CarMax 2001 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2001 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

|

|

45

CIRCUIT CITY STORES, INC. 2001 ANNUAL REPORT

Circuit City Stores, Inc.

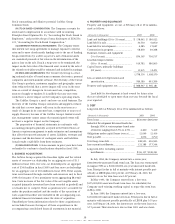

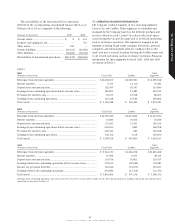

hypothetical effect on the fair value of those interests when

there are unfavorable variations from the assumptions used. Key

economic assumptions at February 28, 2001, are not materially

different than assumptions used to measure the fair value of

retained interests at the time of securitization. These sensitivi-

ties are hypothetical and should be used with caution. In this

table, the effect of a variation in a particular assumption on the

fair value of the retained interest is calculated without changing

any other assumption; in reality, changes in one factor may

result in changes in another, which might magnify or counter-

act the sensitivities.

Impact on Impact on

Assumptions Fair Value Fair Value

(Dollar amounts Used of 10% of 20%

in thousands) (Annual) Adverse Change Adverse Change

Payment rate ........... 7.1—11.3% $10,592 $20,107

Default rate.............. 7.0—14.3% $21,159 $42,318

Discount rate........... 10.0 —15.0% $ 2,973 $ 5,892

(B) AUTOMOBILE LOAN SECURITIZATIONS: The Company also

has an asset securitization program, operated through a special

purpose subsidiary on behalf of the CarMax Group, to finance

the consumer installment credit receivables generated by its

automobile loan finance operation. This automobile loan securi-

tization program had a total program capacity of $450 million

as of February 28, 2001, with no recourse provisions. In October

1999, the Company formed a second securitization facility that

allowed for a $644 million securitization of automobile loan

receivables in the public market. Because of the amortization of

the automobile loan receivables and corresponding securities in

this facility, the program had a capacity of $329 million as of

February 28, 2001, with no recourse provisions. In January

2001, the Company sold $655 million of receivables in the pub-

lic market through an additional owner trust structure. The pro-

gram had a capacity of $655 million as of February 28, 2001,

with no recourse provisions. In these securitizations, the

Company retains servicing rights and subordinated interests.

The Company’s retained interests are subject to credit and pre-

payment risks on the transferred financial assets.

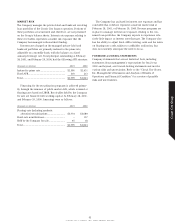

At February 28, 2001, the total principal amount of loans

managed or securitized was $1,296 million. Of the total loans,

the principal amount of loans securitized was $1,284 million and

the principal amount of loans held for sale or investment was

$12 million. The principal amount of loans that were 31 days or

more delinquent was $18.1 million at February 28, 2001. The

credit losses net of recoveries were $7.2 million for fiscal 2001.

The Company receives annual servicing fees approximating

1 percent of the outstanding principal balance of the securitized

automobile loans and rights to future cash flows arising after the

investors in the securitization trust have received the return for

which they contracted. The servicing fee specified in the auto-

mobile loan securitization agreements adequately compensates

the finance operation for servicing the accounts. Accordingly, no

servicing asset or liability has been recorded.

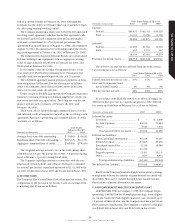

The table below summarizes certain cash flows received from

and paid to securitization trusts:

Year Ended

(Amounts in thousands) February 28, 2001

Proceeds from new securitizations ................................ $619,525

Proceeds from collections reinvested

in previous automobile loan securitizations........... $313,827

Servicing fees received ................................................... $ 10,474

Other cash flows received on retained interests*......... $ 39,265

* This amount represents total cash flows received from retained interests by

the transferor other than servicing fees, including cash flows from interest-only

strips and cash above the minimum required level in cash collateral accounts.

In determining the fair value of retained interests, the

Company estimates future cash flows using management’s best

estimates of key assumptions such as finance charge income,

default rates, prepayment rates and discount rates. The Company

employs a risk-based pricing strategy that increases the stated

annual percentage rate for accounts that have a higher predicted

risk of default. Accounts with a lower risk profile also may qual-

ify for promotional financing.

Rights recorded for future finance income from serviced

assets that exceed the contractually specified servicing fees are

carried at fair value and amounted to $42.0 million at February

28, 2001, and are included in net accounts receivable. Gains on

sales of $35.4 million were recorded in fiscal 2001.

The fair value of retained interests at February 28, 2001, was

$74.1 million with a weighted-average life ranging from 1.5 years

to 1.8 years. The table below shows the key economic assumptions

used in measuring the fair value of retained interests at February

28, 2001, and a sensitivity analysis showing the hypothetical

effect on the fair value of those interests when there are unfavor-

able variations from the assumptions used. Key economic assump-

tions at February 28, 2001, are not materially different than

assumptions used to measure the fair value of retained interests at

the time of securitization. These sensitivities are hypothetical and

should be used with caution. In this table, the effect of a variation

in a particular assumption on the fair value of the retained interest

is calculated without changing any other assumption; in reality,

changes in one factor may result in changes in another, which

might magnify or counteract the sensitivities.

Impact on Impact on

Assumptions Fair Value Fair Value

(Dollar amounts Used of 10% of 20%

in thousands) (Annual) Adverse Change Adverse Change

Prepayment speed..... 1.5 —1.6% $1,840 $3,864

Default rate ................ 1.0 —1.2% $1,471 $3,050

Discount rate.............. 12.0% $ 890 $1,786