TomTom 2010 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2010 TomTom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

p 62 / TomTom Annual Report and Accounts 2010

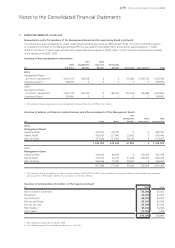

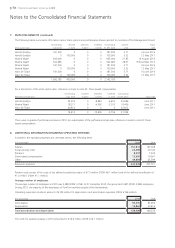

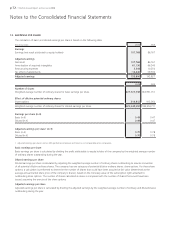

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Leasing

Leases are classified as finance leases whenever the terms of the lease transfer substantially all the risks and rewards of ownership to the

lessee. All other leases are classified as operating leases. Rentals payable under operating leases are charged to income on a straight-line

basis over the term of the relevant lease. Benefits received and receivable as an incentive to enter into an operating lease are also spread

on a straight-line basis over the lease term.

The group leases certain property, plant and equipment. Where the group has substantially all the risks and rewards of ownership, the

leases are classified as finance leases. Finance leases are capitalised at the lease commencement date at the lower of fair value of the

leased property and the present value of the minimum lease payments.

Lease payments are allocated between the liability and the finance charge with the corresponding rental obligations being included in

long-term liabilities. The interest element is charged to finance costs in the income statement. The property, plant and equipment is

depreciated over the shorter of the expected useful life of the asset and the lease term.

Derivative financial instruments and hedging activities

The group uses derivative financial instruments principally to manage the financial risks of changes in foreign exchange rates and

potentially adverse movements in interest rates related to our borrowing positions. The group does not use derivative financial instruments

for speculative purposes. All derivative financial instruments are classified as current or non-current assets or liabilities based on their

maturity dates and are accounted for at trade date. The group measures all derivative financial instruments using quoted prices for similar

instruments or input other than quoted prices. The fair values of the derivatives are disclosed in note 19. Gains or losses arising from

changes in fair value of derivatives are recognised in the income statement, except for derivatives that are highly effective and which

qualify for cash flow hedge accounting.

When hedge accounting is applied, the group formally assesses, both at the hedge’s inception and on an ongoing basis, whether the

derivatives that are used in hedging transactions are highly effective in offsetting changes in cash flows of hedged items. When it is

established that a derivative is not highly effective as a hedge or that it has ceased to be a highly effective hedge, the group discontinues

hedge accounting prospectively. When hedge accounting is discontinued, the group continues to carry the derivative on the balance sheet

at its fair value, and gains and losses that were recognised in Other comprehensive income up to the point of de-designation will remain

in equity until the forecast transaction is ultimately recognised in the income statement. Gains or losses on the hedging instrument after

de-designation will be recognised in profit or loss if the hedging instrument continues to be held.

The use of financial derivatives is governed by the group’s Treasury policies, approved by the Supervisory Board. These written principles

are consistent with the group’s risk management strategy.

Government grants

The group receives government grants related to the research and development activities performed by the group. Government grants are

recognised at their fair value when there is a reasonable assurance that the group will comply with the conditions attached to them, and

that the grants will be received. Government grants that are receivable as compensation for expenses or losses already incurred, or for the

purpose of giving immediate financial support to the group with no future related costs, are recognised in profit or loss in the period in

which they become receivable.

Pension costs

The group operates various defined contribution plans and a defined benefit plan for a German subsidiary. For defined contribution plans,

the group pays contributions to publicly or privately administered pension insurance plans on a mandatory, contractual or voluntary basis.

The group has no further payment obligations once the contributions have been paid. The contributions are recognised as employee

benefit expense when they are due. Prepaid contributions are recognised as an asset to the extent that a cash refund or reduction of

future payments is available.

The assets of the German defined benefit scheme are held separately from those of the group in independently administered funds.

Contributions are charged to the income statement as they become payable, in accordance with the rules of the scheme. The

contributions are included in employee benefit expense. Full defined benefit disclosures are not provided given the fact that the plan

is not significant.

In Italy, employees are paid a staff leaving indemnity on termination of employment. This is a statutory payment based on Italian civil law.

An amount is accrued each year based on the employee’s remuneration and previously revalued accruals. The indemnity has the

characteristics of a defined contribution obligation and is an unfunded, but fully provided liability. The costs of providing benefits under

the plans is determined separately for each plan. Actuarial gains and losses are recognised as either an income or an expense immediately.

Notes to the Consolidated Financial Statements