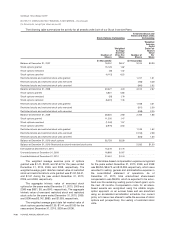

Vonage 2010 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2010 Vonage annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

|

|

V

O

NA

G

EH

O

LDIN

GS CO

RP

.

N

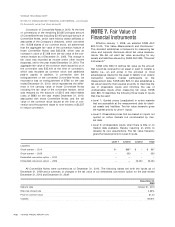

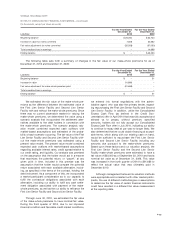

OTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(

In thousands, except per share amounts

)

Lawsuits b

y

the Nebraska Public

S

ervice

C

ommission an

d

New Mexico Public Regulatory

C

ommission that were

r

esolved in 2009 are examples of state public utilit

y

commission attem

p

ts to extend traditional state tele

-

communications re

g

ulation to our service. In these cases,

the state public utility commissions sou

g

ht to apply stat

e

universal service fundin

g

requirements to us. The Kansas

C

or

p

oration

C

ommission also has taken the

p

osition that i

t

has jurisdiction to seek state universal service

f

undin

gf

rom

nomadic VoIP providers. Similarly, the Public Utility Com-

mission of Ohio has adopted rules that would apply stat

e

fees for Telephone Relay Service to nomadic VoIP service.

O

n July 16, 2009, the Nebraska Public Service Com

-

mission and the Kansas Cor

p

oration Commission filed

a

p

etition with the FCC seekin

g

a declaratory rulin

g

or, alter-

natively, adoption o

f

a rule declarin

g

that state authoritie

s

may apply universal service fundin

g

(“USF”) requirement

s

to nomadic VoIP

p

roviders. We

p

artici

p

ated in the FC

C

p

roceedin

g

s on the petition. On November 5, 2010, th

e

FCC issued a declaratory rulin

g

that allowed states t

o

assess state USF on nomadic VoIP providers on a

g

oin

g

f

orward basis provided that the states comply with certai

n

conditions to ensure that imposin

g

state USF does no

t

con

f

lict with

f

ederal law or polic

y

. We expect that stat

e

p

u

bli

cut

ili

ty comm

i

ss

i

ons an

d

state

l

eg

i

s

l

ators w

ill

cont

i

nue

t

h

e

i

r attempts to app

l

y state te

l

ecommun

i

cat

i

ons regu-

l

at

i

ons to noma

di

c

V

o

IP

serv

i

ce.

S

tate and Municipal Taxe

s

I

n accor

d

ance w

i

t

h

genera

ll

y accepte

d

account

i

ng

p

rinciples, we make a provision for a liabilit

y

for taxes whe

n

i

t

i

s

b

ot

h

pro

b

a

bl

et

h

at a

li

a

bili

t

yh

as

b

een

i

ncurre

d

an

d

t

he

amount of the loss or range of loss can be reasonabl

y

est

i

mate

d

.

Th

ese prov

i

s

i

ons are rev

i

ewe

d

at

l

east quarter

ly

and adjusted to reflect the impacts of negotiations, settle

-

ments, rulings, advice of legal counsel, and othe

r

i

nformation and events pertaining to a particular case. For

a

p

eriod of time, we did not collect or remit state or municipa

l

t

axes

(

such as sales, excise, utilit

y

, use, and ad valore

m

t

axes

)

, fees or surcharges

(

“Taxes”

)

on the charges to our

customers for our services, except that we historicall

y

comp

li

e

d

w

i

t

h

t

h

e

N

ew

J

erse

y

sa

l

es tax.

W

e

h

ave rece

i

ve

d

i

nquiries or demands from a number of state and municipa

l

t

axing and 911 agencies seeking payment of Taxes that ar

e

a

pp

lied to or collected

f

rom customers o

fp

roviders o

f

tradi

-

t

ional

p

ublic switched tele

p

hone network services

.

Althou

g

h we have consistently maintained that these Taxes

do not apply to our service

f

or a variety o

f

reasons depend-

i

n

g

on the statute or rule that establishes such obli

g

ations,

a number o

f

states have chan

g

ed their statutes to expressl

y

i

nclude VoIP and we are now collectin

g

and remittin

g

sale

s

t

axes in those states. In addition, many states address how

VoIP providers should contribute to support public sa

f

et

y

a

g

encies, and in those states we remit

f

ees to the appro

-

p

riate state a

g

encies. We could also be contacted by state

or municipal taxin

g

and 911 a

g

encies re

g

ardin

g

Taxes tha

t

d

o exp

li

c

i

t

l

y app

l

yto

V

o

IP

an

d

t

h

ese a

g

enc

i

es cou

ld

see

k

r

etroactive payment o

f

Taxes. As such, we have a reserve

of $2

,

803 as of December 31

,

2010 as our best estimate o

f

t

he potential tax exposure

f

or an

y

retroactive assessment

.

We believe the maximum estimated exposure

f

or retro-

active assessments is approximatel

y

$8,000 as o

f

D

ecem

b

er 31

,

2010

.

E

mp

l

oyment

A

greements

O

ur

C

hief Executive

O

fficer and

C

hief Financial

O

fficer

are su

bj

ect to emp

l

o

y

ment contracts w

i

t

h

m

i

n

i

mum sa

l

ar

y

comm

i

tments t

h

at, su

bj

ect to annua

l

rev

i

ew, aggregat

e

$

1,375 per annum. Our Chief Executive Officer and Chie

f

Financial

O

fficer are also eligible for annual performance

b

onuses w

i

t

h

targets

b

ase

d

upon t

h

e

i

rt

h

en annua

l

sa

l

ary

.

T

he initial term of the emplo

y

ment contract with our

C

hie

f

Executive

O

fficer expires in 2011 but is subject to one-

y

ear

r

enewals unless prior notice of 90 da

y

s is provided b

y

eithe

r

p

art

y

. The emplo

y

ment contract with our

C

hief Financia

l

O

fficer ma

y

be terminated b

y

either part

y

upon 30 da

y

s’

notice. In the event of the termination of our

C

hief Executiv

e

O

fficer’s employment, depending upon the circumstances,

h

ew

ill b

e ent

i

t

l

e

d

to severance pa

y

ments up to an amoun

t

equal to a prorated annual bonus for the

y

ear of termi

-

nat

i

on, two

y

ear

’

s

b

ase sa

l

ar

y

,an

d

amounts to cover spec

i-

fied health care coverage premiums and outplacemen

t

s

ervices. In the event of the termination of our

C

hief Finan

-

cial

O

fficer’s employment, dependin

g

upon the circum-

s

tances, he will be entitled to severance payments up to an

amount equal to a prorated annual bonus for the year of

t

ermination and one year’s base salary

.

F

-3

1