Westjet 2014 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2014 Westjet annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

|

|

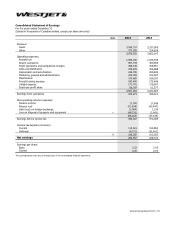

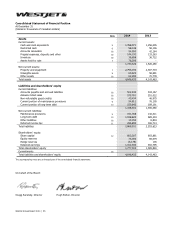

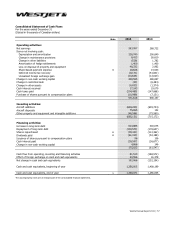

Notes to Consolidated Financial Statements

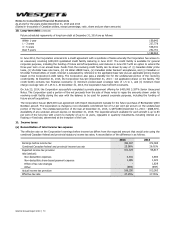

As at and for the years ended December 31, 2014 and 2013

(Stated in thousands of Canadian dollars, except percentage, ratio, share and per share amounts)

WestJet Annual Report 2014 │ 64

1. Statement of significant accounting policies (continued)

(l) Intangible assets

Included in intangible assets are costs related to software, landing rights and other. Software and landing rights are carried at

cost less accumulated amortization and are amortized on a straight-line basis over their respective useful lives of five to 20

years. Expected useful lives and amortization methods are reviewed annually.

(m) Impairment

Property and equipment and intangible assets are grouped into cash generating units (CGU) and reviewed for impairment when

events or changes in circumstances indicate that the carrying value of the CGU may not be recoverable. When events or

circumstances indicate that the carrying amount of the CGU may not be recoverable, the long-lived assets are tested for

recoverability by comparing the recoverable amounts, defined as the greater of the CGU’s fair value less cost to sell or value-in-

use, with the carrying amount of the CGU. Fair value is defined as the amount an asset could be exchanged, or a liability settled,

between consenting parties, in an arm’s length transaction. Value-in-use is defined as the present value of the cash flows

expected from the future use or eventual sale of the asset at the end of its useful life. If the carrying value of the CGU exceeds

the greater of the fair value less cost to sell and value-in-use, an impairment loss is recognized in net earnings for the

difference. Impairment losses may subsequently be reversed and recognized in earnings due to changes in events and

circumstances, but only to the extent of the original carrying amount of the asset, net of depreciation or amortization, had the

original impairment not been recognized.

(n) Maintenance

(i) Provisions

Provisions are made when it is probable that an outflow of economic benefits will be required to settle a present legal or

constructive obligation in respect of a past event and where the amount of the obligation can be reliably estimated.

The Corporation’s aircraft operating lease agreements require leased aircraft to be returned to the lessor in a specified operating

condition. This obligation requires the Corporation to record a maintenance provision liability for certain return conditions

specified in the operating lease agreements. Certain obligations are based on aircraft usage and the passage of time, while

others are fixed amounts. Expected future costs are estimated based on contractual commitments and company-specific history.

Each period, the Corporation recognizes additional maintenance expense based on increased aircraft usage, the passage of time

and any changes to judgments or estimates, including discount rates and expected timing and cost of maintenance activities.

The unwinding of the discounted present value is recorded as a finance cost on the consolidated statement of earnings. The

discount rate used by the Corporation is the current pre-tax risk-free rate approximated by the corresponding term of a

Government of Canada Bond to the remaining term until cash outflow. Any difference between the provision recorded and the

actual amount incurred at the time the maintenance activity is performed is recorded to maintenance expense.

(ii) Reserves

A certain number of aircraft leases also require the Corporation to pay a maintenance reserve to the lessor. Payments are based

on aircraft usage. The purpose of these deposits is to provide the lessor with collateral should an aircraft be returned in an

operating condition that does not meet the requirements stipulated in the lease agreement. Maintenance reserves are refunded

to the Corporation when qualifying maintenance is performed, or if not refunded, act to reduce the end of lease obligation

payments arising from the requirement to return leased aircraft in a specified operating condition. Where the amount of

maintenance reserves paid exceeds the estimated amount recoverable from the lessor, the non-recoverable amount is recorded

as maintenance expense in the period it is incurred. Non-recoverable amounts previously recorded as maintenance expense may

be recovered and capitalized based on changes to expected overhaul costs and recoverable amounts over the term of the lease.

(iii) Power-by-the-hour maintenance contracts

The Corporation is party to certain power-by-the-hour aircraft maintenance agreements, whereby the Corporation makes

ongoing payments to maintenance providers based on flight hours flown. Payments are capitalized when they relate to qualifying

capital expenditures such as major overhauls, otherwise, payments are recorded to maintenance expense on the consolidated

statement of earnings when payment is incurred.