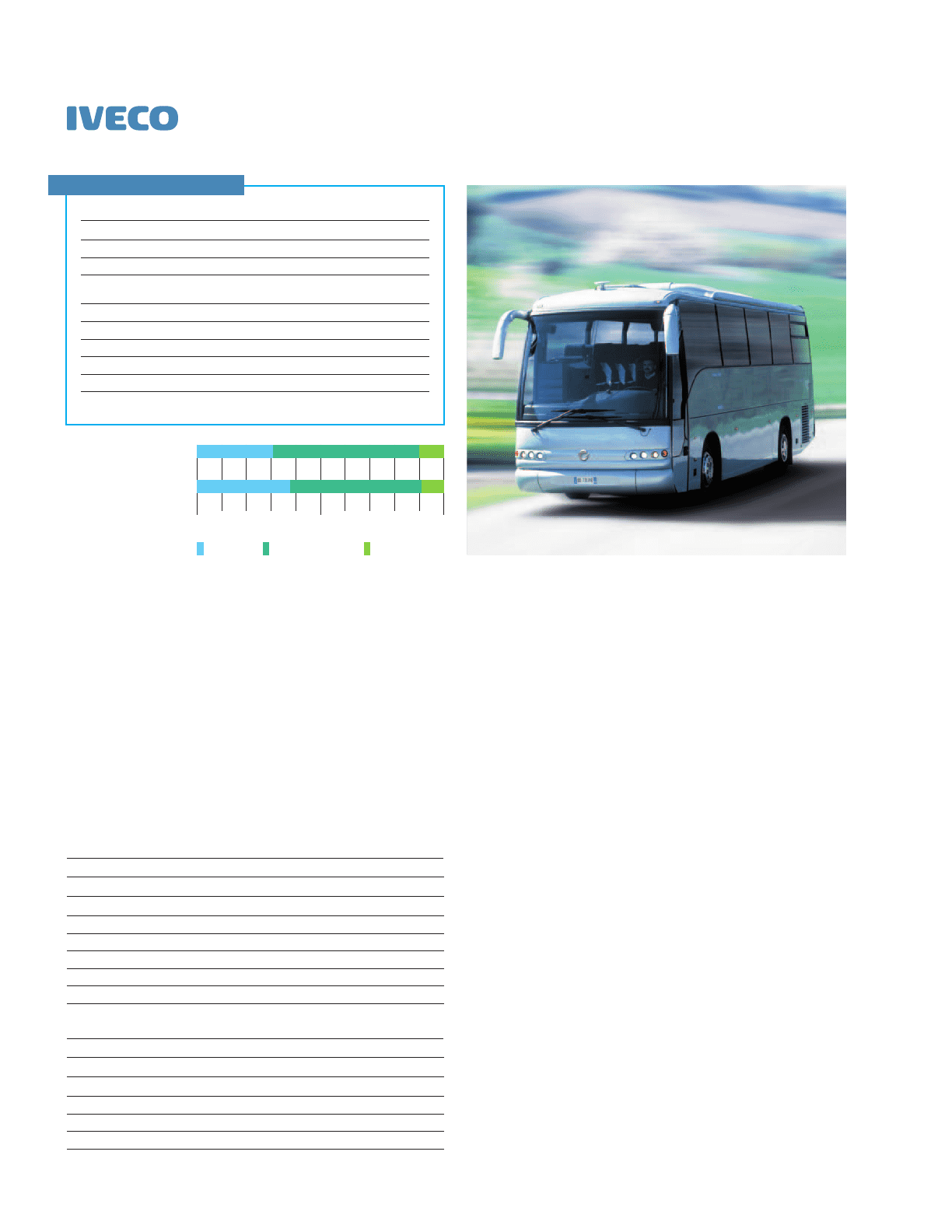

Iveco sold 161,883 vehicles worldwide, or approximately 0.9%

more than in 2001. The Sector’s licensee associated companies

shipped approximately 37,500 vehicles, or 9.3% more than in

2001. In Western Europe, the Sector sold 128,760 vehicles,

or about the same as in 2001 (-3.0% on a comparable basis).

The main reason for this reduction was a decline in the French

market, where the Sector experienced a sharp 23.1% drop in

unit sales, due in part to a more selective approach in signing

new contracts with buyback clauses, and to weak demand in

Germany (-8.0%). These decreases were offset by positive

performances in Italy and Great Britain.

Iveco’s share of a contracting Western European market for

vehicles with a curb weight equal to or greater than 3.5 tons

increased to 17.9% (+0.9 percentage points). The main reason

for this achievement is the Sector’s outstanding performance

in the medium-vehicle segment, in which Iveco became the

European market leader with a penetration of more than 30%

(+5.3 percentage points). The Sector’s share of the heavy-vehicle

segment also improved, rising by 1.3 percentage points to

12.3%. This improvement reflects the success of the new

Stralis, which was named Truck of the Year 2003.

Iveco’s performance in the light vehicle segment (market share

of 18.5%) was comparable with 2001, owing in part to an upturn

49 Report on Operations

Commercial Vehicles — Iveco

(in millions of euros)

2002

2001 2000

Net revenues 9,136 8,650 8,611

Operating result 102 271 489

EBIT (409)46 422

Net result before

minority interest (493)(123) 147

Cash flow (70)287 569

Capital expenditures (*) 587 718 656

Research and development 239 215 227

Net invested capital 1,582 1,979 2,207

Number of employees 38,113 35,340 35,852

(*) Vehicles under long-term rentals

331

348 306

Highlights

Revenues by geographical

region of destination

Italy Rest of Europe Rest of the world

Employees by geographical

region

050% 100%

Commercial Vehicles Market (GVW ≥3.5 tons)

(in thousands of units) 2002 2001 % change

France 113.4 123.1 (7.9)

Germany 125.8 140.4 (10.4)

Great Britain 116.9 118.6 (1.5)

Italy 105.0 94.6 11.1

Spain 68.9 72.8 (5.4)

Western Europe 650.5 689.7 (5.7)

Commercial Vehicles Market (GVW ≥3.5 tons)

(in thousands of units) 2002 2001 % change

Heavy 213.7 237.3 (9.9)

Medium 81.8 89.5 (8.6)

Light 355.0 362.9 (2.2)

Western Europe 650.5 689.7 (5.7)